S&P Global — 23 Sep, 2020

Daily Update: September 23, 2020

By S&P Global

Subscribe on LinkedIn to be notified of each new Daily Update—a curated selection of essential intelligence on financial markets and the global economy from S&P Global.

While the coronavirus pandemic’s disruptions have done more in roughly nine months to reduce global emissions than the 2-degree Celsius pathway has in the five years since the Paris Agreement was signed, the determinant outcomes of its implications for the fight against climate change are yet to be seen. Will the drastic decline in greenhouse gas emissions seen during this crisis be enough to accelerate the global economy’s transition toward renewable energy sources, or will fossil fuel generation regain its grip?

In order to keep atmospheric warming at or below 2 degrees Celsius as compared to industrial levels through 2050, the world will need to reduce more than 10 times the emissions that have resulted from the current crisis, according to new research from S&P Global Platts and S&P Global Ratings.

“COVID-19 has altered three fundamentals drivers of emissions: macroeconomics, behaviors, and policy, that combined will lower energy sector CO2 emissions by 27.5 gigatons over 2020-2050. However, this is only a minor step in the direction needed to meet the 2-degree target, which would require more than 10 times that reduction over the period,” Dan Klein, &P Global Platts Analytics’ head of scenario planning, said in the report. “The emissions reduction achieved in 2020 nevertheless is equivalent to the decline required by 2027 in a 2-degree scenario, illustrating that sizable emissions reductions are possible.”

Next year, global oil demand is projected to recover roughly 75% of demand loss garnered this year, according to the new projections from S&P Global Platts Analytics, which believes long-term demand for oil has been permanently altered by the pandemic. Overall oil consumption is unlikely return to pre-pandemic levels until late 2022.

Against the backdrop of S&P Global Ratings’ expectation that global output will contract 3.8% this year, the prospects of achieving such enormous emissions reductions is largely dependent on governments’ making good on their commitments to centering sustainable policy in their recovery plans.

“The two economies that will shape the way that Asia-Pacific’s COVID-19 recovery affects the global energy transition are China and India. We expect China's transition to a low-energy-intensity economy, fueled increasingly by renewables, to stall in 2020 and 2021 as policy stimulus ripples through the economy,” S&P Global Ratings’ Chief APAC Economist Shaun Roache said in the report. “India’s economy has been hit by an enormous shock that will impose large, permanent damage. While the plunge in activity will reduce energy use, policymakers are unlikely to focus on energy transition until the economy regains its footing.”

U.S. Democratic presidential candidate Joe Biden has proposed a $2 trillion clean energy spending plan that includes supporting of a carbon-free power sector by 2035. Combined with ambitious objectives for green hydrogen to accomplish within the next decade, one-third of Europe’s Recovery Fund is allocated to green investments.

However, the power to push economies towards greener growth isn’t the sole responsibility of citizens or policymakers. Rather, markets have the ability to incentivize change—if more investors took action.

“If markets are given the choice, then people can act on them,” Roman Kramarchuk, head energy scenarios, policy, and technology analytics at S&P Global Platts, said during S&P Global’s Sept. 22 Climate Week webinar on the transition to a low-carbon economy. He explained that increased transparency and information will help markets, such as commodities, work better, and this should naturally lead the transition. “This view can be summed up, I think, as, ‘the natural, market-driven elements of the transition have been held back up to now by a lack of information.’”

Today is Wednesday, September 23, 2020, and here is today’s essential intelligence.

