13 November 2025

Mastering the “What Ifs”: Scenario planning for resilience and agility

Article Summary

In a recent webinar presented by Automotive News, S&P Global Mobility experts Michael Robinet and Guido Vildozo explored the mounting challenges facing OEMs and the critical need for advanced scenario planning capabilities.

As the industry grapples with trade policy uncertainty, regulatory shifts, rapidly changing consumer preferences, changing cost structures and Chinese OEM competition, manufacturers are in need of agile, data-driven planning that can model multiple assumptions simultaneously and respond to sudden market changes.

- The planning crisis: Why traditional tools fall short

- US market dynamics: Tariffs, regulations, and cost pressures

- European and Chinese markets: Electrification under pressure

- Financial realities: Understanding natural adoption vs cost to build and implications on profitability

- Building a modern scenario planning capability

- Conclusion

The planning crisis: Why traditional tools fall short

While pandemic-era challenges may be in the rearview mirror, the automotive industry continues to face unique hurdles that demand immediate strategic attention.

Still, OEMs continue to struggle to develop reliable and agile forecasts. The root cause? Many organizations remain dependent on outdated scenario planning tools, such as spreadsheets and legacy software systems, that simply cannot keep pace with today's volatile environment. The consequences are severe: misallocated capital, missed opportunities, and strategic decisions based on incomplete assumptions.

In a recent webinar hosted by Automotive News, S&P Global Mobility experts Michael Robinet and Guido Vildozo explored the current market landscape and why growing uncertainty has made scenario planning essential.

“What tools are you using to plan for 2026?” asked Vildozo, Associate Director of Automotive Consulting. “Do you have the right tools available to you or are you trying to run a race car with bicycle tires?”

