BLOG — May 13, 2021

Indonesia’s consumers remain sidelined hampering economic recovery

By Bree Neff

- The economic recovery in Indonesia is underway with support from government spending and exports.

- Further economic momentum will be dependent on private consumption, but if consumer inflation and labor market data are any indication, households are not yet ready to carry the economy and may feel the economic recovery is passing them by.

- The government and central bank have largely tapped out their options for pushing the economic recovery along, after implementing significant stimulus measures in 2020.

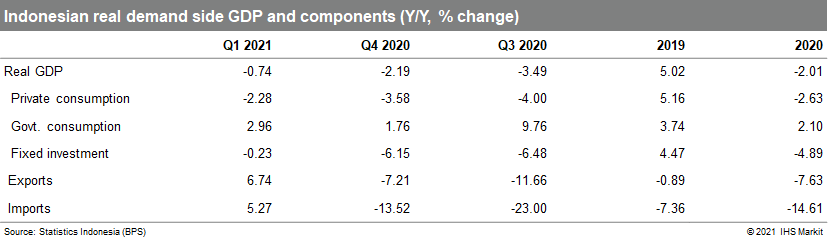

The Indonesian economy contracted 0.74% year on year (y/y) in the first quarter of 2021, up from a 2.2% y/y contraction the previous quarter, supported by ramped up government spending, a stronger recovery in fixed investment, and healthy exports. Lagging in the recovery was private consumption.

The first quarter GDP result was peppered with good news including the government managing to roll over programs as part of the National Economic Recovery stimulus program (known locally as PEN) which had underspent versus plan in 2020. This allowed government consumption spending to expand at a faster-than-usual pace at the start of the fiscal year. It is understood that PEN spending through 30 April 2021 reached 22.3% of its 699.4 trillion Indonesian rupiah (USD 48.4 billion) 2021 budget, with spending on corporate support programs, business incentives, and social assistance programs accounting for much of the spending and providing an extra boost to growth.

Fixed investment activity also beat expectations during the first quarter with real (inflation-adjusted) spending on machinery and equipment and transportation both returning to year on year growth after machinery and equipment spending has contracted for five consecutive quarters and transportation investment has contracted since the first quarter of 2019. Building activity remained subdued, contracting 0.7% y/y as costly and labor-intensive construction projects likely faced delays.

Also positive for the economy, exports of goods in real terms surged to 11.8% q/q, or the strongest expansion since a one-off surge in the third quarter of 2017, and prior to that 2011. The recovery was led by stronger demand from mainland China and major advanced economies boosting demand for a wide range of Indonesian commodities including oil and gas exports.

Unfortunately, the COVID-19 pandemic continued to weigh heavily on private consumption during the quarter. Firstly, there was a progressive scaling up of COVID-19 containment measures in the first quarter. It should be noted that the measures are far from full lockdown and vary down to the micro (neighborhood) level dependent on the prevalence of COVID-19 infections, but they did limit mobility and availability of work. Additionally, semi-annual data on employment from Statistics Indonesia indicates that as of February 2021, 1.62 million people have lost their formal sector jobs and 15.7 million people are working reduced hours, implying reduced household incomes and hence, spending capacity.