ESG in the Time of COVID-19

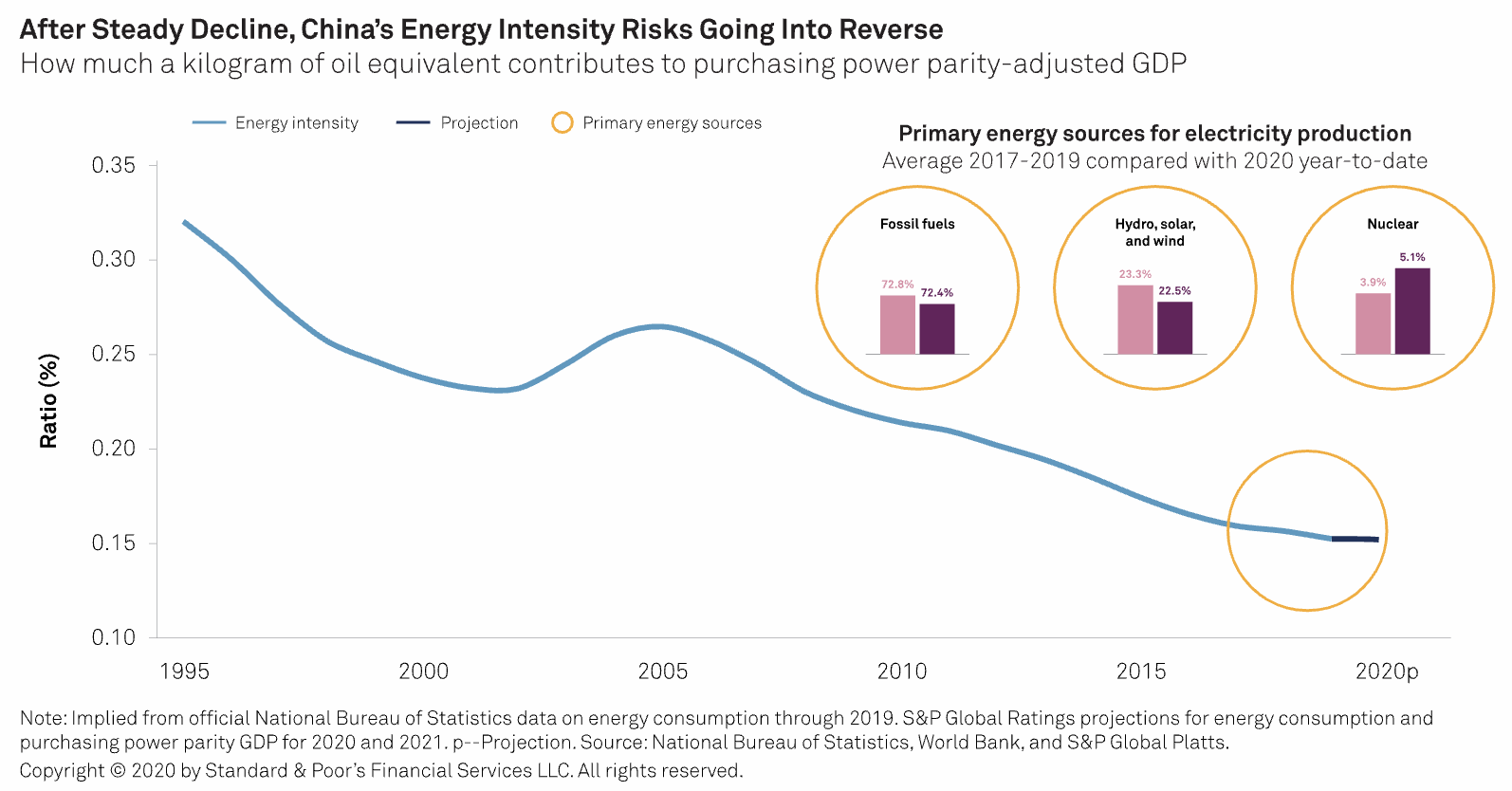

Economic Research: China's Energy Transition Stalls Post-COVID

China's energy policy is drifting. To dig the economy out of its COVID lows, planners are approving more infrastructure, and using more energy to drive the economy. China is also relying more on high-carbon fuel. S&P Global Ratings believes Beijing's success in returning to a less energy-intensive growth model has implications for its economy, financial resilience, and environment. China is the world's largest emitter of carbon. It needs to dramatically cut its emissions if the world is to meet the Paris Agreement target of capping global warming within 2 degrees Celsius by 2050. Climate scientists widely view the threshold as the limit to avoid potentially catastrophic warming. As this year's floods in the Yangtze delta show, climate change carries social and economic risks.

