BLOG — Jan 10, 2022

Daily Global Market Summary - 10 January 2022

By Chris Fenske

All major European and most US equity indices closed lower, while APAC markets were mixed. US government bonds closed mixed with the curve flatter on the day, tax exempt US municipal bonds closed lower for a third consecutive day, and benchmark European bonds closed mixed. European iTraxx closed wider on the day across IG and high yield, while CDX-NA was flat on the day. The US dollar, natural gas, and gold were higher on the day, while oil and copper closed lower.

Please note that we are now including a link to the profiles of contributing authors who are available for one-on-one discussions through our Experts by IHS Markit platform.

Americas

- Most major US equity indices closed lower except for Nasdaq +0.1%; S&P 500 -0.1%, Russell 2000 -0.4%, and DJIA -0.5%.

- 10yr US govt bonds closed flat/1.77% and 30yr bonds -3bps/2.09% yield.

- CDX-NAIG closed flat/53bps and CDX-NAHY flat/308bps.

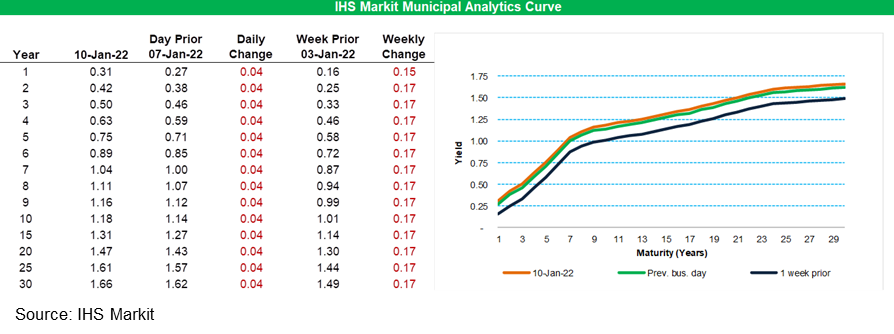

- IHS Markit's AAA Tax-Exempt Municipal Analytics Curve (MAC) sold-off 4bps across the curve, with the curve 15-17bps worse week-over-week.

- DXY US dollar index closed +0.3%/95.99.

- Gold closed +0.1%/$1,799 per troy oz, silver +0.2%/$22.46 per troy oz, and copper -1.3%/$4.35 per pound.

- Crude oil closed -0.8%/$78.23 per barrel and natural gas closed +2.9%/$3.83 per mmbtu

- Municipal bond buyside accounts are set to welcome greater par size follow a lighter calendar to start the new year after $2 billion of new issue supply priced across the course of last week, falling well beneath investor demand given the mounting sideline capital ready to be deployed across state and local credits. The Department of Airports of the City of Los Angeles (Aa3/AA-/AA-) led last week's negotiated calendar selling $504 million of subordinate revenue bonds with significant cuts noted across the scale following wide movements noted across muni benchmarks resulting in cuts of 7-10bps across the intermediate range of the scale, providing allotted investors a yield of 1.58% (+45bps off the interpolated MAC) in the 2032 maturity. The City of San Antonio, TX (Aa2/AA/AA) also tapped into the negotiated market to price $78 million of revenue refunding bonds with maturities spanning 05/2029-05/2042 with robust investor demand suppressing yields by 2-9bps across select maturities with the greatest bumps noted in the short term maturities available. This week's calendar is set to return to larger weekly volume levels, presenting investors $8.8 billion pricing across 198 new issue deals with the Board of Education of The City of Chicago, IL (-/-/BB+/BBB) leading the negotiated calendar to sell $863 million of dedicated revenue bonds with maturities spanning 12/2035-12/2047 selling on Thursday 01/13 and senior managed by Goldman Sachs. The State of Louisiana (Aa2/AA-/-) will also tap into the negotiated arena to price $651 million of taxable gasoline and fuel tax revenue refunding bonds, senior managed by Wells Fargo. This week's competitive calendar will span across 116 new issues for a total of $3.3 billion, led by the State of Colorado auctioning $400 million education loan program tax and revenue notes across a single maturity, selling on Wednesday 01/12. (IHS Markit Global Market Group's Matthew Gerstenfeld)

