ECONOMICS COMMENTARY — Jul 24, 2023

United Kingdom flash PMI data point to cooler inflation as economy stalls

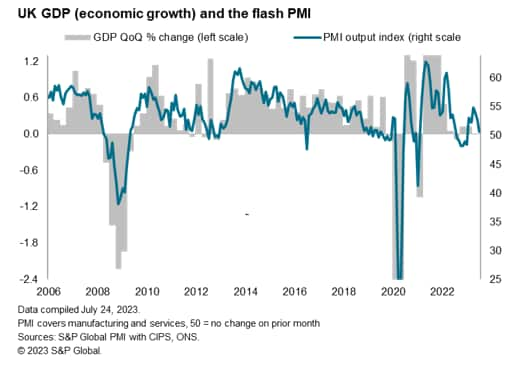

The UK economy has come close to stalling in July which, combined with gloomy forward-looking indicators, reignites recession worries.

July's flash PMI survey data revealed a deepening manufacturing downturn accompanied by a further cooling of the recent resurgence of growth in the service sector.

Rising interest rates and the higher cost of living appear to be taking an increased toll on households, dampening a post-pandemic rebound in spending on leisure activities. Meanwhile, manufacturers are cutting production in response to a worryingly severe downturn in orders, both from domestic and export markets.

Forward-looking indicators, such as order book inflows, levels of work-in-hand and future business expectations, all point to growth weakening further in the months ahead, adding to a risk of GDP falling in the third quarter.

An upside to the deteriorating growth and demand picture is a further cooling of inflationary pressures. Manufacturing prices are falling at an increased rate and service sector inflation is continuing to moderate. Although ongoing upward wage pressures mean service sector price growth remains elevated, the survey data signal further, potentially marked, falls in consumer price inflation in the months ahead.

Economic growth slows

UK business activity growth slowed to close to stalling in July, according to the flash PMI survey data compiled by S&P Global and sponsored by CIPS. Although at 50.7 the survey's headline output gauge remained above the 50.0 no change level to register an expansion of output for a sixth successive month, the rate of growth slowed sharply, cooling for a third successive month to register the weakest expansion since the recent recovery began.

The latest reading is consistent with no change in GDP at the start of the third quarter, adding to the risk of a renewed economic downturn as the economy heads through the second half of the year.

Further weakness ahead is signalled by the survey registering no growth in new orders for goods and services in July, contrasting with the growth in order inflows seen over the prior five months, in turn led by the steepest drop in export orders since last November.

Gloom about near-term prospects was compounded by an increasingly severe decline in outstanding work at companies, which fell for a third successive month in July. Excluding the early pandemic lockdowns, the drop in backlogs of work was the steepest recorded since mid-2016.

The diminishing stock of work-in-hand suggests that companies will seek to reduce operating capacity in the coming months unless demand revives. However, companies are increasingly pessimistic about such a demand revival, with future business expectations dropping in July to their lowest so far this year. Hence employment growth moderated in July, albeit with companies continuing to hire as they often sought to fill long-held vacancies.

Service sector growth wanes alongside deepening manufacturing decline

By sector, July saw the manufacturing downturn deepen while service sector growth near-stalled. The fall in factory production was the steepest since last December while the latest increase in service sector output was the smallest recorded in six months.

Within the service sector, July brought signs of weakness becoming more broad-based. Business activity levels fell sharply for hotels and restaurants and also declined for transportation and business services, the latter registering its first contraction since December. Besides resilient growth for computing and IT, only the financial services sector and 'other consumer services' saw higher levels of activity in July, with the financial sectors seeing a notable slowing in the rate of expansion to the lowest seen so far this year.

Trends in backlogs of work meanwhile deteriorated in both sectors, with factory backlogs slumping at a rate not seen since December and services backlogs showing the steepest decline since the lockdowns of early 2021.

While manufacturing employment is already being reduced in response to the deteriorating order book picture, service sector hiring continued to show resilience, albeit with the rate of job creation moderating slightly and looking prone to a further weakening barring a revival of order book growth.

Inflation pressures continue to cool

Price pressures meanwhile continued to cool in July, albeit showing pockets of resilience, notably in the service sector.

Looking first at input costs, the combination of improved supply availability and deteriorating demand led to a third successive monthly drop in manufacturing input prices, the rate of decline of which accelerated to the steepest since February 2016. Suppliers' delivery times shortened to the greatest extent since data were first available in 1992, and the purchasing of inputs by factories fell at a rate not seen since the global financial crisis in 2009 if the early lockdown months of 2020 are excluded.

Service sector input costs meanwhile continued to rise at a rate well above the pre-pandemic average, buoyed principally by rising wage pressures and higher interest rates, though even here the rate of increase moderated to the lowest since May 2021. The strongest rates of increase were seen in financial services and hotels & restaurants.

Selling price inflation likewise moderated. Average prices charged for goods fell for a second straight month, dropping at a rate not seen since February 2016. While average prices charged for services continued to rise at an elevated rate, far higher than anything seen prior to the pandemic, the rate of inflation slowed sharply to the lowest since August 2021.

Measured across both goods and services, the rise in both average input costs and selling prices in July was consequently the lowest recorded since February 2021.

Absent any major shocks, the survey's selling price gauge is consistent with consumer price inflation (CPI) moderating from the current 7.9% rate in the coming months, falling closer to 6% by the start of the fourth quarter and to around 4% into the start of 2024.

Rate hike speculation to moderate

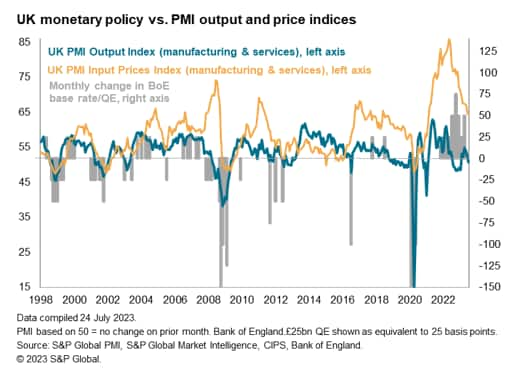

The flash July PMI data come on the heels of a 50 basis point hike in interest rates by the Bank of England in late June. The latest rise takes the main policy rate to 5.0%, its highest since 2008.

Since the latest rate hike, inflation surprised to the downside, albeit merely dropping in line with the signal from the June PMI. The inflation decline meant investors have pencilled-in a 25 basis point hike at the Monetary Policy Committee's next meeting on 3rd August rather than a 50 basis point hike. With the flash July PMI numbers hinting at a further, potentially marked, decline in inflation, as well as a growing risk of the economy falling into decline in the coming months, there will be mounting speculation that interest rates could peak in August.

Note that the PMIs output gauge is now in territory more associated with a lowering of interest rates rather than a hike. While the survey's input price gauge remains elevated, it is clearly moving lower.

Access the press release here.

Chris Williamson, Chief Business Economist, S&P Global Market Intelligence

Tel: +44 207 260 2329

© 2023, S&P Global. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Location