—Read the full report from S&P Global Ratings

Voluntary Carbon Market Grows 6% On Year In 2019: Ecosystem Marketplace

The value of the global voluntary carbon market increased by 6% year on year in 2019, according to a report by environmental markets information group Ecosystem Marketplace. While average carbon offset prices were unchanged in 2019, prices increased 30% for nature-based emissions projects, according to the report released Sept. 21."In order to deliver deep and cost-effective [emissions] reductions now, many companies have pledged to become carbon neutral in the near term by financing emissions-reductions elsewhere – or in climate parlance, 'offsetting' any emissions they can't yet eliminate," said Ecosystem Marketplace.

—Read the full article from S&P Global Platts

National Grid, Tennet To Study Joint GB-NL Offshore Wind/Interconnection Project

National Grid Ventures and Tennet are to study development of 2 GW of interconnection between Britain and the Netherlands connecting up to 4 GW of offshore wind, the network companies said Sept. 22. The two companies aim to have a "path-finder" project defined by the end of 2021 with a view to delivering an operational asset by 2029.

—Read the full article from S&P Global Platts

Long-Term R&D, Hydrogen, Renewables Powering Energy Transition: Executives

Officials at chemical giant BASF and investor-owned utility Southern California Edison are moving the energy transition forward through efforts such as electrifying steam cracker technology, increased use of hydrogen and renewable energy procurements, they said during a Sept. 21 New York City Climate Week event. "We are serving a population that has seen the impacts of climate change in a major way" through drought and recent wildfires, Pedro Pizarro, president and CEO of Edison International, the parent company of Southern California Edison, said.

—Read the full article from S&P Global Platts

US Net-Zero Targets Require Earlier Coal Retirements, Gas Emissions Elimination: Deloitte

The current and scheduled pace of coal-fired power plant retirements needs to speed up in the next few years and emissions from their gas-fired counterparts must be eradicated for US companies to reach their decarbonization goals, Deloitte said in a report released Sept. 21. In a report titled, "Road to Net Zero Reality Check: So Much To Do, In So Little Time," Deloitte said "the math is not adding up across the phases required to achieve decarbonization in the next 30 years," and it asked, how can utilities close that gap and at what cost?

—Read the full article from S&P Global Platts

Analysis: High Credit Values Outweigh Cost Of Production For US Renewable Distillates

Rising prices for government credits have pushed the value of available incentives above the cost of production for renewable distillates, according to data analyzed by S&P Global Platts. D4 Renewable Identification Numbers have reached multi-year highs amid rallies in soybean oil, the most common feedstock for biodiesel in the US, while California Low Carbon Fuel Standard credits have hovered between $190/mt and $210/mt for the past two years. The reinstatement of the $1/gal federal biomass-based diesel tax credit through the end of 2022 has added additional value to entice refiners.

—Read the full article from S&P Global Platts

US Gas-To-Coal Switching To Boost Coal Consumption, Help Trim Stocks

Despite a long-term trend of coal power plant closures, and dented energy demand more recently due to the coronavirus crisis, upside for coal has been materializing in the US as gas-fired generators reacted to higher prices in the summer months and coal regained some market share lost in 2019. S&P Global Platts Analytics expects coal generation and production to ramp up through the rest of 2020. Platts Analytics projects the combination of seasonal demand patterns, recovering power demand and increasing electricity and gas prices will drive an increase in US coal consumption in the generation sector of 5-15 million st through the end of 2020, compared with 2019.

—Read the full article from S&P Global Platts

Listen: Biden's Shift On Energy, Climate Issues Ahead Of November Vote (Part 2 Of 2)

In Part 2 of Platts’ look at the US presidential candidates' evolving energy platforms, S&P Global Platts examine how progressive Democrats have pushed former Vice President Joe Biden further left on climate and environmental policies. Glenn Schwartz, director of Rapidan Energy Group's Energy Policy Service, shares his latest prediction for how far Biden would go in restricting oil and gas drilling, and why running mate Kamala Harris' views on fracking and climate remain important in predicting the future of the Democratic energy platform.

