11 Feb, 2021

Relative pricing in spotlight for European high-yield bonds and leveraged loans

By Luke Millar

A clear pattern has been established in the opening weeks of this year as secured bonds have priced tighter than leveraged loans in Europe. This dynamic has developed in the last year or so, and was typically applicable to only a small number of well-liked credits, but this year it has become ubiquitous, and the yield differential in some instances between bonds and loans has never been bigger. It also means that private equity sponsors and lenders now have even more firepower at their disposal, with the technicals in both markets coming together to create a “Goldilocks” scenario for borrowers.

“There is a ton of liquidity in both markets, and so it is sensible to take advantage of it and generate the best execution for clients,” says a head of syndicate. “It is easier to price the bonds inside loans by 25-50 basis points than ever before.”

“We are pitching secured bonds alongside term loans wherever we can,” states a head of leveraged finance. “Both markets are in fantastic shape, and there is high demand for deals. It makes sense where there is a big enough debt quantum to raise fixed and floating paper to ensure best pricing.”

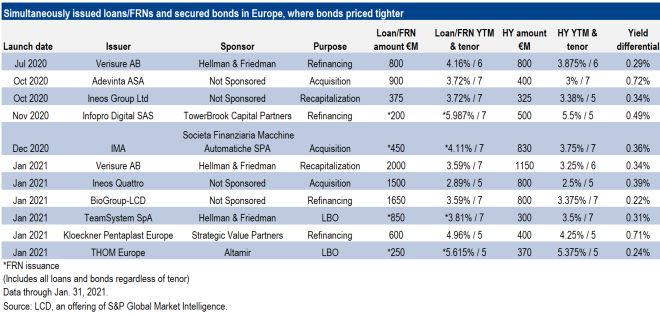

|

While 2020 saw five cases all year when a borrower's bonds priced tighter than a concurrent loan or floating-rate debt offering, this year has already hosted six such instances. What’s more, the differential is growing. It is possible to look at a like-for-like comparison here too, as Verisure AS and Ineos Quattro Finance 1 PLC both issued bonds and loans together last year and this year, and in both instances the yield differential has grown to 34-39 basis points, from 29-34 basis points.

|

Against the grain

That there has been a clear pick-up in such instances of bonds pricing tighter than loans, and even a widening of the differential, goes against the grain of European leveraged finance history.

Indeed, it has traditionally been rare for a secured bond to price tighter than a loan, as tracked on an average basis over a rolling three-month period, and in recent times loans have been significantly lower-yielding on this measure. That though was largely because the bond market took on greater credit risk in 2020, offering financing to companies that were either in dire need of liquidity or had a chequered past, one that required a premium to be added. Just over a month into this year's action, however, that average yield differential is now coming down, driven by the sharper tightening in bond yields.

Bond yields are falling sharply due to the relative value of the asset class, versus other fixed income products, investors and bankers say. “High-yield is driven by relative value to other fixed income asset classes,” confirms another head of leveraged finance. “Much of the fixed income world is either negative-yielding or has very low yields. Consequently, more investment-grade accounts are coming into double-Bs, and this drives yields down in single-Bs. High-yield is really the only fixed income product offering much in the way of yield.”

“Central bank stimulus is here to stay, and the only place you can generate any yield is in high-yield,” notes a fund manager. “The default rate is going to stay low and holding cash is negative return. It makes sense in this environment to pile into high-yield, and that is what you are seeing — despite none of us liking valuations.”

While high-yield has been pumped up by central bank stimulus, loan spreads are floored to a large extent by CLO liabilities (CLOs are the predominant investor segment in European leveraged loans). Here there has been good news for the market, with triple-A CLO spreads and the weighted average cost of capital tightening sharply, and by more than most expected, so far this year. The tightest triple-A print this year is 83 basis points versus 105 basis points late last year, and this fall has enabled the average yield on a TLB to come down almost 30 basis points to 4.16% on a rolling three-month rolling basis, according to LCD.

In short, both the loan and bond asset classes are enjoying very strong technical support as demand outweighs supply — with repayments adding further cash to investors' coffers in both markets — though for now, it is high-yield that is offering the more attractive cost of financing.

Consequently, high-yield is gaining a more prominent seat at the leveraged finance table, even though it is still too early in the year to draw definite conclusions.

|

Indeed, when it comes to funding corporate acquisitions, bond-only financing has been used 27% of the time so far this year, which is more than double the share recorded in all of 2020, according to LCD. Moreover, when adding in deals with senior debt plus bonds, then bonds have been used in 45% of M&A situations already this year, versus just 25% in 2020, and an average of 24% for the period 2016-20. Comparing a month with a full year is clearly fraught with danger, but the current situation does suggest that this nascent trend is growing in strength.

|

The trend is even more stark when it comes to LBOs, which are more the domain of the loan market. Here, a staggering 29% of LBOs this year have been bond-only, while the average for the five years before 2021 was just 6%. Again, when looking at bonds plus senior loans combined, high-yield has been used in 43% of LBOs this year, versus just 14% in 2019 and 2020, and an average of 16% for the period 2016-20.

Favorite things

However, while there is a benefit to baking in high-yield financing from a cost-of-debt perspective — not to mention the pricing tension it drives across companies' capital structures, which then brings the cost of loans down — there are other reasons why private equity sponsors will nonetheless continue to favor the loan market where possible. “We always still do loans at these current levels due to call protection on bonds, the cost of preparing an offering memorandum and the cost in terms of management time, and because bonds are not appropriate for carve-outs, which generally don’t have audited stand-alone accounts,” states a sponsor.

Indeed, while bond financing is playing a role more frequently across deals, the issue sizes of loans versus bonds highlight that sponsors prefer to take on as much loan debt as they can. “An eighth or more of a saving on the coupon of a bond is washed away by the first call,” says one banker. “Take SCM Biogroup-LCD — it came at 3.375% on the bonds, but that is not enough of a differential versus E+350 offered at 99.5 on the loans.”

Another reason bankers might prefer to pitch more loan financing is that market’s relative stability versus high-yield. A few weeks ago softer equity markets crept into credit, and reminded many players that there will likely be periods of heightened volatility this year, with high-yield typically far more skittish than loans.

It is though not just secured bonds and term loans that are in competition, but also unsecured bonds and second-lien. Indeed, there is rampant demand for unsecured bonds from liked credits, with anecdotal evidence of numerous such bonds raising books that are more than 6-10x covered. “Demand for unsecured paper has been crazy,” says a banker. “You are seeing it reflected in pricing, with subordination worth just 125 bps in some names”.

Asda this week took that subordination premium even lower, to just 75 basis points, with the sterling five-year secured bonds (representing the largest-ever single tranche bond in the European market, at £2.25 billion) printing at 3.25%, and the accompanying six-year sterling unsecured bonds at 4%.

“If you like the name then you are going to move down the capital structure in this environment to try and generate some excess return,” notes another buysider. “Biogroup offered a 160 bps pick-up for just over a half a turn more leverage.”

|

Such demand is naturally driving unsecured bond yields tighter, and at 4.6% they are currently on average lower than they have been at any point since the start of 2010. Even with second-lien spreads falling sharply though, from a pure pricing perspective, most agree that second lien cannot remotely challenge.

Again though, pricing is not everything, as the ability to pre-place the second-lien tranche remains highly attractive for sponsors, while limited call protection, remaining private, and speed of execution can be worth their weight in gold.