US market dynamics: Tariffs, regulations, and cost pressures

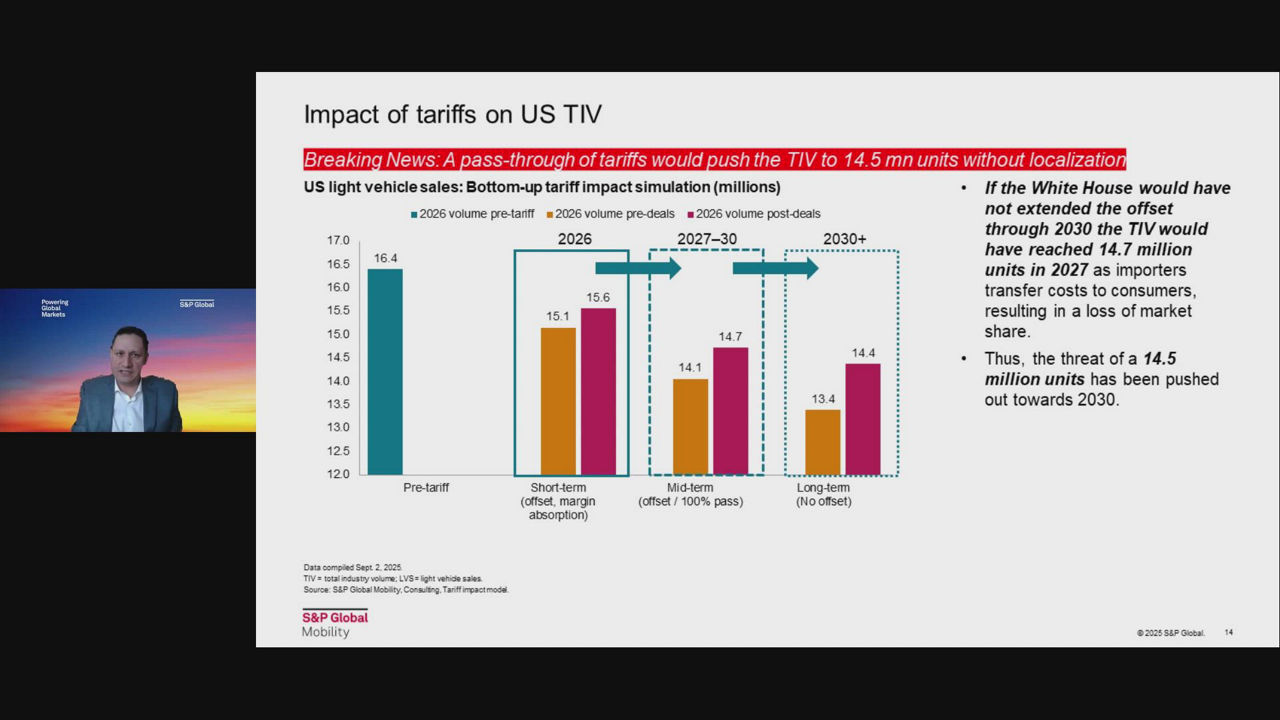

The automotive tariffs landscape has created extraordinary forecast volatility. Original tariff proposals threatened to deteriorate the US market significantly. While recent trade deals with Japan, the EU, and South Korea—combined with government offsets—have stabilized projections, significant complexity remains.

“We do have some stability, but it doesn't mean that the problem has gone away,” Vildozo noted. “We're still looking at the risk of potentially going down to 14 million units if we can't bring some of that manufacturing home, or [if] we don't change some of the different pieces that are tied to trade and tariffs.”

Regulatory changes have been equally dramatic. The potential rollback of NHTSA’s Corporate Average Fuel Economy (CAFE) standards to 35 MPG—essentially 2020-2021 levels—fundamentally altered the electrification equation, reducing battery electric vehicle (BEV) demand.

These and other changes mean that OEMs must now model natural consumer demand rather than incentive-driven adoption—a transition requiring sophisticated scenario planning that can simultaneously evaluate tariff exposure, component sourcing strategies, manufacturing footprint decisions, and evolving demand patterns.

European and Chinese markets: Electrification under pressure

.Europe's automotive landscape reveals deep regional fragmentation, with every country taking their own trajectory on electric vehicles. While the European Union pursues a 100% CO2 reduction target by 2035, individual regions show vastly different EV adoption rates. For example, Scandinavia and Northern Europe exceed 40% BEV penetration, while Southern and Eastern Europe lag below 5%.

Various countries in Europe have also backed away from aggressive ICE ban timelines, adding uncertainty to the market. Robinet noted that OEMs are extending ICE platforms and developing range extenders, requiring entirely new capital planning strategies.

Mainland China presents an equally daunting competitive challenge. Mainland Chinese OEMs now dominate their 25-30-million-unit home market, with Western OEMs losing massive production share.

"Every time you lose one point of share towards the Chinese OEMs away from the Western OEMs,” noted Robinet, “that is a movement of a plant the size of an Arlington or a Dearborn." North American OEMs shouldn't feel shielded, he added.

These combined dynamics demand comprehensive scenario planning tools for OEMs to evaluate regional variations, regulatory pathways, competitive responses, and manufacturing strategies simultaneously.