—Listen and subscribe to Capitol Crude, a podcast from S&P Global Platts

Uncertainty in the Global Economy

Economic Research: U.S. Biweekly Economic Roundup: A Dovish Fed With A Cautious Stance On Economic Growth

So what are the economic benchmarks the voting committee will look for before considering increasing the federal funds rate or changing the pace of asset purchases related to quantitative easing (QE)? On the interest rate policy, the FOMC expects to maintain the federal funds rate target at its current range until reaching "maximum employment" and until inflation has risen to its 2% target and is on track to "moderately exceed" that "for some time." On QE, the FOMC didn't provide any more guidance on the time or economic outcome dimensions other than continuation at current pace (at least) "over coming months."

—Read the full report from S&P Global Ratings

Overseas Companies Struggle To Gain Ground In China's Bulk Purchase Of Drugs

Global pharmaceutical companies are fighting to gain a larger share in China's bulk purchase program for generic drugs, even as domestic companies continue to have the upper hand amid intense price competition. Under the country's bulk purchase program, public hospitals buy predetermined quantities of generic drugs from companies that tender the lowest prices via a bidding process. These purchases account for between 50% and 70% of the total by volume for public hospitals, Zhang Jialin, Hong Kong-based healthcare analyst at ICBC, told S&P Global Market Intelligence. China has concluded three rounds of bulk purchases of generics, after a pilot program was launched in 11 cities in December 2018.

—Read the full article from S&P Global Market Intelligence

Potential U.S. Ban On SMIC Could Choke China's Semiconductor Supply Chain

A potential U.S. ban on Semiconductor Manufacturing International Corp. could cause widespread disruption to China's semiconductor supply chain, according to analysts. SMIC makes chips essential to devices including handsets, telecom base stations and tablets. The company relies on U.S. equipment and software to perform steps in the chip production process such as printing circuits and inspecting the product, the analysts said. The Trump administration is reportedly considering adding SMIC to its trade blacklist. A ban would call into question SMIC's ability to manufacture chips using high-end techniques, Mark Li, senior research analyst at Sanford C. Bernstein & Co. LLC, said.

—Read the full article from S&P Global Market Intelligence

US ELECTIONS: Biden Might Be Better For Fair Trade: Irepas Panelists

With the upcoming US presidential elections, Democratic nominee Joe Biden's administration might provide a better chance for fair trade, panelists at the virtual 83rd International Rebar Producers & Exporters Association (Irepas) conference said this week. F. D. Baysal, president and CEO of Seba International, highlighted the uncertainty, and said that with the death Sept. 18 of US Supreme Court Justice Ruth Bader Ginsburg everything is up in the air. President Donald Trump's re-election will not bring about many changes, though a Biden administration might be more sympathetic toward fair trade, he said. Nonetheless, the Section 232 tariffs will be hard to dismiss for at least the first two to three years of the new administration, he added.