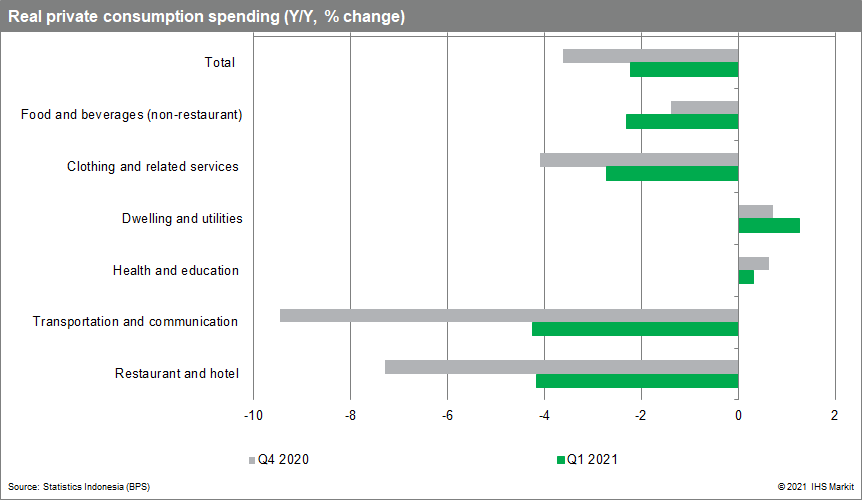

As a result, private consumption spending remained weak across all major spending categories during the first quarter with only marginal easing of year-on-year contractions for transportation and communication and restaurant and hotel spending supporting the minor improvement in the headline private consumption figure. Meanwhile, private consumption spending on food and beverages weakened further contracting 2.3% y/y, down from the fourth quarter's 1.4% y/y contraction.

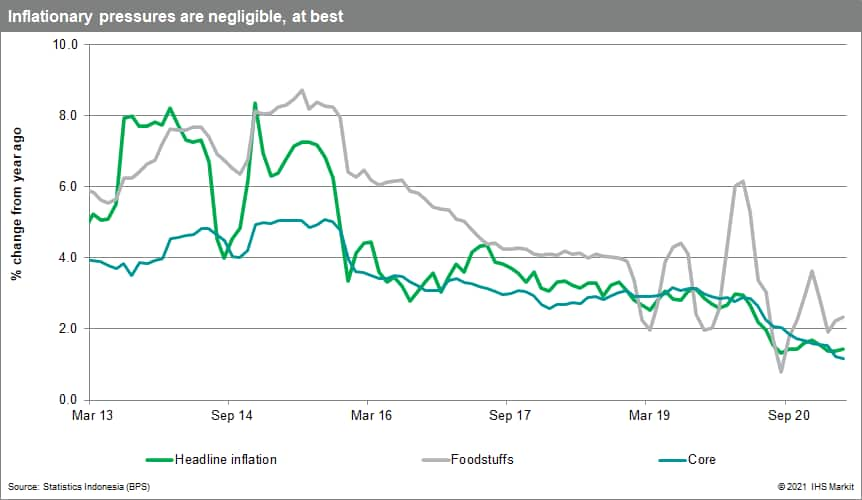

Unfortunately, headline consumer price inflation for April hinted at sustained weak consumer demand as it held steady at 1.4% y/y for a third consecutive month according to Statistics Indonesia and core inflation (which excludes government-controlled and volatile food prices) hovered for a second consecutive month at the record-low 1.2% y/y. There was minor upward pressure on food prices during the month, which may pick up modestly further as Eid al-Fitr is celebrated in May; otherwise, price increases were relatively modest across the other major components of the Consumer Price Index (CPI) indicating limited demand pressures.

Further economic momentum will be slow to build, especially as households remain on the sidelines due to containment measures, reduced incomes and the uncertainty caused by the persistence of the COVID-19 virus in the country. The vaccination campaign is rolling out as fast as it can with 22 million doses administered as of 9 May. However, this is not fast enough for a campaign that aims to vaccinate 180 million people by March 2022, and may not be sufficient to allow COVID-19 containment measures to be relaxed soon.

The government has also cut the length of the Eid-al-Fitr holiday this year and has prohibited travel back to hometowns, dampening a typical period of high consumption for the country. Therefore, IHS Markit projects Indonesia's GDP growth will come in around the high-3% range for 2021. Aside from concerns about the recovery for private consumption, our pessimistic outlook is driven by concerns that the policy space is shrinking for additional stimulus measures.

On the fiscal side, the government has significantly ramped up its PEN spending for this year and expects to return a fiscal deficit on the order of 5.7% of GDP, but there are limits on the administrative capacity front for this level of spending. Additionally, with foreign demand for Indonesian government debt subject to risk of vacillating investor risk aversion, higher fiscal deficits are out of the question. On the monetary side, Bank Indonesia's capacity to cut the policy interest rate further- after 150 basis points worth of cuts since the start of the pandemic- is hampered by the need to maintain rupiah stability. Instead, the central bank will continue using moral suasion to urge lenders to lower their lending rates while seeking to ease other macroprudential regulations where possible to boost lending.