ECONOMICS COMMENTARY — Nov 02, 2023

Worldwide factory prices rise again in October, but wage pressures cool

Global manufacturing prices rose for a third successive month in October, according to the latest JPMorgan Global Manufacturing Purchasing Managers' Index™ (PMI® ) compiled by S&P Global, hint at some renewed upward pressure on consumer price inflation from the industrial sector. However, drilling down into the details provided by survey contributors providers some encouraging news on a moderation in underlying drivers of price hikes, and in particular a cooling of wage-related price pressures.

Global factory prices rise modestly for third month in October

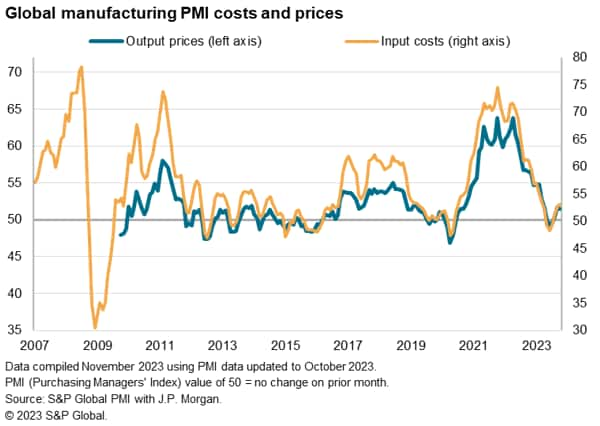

Manufacturers worldwide charged more for their goods on average for a third successive month in October, according to the latest PMI surveys compiled by S&P Global and sponsored by JP Morgan, contrasting with declines recorded over the prior three months. However, the rate of increase remained modest by historical standards. Although the uplift in prices was the second-largest for six months, the rate of increase slipped compared to September to a level in line with the average seen in the five years prior to the pandemic (and only very marginally higher than the pre-pandemic 10-year average).

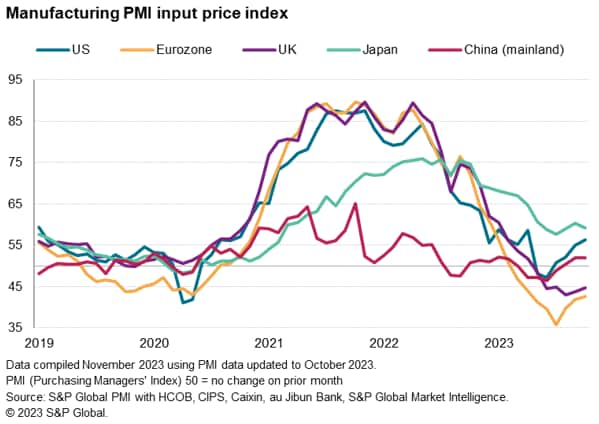

The modest rise in prices reflected higher input costs, which rose in October at the fastest rate for seven months. However, the rate of cost increase remained well below the five- and ten-year pre-pandemic averages, suggesting that cost pressures remain muted by historical standards, in marked contrast to the experience of 2021 and 2022.

Waning wage pressures

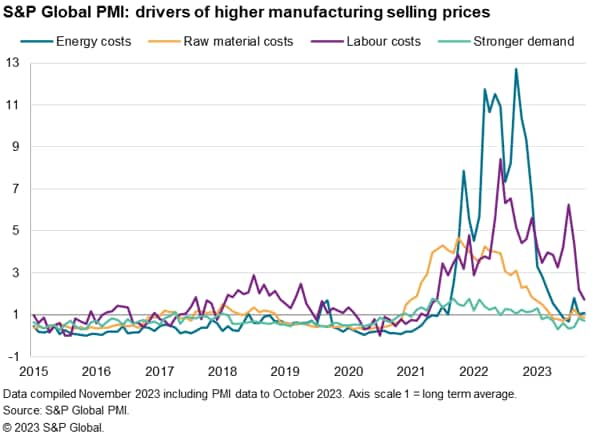

Looking at the reasons cited by manufacturers for higher selling prices in October, there is encouraging news from an inflation-fighting perspective. Despite higher oil prices, overall energy cost pressures remain close to their long-run average, as do other raw material price pressures.

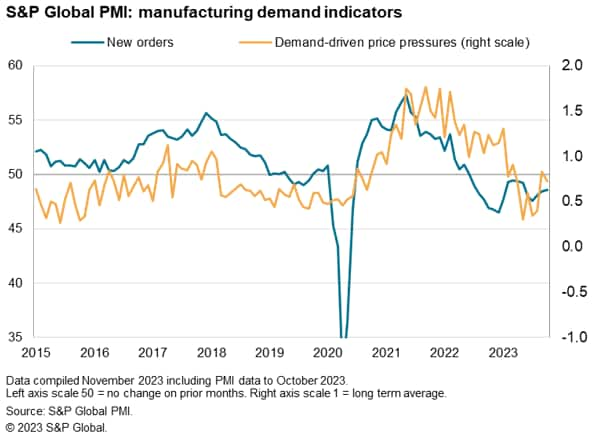

Demand meanwhile remains a drag compared to its long-run average, underscoring a lack of pricing power amid the ongoing manufacturing downturn signalled by the PMI. New orders received by factories have now fallen globally for 16 successive months.