—Read the full article from S&P Global Platts

The Future of Credit

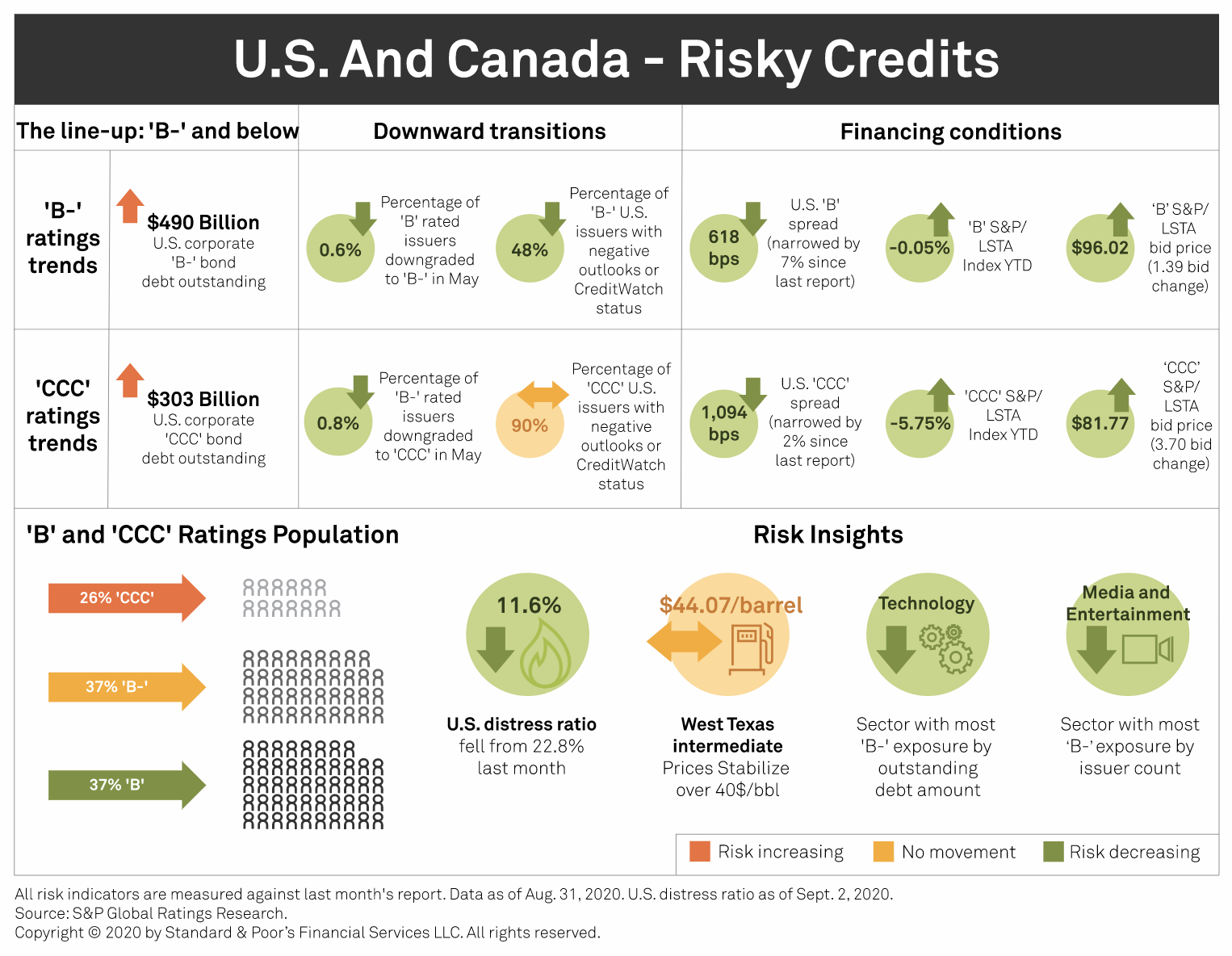

Credit Trends: Risky Credits: The Number Of 'CCC' Category Ratings Stabilizes

Negative actions slow: Negative rating actions in the U.S. and Canada slowed in August, with only 32, down from 48 in July and 374 in April, when state and local governments imposed stringent social distancing measures across the U.S. and Canada. The majority (69%) of negative rating actions in August were downgrades, and most followed a previous negative rating action since March, such as an outlook revision or CreditWatch placement. Defaults slow: There were 11 defaults in August, down from an average of about 31 defaults per month over the previous four months. All 11 defaults in August were rated in the 'CCC' and lower rating categories, illustrating the high default risk associated with this part of the ratings spectrum. Five companies rated in these categories have defaulted so far in September (as of Sept. 9).

—Read the full report from S&P Global Ratings

Industries Most and Least Impacted by COVID-19 from a Probability of Default Perspective – September 2020 Update

In an effort to revisit the impact of coronavirus (COVID-19), S&P Global Market Intelligence took another look at the most and least affected industries to date with a historical view of the summer months. In MI’s two previous blogs, dated March 2020 and April 2020, S&P Global Market Intelligence discussed how COVID-19 caused a significant negative impact on supply chains and disrupted many industries around the world, including Airlines and Oil and Gas Drilling. However, S&P Global Market Intelligence saw a plateau in the probability of defaults (PD) toward the end of March. This plateau continued into the summer months, declined and then picked back up in a second increase that coincided with a second wave of virus infections in some countries.

