Research — Oct 11, 2024

Lower rates spell modest funding relief for US banks

By Nathan Stovall and Zain Tariq

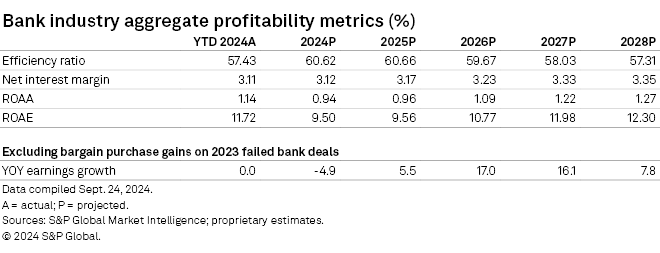

Lower interest rates should alleviate pressure on funding costs and allow for net interest margins to expand, while serving as a modest positive for bank credit quality.

The Federal Reserve's pivot to lower interest rates will provide relief to banks' deposit business and allow institutions to reduce deposit costs. The decline will be slower than what banks experienced when interest rates began to rise, but the decrease will still be material enough to allow for net interest margins to expand. Higher credit costs will serve as a headwind to bank earnings, but lower rates will provide some relief for strained borrowers and prevent credit quality from seriously challenging most institutions' balance sheets.

Click here to access data exhibits and the US banking industry's projections template.

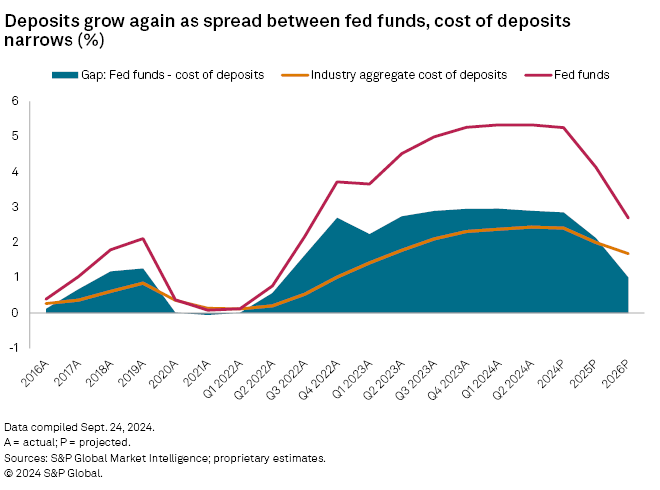

Funding pressures easing but not as quickly as they began

Deposit costs rose modestly in the second quarter as funds continued to shift into higher-cost deposits such as certificates of deposits, or CDs. The Fed was on hold during the second quarter and intermediate rates actually rose in the period, but customers remained rate sensitive.

Some banks tried to lower deposit rates in the period as the prospect of the Fed's shift in monetary policy lied on the horizon. As some banks tested the waters with lower rates and became less competitive with alternatives in the Treasury and money markets, nonbrokered deposits actually declined in the second quarter.

Across the industry, the difference between the average fed funds rate and the industry's cost of deposits narrowed modestly in the second quarter and should decline further in the second half of 2024. Banks will be more competitive with higher-yielding alternatives now that the Fed has begun its easing campaign and intermediate rates have fallen considerably, allowing core deposit growth to return.