Even more encouraging is the reduced upward pressure from wages. Labour costs had spiked after the pandemic, sustaining higher selling prices into the first half of 2023. But this labour market effect has moderated considerably in recent months, with upward pressure from labour costs diminishing globally in October to its lowest since May 2021.

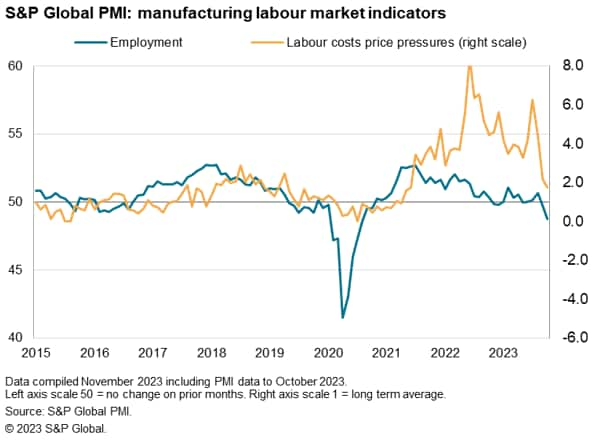

This cooling of wage pressures corresponds with a reduction in demand for labour by manufacturers. Global factory employment fell in October for a second successive month in October, according to the PMI, dropping at a pace not seen since the global financial crisis in 2009, if early pandemic lockdown months are excluded.

Rising prices in the US and Japan contrast with falling European charges

Looking geographically, there are some variations in price trends around the world, though in general, price trends remain muted by historical standards.

Higher costs were most notably recorded in Japan and the US, the latter seeing an accelerated rate of increase, albeit still below the ten-year pre-pandemic average. Costs also rose modestly in mainland China, as well as across Asia as a whole. In contrast, costs fell in both the Eurozone and the UK.

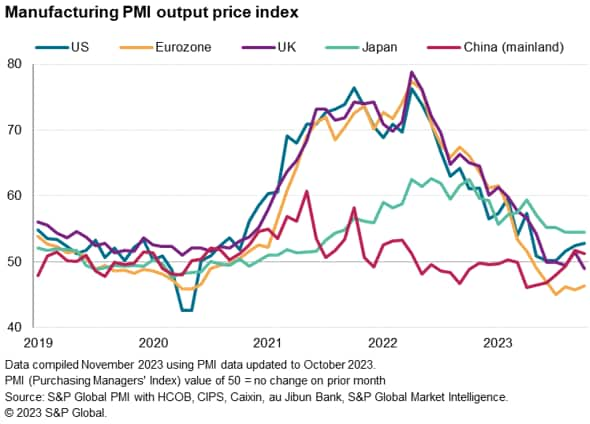

These cost variances were reflected in changing selling price trends. Average prices charged by factories for goods continued to fall sharply in the eurozone and also fell in the UK, the latter reporting the steepest fall since February 2016.

Prices meanwhile rose markedly in Japan and at a rate that was unchanged for the third successive month. The rate of charge inflation across the US was the quickest in six months, though was modest overall. Prices also rose slightly for a second successive month in mainland China, helping to assuage recent deflation concerns.

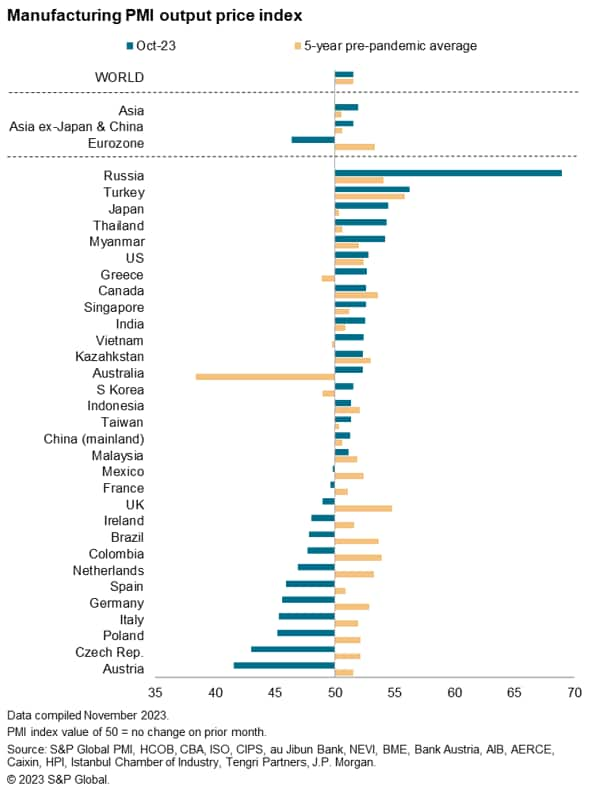

One stand-out during the month was Russia, where prices charged have surged higher in recent months, rising in September and October at rates not seen since early 2015, excluding the initial months following Russia's invasion of Ukraine in February 2022.

Chris Williamson, Chief Business Economist, S&P Global Market Intelligence

Tel: +44 207 260 2329

© 2023, S&P Global. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Location