—Read the full article from S&P Global Market Intelligence

Down But Not Out: Insurers' Capital Buffers Are Proving Resilient In The Face Of COVID-19

S&P Global Ratings' surveillance of insurance companies has both increased and deepened since the COVID-19 pandemic began to spread around the globe. The impact has been broad, covering blanket travel restrictions, societal lockdowns, and extensive monetary and expansive fiscal policy responses. Throughout the pandemic, S&P Global Ratings has focused on key risks to insurers, to ensure ratings and outlooks appropriately reflect Ratings’ expectations. To date, S&P Global Ratings has taken 51 actions globally, representing just under 10% of Ratings’ insurance portfolio (see chart 1). This compares favorably to the broader corporate and government rating universe where 41% of ratings have experienced a downgrade, negative outlook revision, or CreditWatch negative placement.

—Read the full report from S&P Global Ratings

US Corporate Bankruptcies Grow By 25 In Last 2 Weeks

U.S. corporate bankruptcies continue to climb during the coronavirus pandemic as 25 new companies in the last two weeks joined a growing list of bankruptcies in 2020, according to an S&P Global Market Intelligence analysis. A total of 492 companies have entered bankruptcy proceedings as of Sept. 20. The number continues to trend higher than comparable levels since 2010. Market Intelligence's bankruptcy analysis includes public companies or private companies with public debt. Public companies included in the list of companies with public debt must have at least $2 million in either assets or liabilities at the time of the bankruptcy filing. In comparison, private companies must have at least $10 million in assets or liabilities.

—Read the full article from S&P Global Market Intelligence

US Card Credit Performance Holds Up As Stimulus Safety Net Frays

Credit card portfolios once again showed strong credit performance in monthly reports posted in the middle of September, with lenders continuing to say that emergency pandemic measures would push the recognition of actual loan losses into 2021. The average net charge-off rate for securitized receivables across six large issuers increased 12 basis points from July to 2.21% in August, but was down nine basis points from the year prior. Delinquencies as a percentage of receivables declined month over month at Citigroup Inc., JPMorgan Chase & Co., Capital One Financial Corporation, Bank of America Corp., Discover Financial Services and American Express Co., and the average for the group fell for the fourth consecutive month since April.

—Read the full article from S&P Global Market Intelligence

Why Reach for Yield When You Can Use a Ladder?

The current low interest rate environment is forcing many investors to reassess their risk tolerances. Typically, fixed income investors have three main options when trying to “reach” for yield: 1. Move down in credit quality (i.e., take on more credit risk); 2. Increase duration (i.e., take on more interest rate risk); or 3. Move to alternative assets (i.e., those that can potentially incur other illiquidity and lockup provisions). Of course, all of these options pose the same question: Is the incremental yield worth the additional risk?

—Read the full report from S&P Dow Jones Indices

Banking Sector Under Pressure

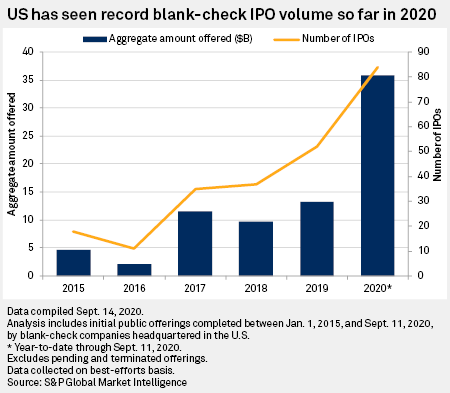

Investment Bankers Tracking Spacs See No Slowdown In Record-Breaking Year

A wave of funding for new special-purpose acquisition companies over the summer is showing few signs of slowing down heading into the final months of an already record-breaking year for blank-check companies. SPACs have shed their checkered pasts in recent years to attract a new class of investors, executive teams and private companies. Now, SPACs are debuting in the U.S. public markets and striking deals at an unprecedented pace expected to continue for the foreseeable future, according to investment bankers, securities lawyers and other capital markets experts.