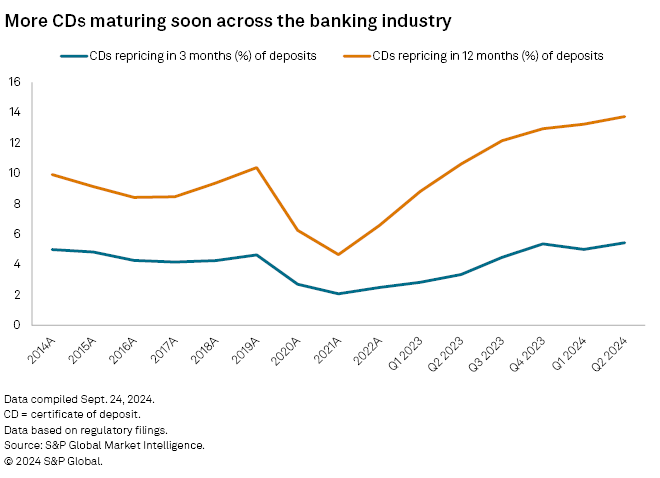

Deposit costs will not necessarily decline quickly for all banks though as most institutions significantly increased their reliance on CDs for funding. CDs grew to 15.8% of deposits by the end of the second quarter, up from 15.5% in the first quarter and 13.1% a year earlier.

Many of those products carry one-year terms, meaning that institutions might not feel pricing relief for some time. At the end of the second quarter, the bulk of CDs were set to mature in the next year, with 62.6% of all CDs maturing or repricing in the next three months, while 86.5% of CDs were set to mature in the next 12 months. At the end of the second quarter of 2024, CDs maturing in the next three months equated to 5.4% of the industry's deposits, while CDs maturing in the next 12 months equated to 13.7% of the industry's deposits.

When those CDs mature, most banks will have to meet market rates to retain the deposit. While the market has waited for lower rates for some time, CDs only began declining late in the third quarter. At Sept. 29, 788 banks marketed one-year CDs with annual percentage yields over 4%. That is down from 908 banks at Sept. 8. However, the number of banks marketing CDs at that level in early September was roughly flat with the level seen at the end of the second quarter, when 928 banks marketed CDs with APYs over 4% at June 28.

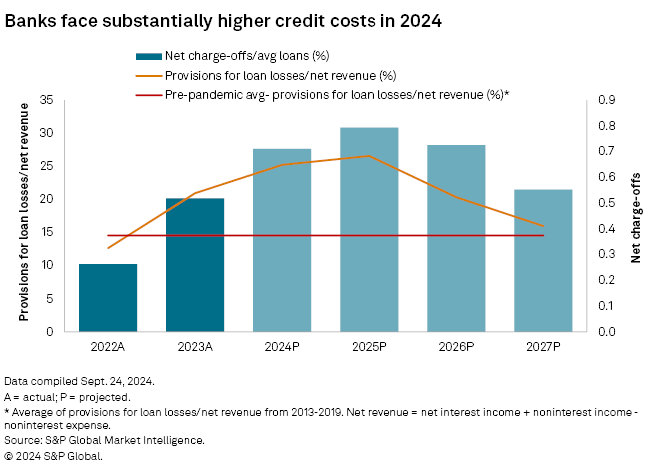

Credit costs continue normalization trend

Credit costs grinded higher in the first and second quarters and should deteriorate further in the second half of 2024 and into 2025 as stress from substantially higher rates begins to weigh on borrowers, particularly in the commercial real estate (CRE) segment.

While we do not expect considerable deterioration in credit quality, we anticipate greater delinquencies and charge-offs in the future. Banks have tried to prepare for slippage by tightening lending standards and building reserves for loan losses.

We expect relatively slow loan growth in 2024 as institutions approach new originations more cautiously and face pressure from their regulators to do so. We also expect banks to continue to build reserves as they work to shore up their balance sheets to clear any potential hurdles ahead.