Financial Realities: BEV adoption vs. profitability

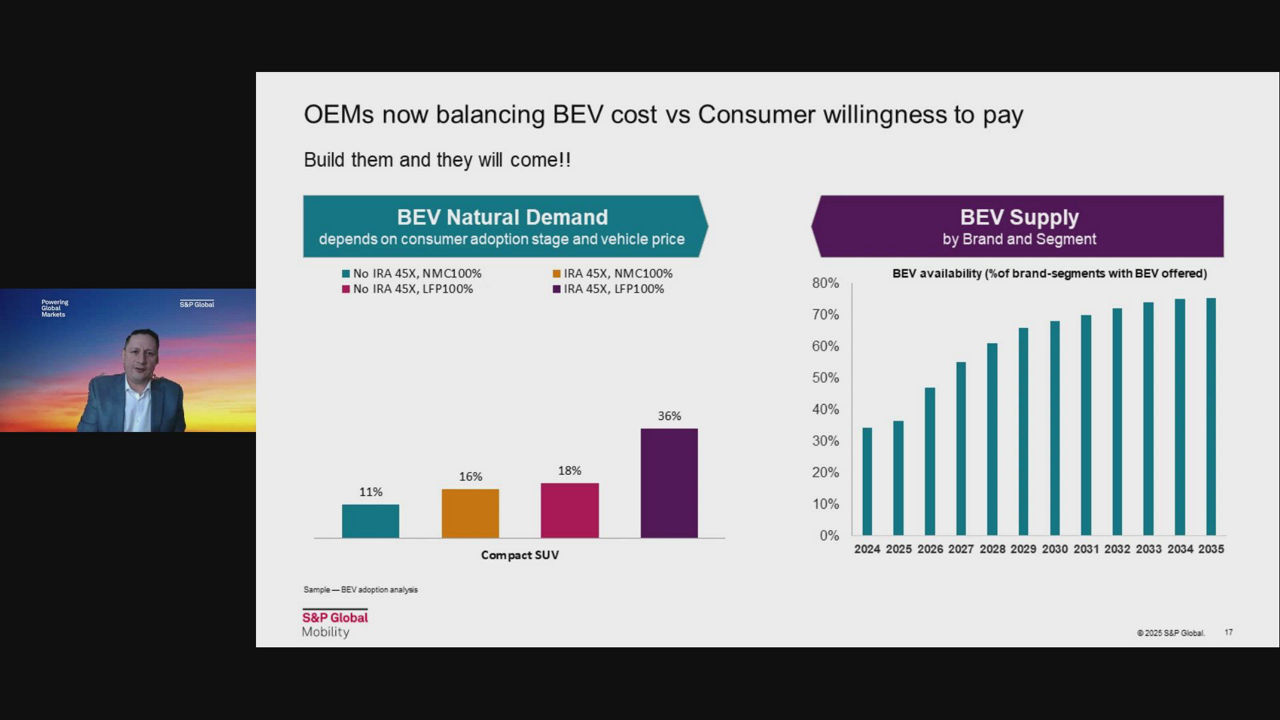

The financial calculus of powertrain transitions has become sobering; current sales data reveals that consumer willingness to pay rarely aligns with the cost to build electrified vehicles. “We can very clearly see, at least in North America for what remains of the decade, it will be very hard to generate a profit on some of these [EVs],” noted Vildozo.

The compact SUV segment illustrates many of the profitability challenges facing OEMs in the transition to electrification. Consumers show little willingness to pay premiums for BEVs in this segment, particularly due to concerns around range and charging convenience. Hybrid vehicles present stronger margin opportunities, while range extenders could achieve profitability by 2030 once LFP battery capacity scales up.

Tariff costs add another financial burden. Some OEMs are now facing monthly tariff expenses exceeding $600 million—in many cases north of 5% of their new light vehicle sales revenue.

These costs are being subsidized through margin absorption rather than passed to consumers, but that may not continue much longer.

Building a modern scenario planning capability

OEMs have much to consider and many pain points to plan for, from affordability and market shifts to supply chain uncertainties and tariffs. Traditional planning tools simply cannot provide the multi-variable analysis needed for confident investment decisions in the current environment.