—Read the full article from S&P Global Market Intelligence

Fincen Leak Is A 'Wake-Up Call' For EU To Address Financial Crime, MEP Says

Leaked documents from the U.S. Financial Crimes Enforcement Network showing $2 trillion in suspicious transactions reported by global banks, including some of the largest institutions in Europe, are "a wake-up call" for EU authorities who need to take urgent action, EU parliamentarian Sven Giegold told a press conference. He was speaking after BuzzFeed News obtained more than 2,100 suspicious transaction reports filed with FinCEN, which is part of the U.S. Treasury, and other U.S. government documents covering the period 1999 to 2017.

—Read the full article from S&P Global Market Intelligence

India Needs Bad Banks, Government Exit From Some Lenders: Former Central Bankers

India should set up bad banks to resolve nonperforming loans, reduce its ownership in some state-run lenders to below 50% and create a greater variety of structures to help grow its banking sector, former Reserve Bank of India Governor Raghuram Rajan and former Deputy Governor Viral Acharya said. India needs to transform its banking sector to make it an engine of growth as government finances are under "enormous" strain after an already slowing economy was hit by the coronavirus pandemic, Rajan and Acharya wrote in a Sept. 21 paper, listing a number of "implementable reforms" for the sector. "There may be a window of opportunity in which these reforms may be possible since the status quo is untenable," they said.