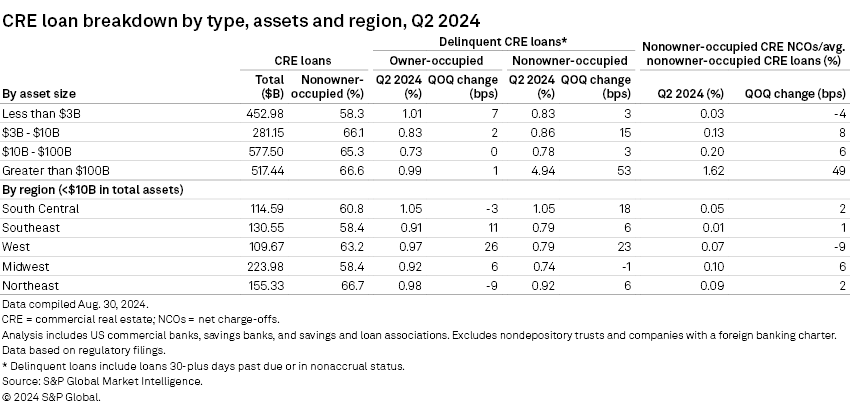

CRE delinquencies have risen off historically low bases as well, increasing for seven straight quarters to the highest level in nearly a decade. However, the growth in problem credits have been driven by delinquencies in nonowner-occupied CRE loans — loans to landlords as opposed to owner-occupied CRE loans, which are effectively business loans collateralized by CRE — have risen far more, increasing to 2.03% of those loans in the second quarter from 1.16% a year ago compared to 0.89% on owner-occupied credits in the second quarter, up from 0.74% a year earlier.

The slippage in credit quality of nonowner-occupied loans has been far, far greater for the nation's biggest banks, which have the scale to make loans against the properties of the greatest concern such as high-rise offices.

Banks have increased reserves against their CRE portfolios, particularly related to office credits, where large banks such as Wells Fargo & Co., PNC Financial Services Group Inc., Truist Financial Corp. and Citizens Financial Group Inc. have built reserves to 8% or more of their office portfolios. Losses on CRE portfolios have also risen but remain well below levels witnessed during the Great Recession.

Loss content will be location specific and differ across the subcategories of the asset class, but banks will feel some pain in their commercial real estate books, particularly as borrowers seeking to refinance maturing credits find it more difficult to access credit, or they will at least face a significantly higher debt service given the increase in interest rates.

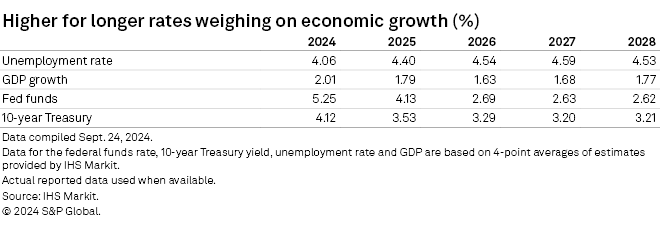

In fact, when examining property records nationwide, the average rates on loans originated in 2024 through the first half of the year was 6.2% compared to the rate on mortgages maturing of 4.3%, a jump of nearly 200 basis points. Decreases in interest rates in the second half of 2024 should reduce the hit of the higher debt service, but some of the properties associated with those credits are also producing weaker cash flows given the shift to hybrid work.

We expect that refinancing test to result in defaults and notably higher loss content in 2024, with net charge-offs jumping off relatively benign levels. We expect loss content to linger as banks provide borrowers with extensions in the face of some maturity walls. Some of those extensions might provide borrowers or their lenders the ability to reduce losses by working them over time, but other properties, particularly class B and class C office properties in center city areas will bring notable losses.

However, many banks have already set aside considerable reserves for the most troubled projects. And even though net charge-offs will rise significantly in the coming years, losses and the reserves required to fund them should serve as a headwind to earnings as opposed to the headwind that would occur during a severe downturn.

We expect provisions to rise to 25.2% of net revenue in 2024, up from 21.3% through first half of the year and 20.9% in 2023. From 2013 to 2019, banks' provisions equated to 14.6% of net revenue on average.

Scope and methodology

The outlook discussed in this article is based on a proprietary S&P Global Market Intelligence model that utilizes the actual results of nearly 10,000 active and historical commercial and savings banks and savings and loan associations. The outlook is based on management commentary, discussions with industry sources, regression analysis, and asset and liability repricing data disclosed in banks' quarterly call reports. While taking into consideration historical growth rates, the analysis often excludes the significant volatility experienced in the years around the credit crisis.

The outlook is subject to change, perhaps materially, based on adjustments to the consensus expectations for interest rates, unemployment and economic growth. The projections can be updated or revised at any time as developments warrant, particularly when material changes occur.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.