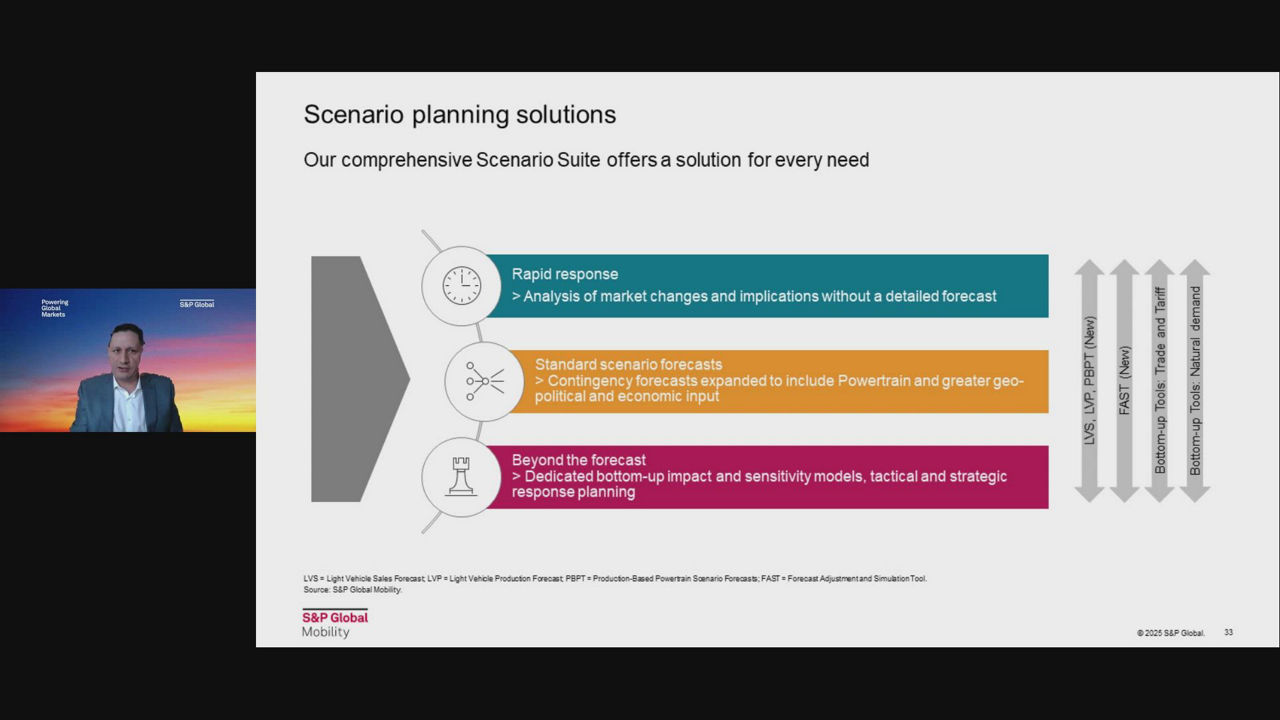

To navigate this complexity, OEMs need to fundamentally rethink their approach to scenario planning, moving beyond traditional top-down forecasting toward both top-down and bottom-up methodologies.

“This is what we're calling ‘beyond the forecast,’” said Vildozo, explaining S&P Global Mobility’s scenario planning solution for OEMs, the Forecast Adjustment and Simulation Tool (FAST). “It's not our standard approach where we look at the macro and we start to derive that into vehicle sales. When we're looking at beyond the forecast, we look at the lowest level of granularity and build that up... We want to provide as many different perspectives as possible to put you in the driver's seat.”

OEMs need capabilities that enable simultaneous analysis of multiple assumptions—something Excel spreadsheets and legacy systems simply cannot deliver at the required speed and accuracy. The planning process must provide both high-level strategic insights and granular bottom-up analysis, allowing decision-makers to quickly model how tariff scenarios, regulatory pathways, or demand shifts impact their business across showroom composition, market volumes, powertrain mixes, and manufacturing footprints.

Crucially, organizations need to put planning control directly in the hands of strategic planners, product managers, and volume planners rather than creating bottlenecks through centralized analytics teams.

Conclusion

The automotive industry stands at an inflection point where traditional planning approaches may not suffice. Market complexity, regulatory uncertainty, and competitive pressures demand scenario planning capabilities that match today's pace and sophistication. Organizations that continue relying on outdated tools risk making strategic errors with consequences measured in billions.

Scenario planning cannot be a quarterly exercise, but rather an “on-demand” capability for informing decisions whenever major capital investments or strategic pivots are required. This means tools must be intuitive enough that planners can explore assumptions without requiring data science expertise, while maintaining the analytical rigor needed for confident multi-million-dollar commitments.

To learn more about today’s auto industry landscape and how a modern scenario planning tool can help OEMs become more agile, download our whitepaper, Taming complexity with agility: Confident scenario planning for OEMs.

This article was published by S&P Global Mobility and not by S&P Global Ratings, which is a separately managed division of S&P Global.