—Read the full article from S&P Global Market Intelligence

Technology & Innovation

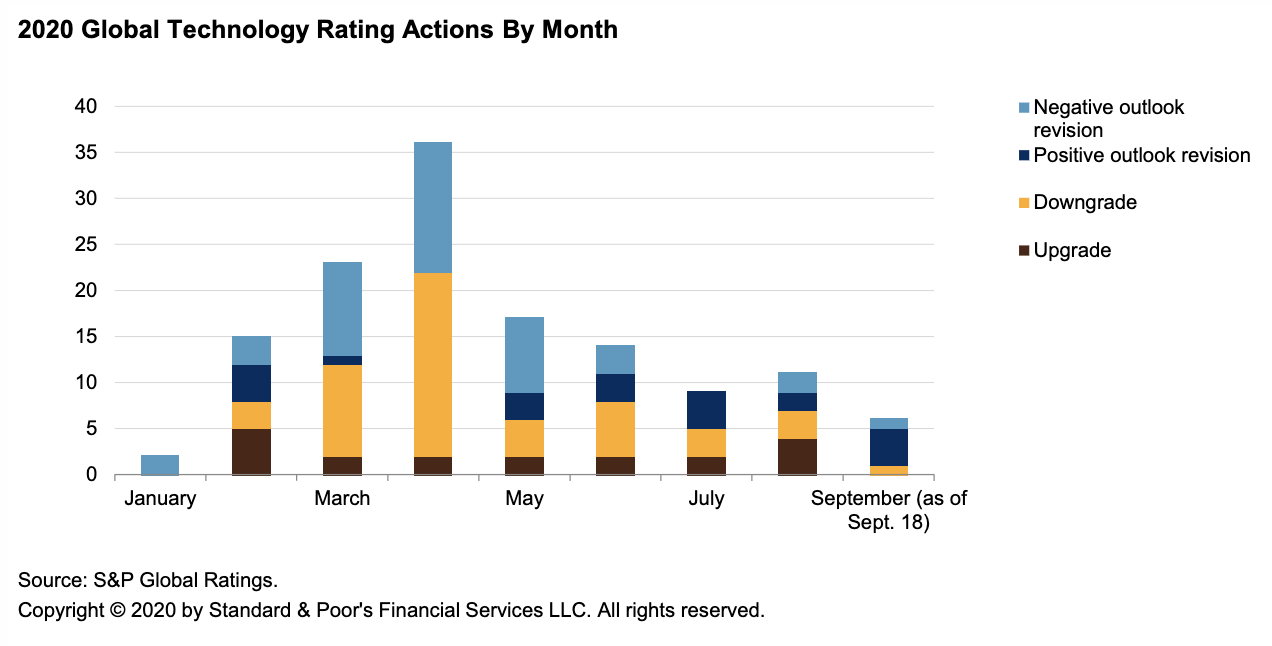

2020 Global IT Spending Outlook Improves Through COVID-19 Disruption

S&P Global Ratings took 54 negative rating actions in March and April 2020 because of COVID-19-related concerns. Since then, financial markets have stabilized and economies have gradually reopened. Work-from-home-related spending and an accelerated move to the cloud boosted first-half 2020 global IT spending above Ratings’ expectations. The software segment, despite growing less than S&P Global Ratings had forecast, outperformed all other segments, in part because of its mission-critical nature. S&P Global Ratings expect enterprise customers will pull back on spending in second-half 2020, given the slow pace of economic recovery. S&P Global Ratings have revised Ratings’ 2020 global information technology (IT) spending outlook.

—Read the full report from S&P Global Ratings

SASE, ZTNA And XDR: Three Security Trends Catalyzed By The Impact Of 2020

As S&P Global Market Intelligence emerge from the first months of a very different world from the one prior to the RSA Conference, As S&P Global Market Intelligence finds themselves taking stock of the trends shaping technology and asking what's next. As S&P Global Market Intelligence recently had occasion to think about this question in detail as As S&P Global Market Intelligence updated their outlook for 2020 – not from the point of view of late 2019, when it was first published, but through a very different lens in the months since the World Health Organization declared COVID-19 a pandemic. Midway through Q3, as S&P Global Market Intelligence find themselves taking stock once again as As S&P Global Market Intelligence prepare for the coming year, and As S&P Global Market Intelligence see some definite themes emerging in information security.

—Read the full article from S&P Global Market Intelligence

The Future of Energy & Commodities

Watch: Market Movers Americas, Sep 21-25: Flotilla Of U.S. Crude Heads Toward China

In this week's Market Movers Americas, presented by Kelsey Hallahan: VLCC flotilla of US crude heads toward China; higher netbacks bolster US LNG feedgas demand; NYMEX RBOB futures rise as hurricanes reduce refinery runs; and US hot-rolled coil prices approach $600/st.

—Watch and share this Market Movers video from S&P Global Platts

Spotlight: New Cases Of Coronavirus Remain High Globally, Economic Recovery On Track, Impairment In The Energy Space Lessened

While new cases of coronavirus remain very high globally, economic recovery appears on track and impairment in the energy space has lessened. Even so, product cracks are low, indicative of weak demand, both seasonally and year on year. Power demands have held up well, almost across the board, and have certainly risen markedly from spring. S&P Global Platts Analytics has just released its Global Economic Outlook report, GEO. The economic recovery remains on track, but risks remain due to a very high rate of increase in coronavirus cases. There has been a significant upswing in cases within Europe, while cases in India continue rising at the highest rate globally. Renewed lockdown measures have been re-instituted in Israel (3 weeks) and in Jakarta, Indonesia (two weeks).

—Read the full article from S&P Global Platts

Pa. Shale Gas Production Flatlines In June As Producer Cuts Take Effect

Shale gas production in Pennsylvania dropped 2% in June from May, to 18.48 Bcf/d, almost flat to the year prior, according to data from the state Department of Environmental Protection. Volume cuts by EQT Corp., the nation's largest natural gas producer, accounted for a large part of the falloff. EQT announced in May it was shutting in 1.4 Bcf/d of production, about one-third of companywide volumes. That led to an immediate 11% drop in its Pennsylvania production, followed by another 10% cut in June. EQT's Pennsylvania production fell to 2.86 Bcf/d in June, a 16% decrease year over year.

—Read the full article from S&P Global Market Intelligence

Written and compiled by Molly Mintz.

Content Type

Theme

Language