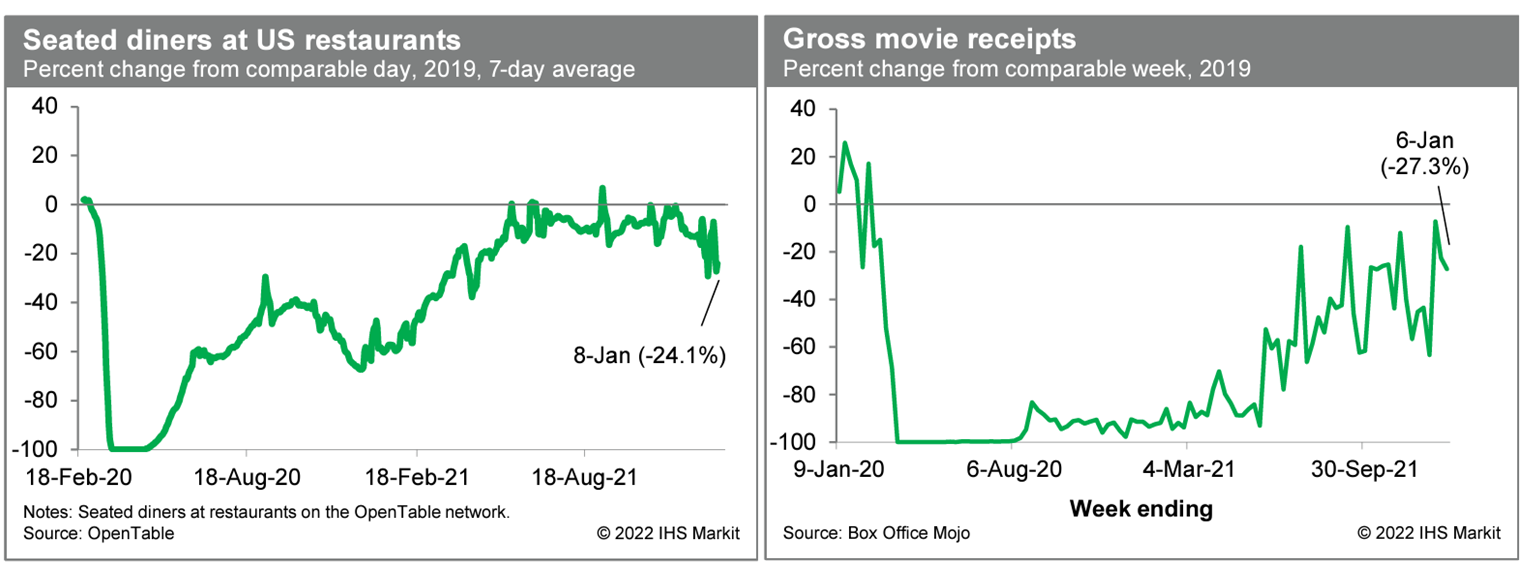

- Averaged over the last seven days, the count of seated diners on the OpenTable platform was 24.1% below the comparable period in 2019. This indicator has been volatile over the last couple of weeks but is nevertheless suggestive of heightened caution on the part of would-be diners. Meanwhile, box office receipts last week were 27.3% below the comparable week in 2019. This is in the upper half of a recent range and suggests that Omicron has yet to have a material impact on movie theater activity. (IHS Markit Economist Ben Herzon and Lawrence Nelson)

- Novel, biodegradable fibers that release antimicrobial compounds when triggered by bacterial enzymes or critical increases in relative humidity might lead to food producers' holy grail of environmentally friendly packaging materials that extend product shelf life and diminish the risks of food poisoning by combatting the likes of fungi, E. coli, and Listeria. (IHS Markit Food and Agricultural Policy's William Schulz)

- The cellulosic nanofibers, which can be deposited as a functional layer of food packaging materials, were developed by researchers at Harvard University's T.H. Chan School of Public Health and the Nanyang Technological University (NTU) in Singapore. They are created with an industrial method known as electrospinning that produces fibers by using electric force to draw charged threads of polymer solutions into tubes.

- The multi-stimuli-responsive fibers the Harvard-NTU team developed consist of cellulose nanocrystals, corn protein zein, and starch. Electrospinning allows incorporation of nature-derived antimicrobial active ingredients (AI) such as thyme oil, citric acid, and nisin, as well as cyclodextrin-inclusion complexes of thyme oil, sorbic acid and nisin. The ingredients all meet FDA's standard of Generally Recognized as Safe (GRAS), researchers say.

- "Food safety and waste have become a major societal challenge of our times with immense public health and economic impact which compromises food security," says Philip Demokritou, a professor of environmental health and co-director of the NTU-Harvard Initiative on Sustainable Nanotechnology. "One of the most efficient ways to enhance food safety and reduce spoilage and waste is to develop efficient, biodegradable, nontoxic food-packaging materials. In this study, we used nature-derived compounds including biopolymers, nontoxic solvents, and nature-inspired antimicrobials and developed scalable systems to synthesize smart antimicrobial materials."

- The packaging industry is the largest and growing consumer of synthetic plastics derived from fossil fuels, Demokritou says, with food packaging plastics accounting for the bulk of plastic waste in the environment.

- The study notes that synthetic, petroleum-based polymers are widely used as food packaging materials because of their low cost, excellent gas barrier, and mechanical properties. But incorporating AIs in these materials has not been successful due to poor antimicrobial performance related to the materials' low surface-to-volume ratio, and "potential negative sensory effects."

- Navitas Midstream Holdings LLC announced January 10 it has sold 100% of its interests in Navitas Midstream Partners LLC, a Midland Basin gas gatherer and processor, to Enterprise Products Partners for $3.25 billion in cash. (IHS Markit PointLogic's Annalisa Kraft)

- Navitas said the deal for the Warburg Pincus portfolio company is expected to close in the first quarter. The company's assets include 1,750 miles of pipeline and more than 1 Bcf/d of processing capacity once the Leiken plant comes in service in the first quarter of 2022.

- An Enterprise release stated the acquisition provides it a toehold in the Midland Basin. "This acquisition provides Enterprise's natural gas processing and NGL business with an entry point into the Midland Basin, one of the most economic and prolific crude oil regions in the United States. Drilling activity in the Midland Basin currently represents approximately 20 percent of active onshore drilling rigs in the U.S. The system is anchored by long-term contracts and acreage dedications with a diverse group of over forty independent and publicly owned producers.

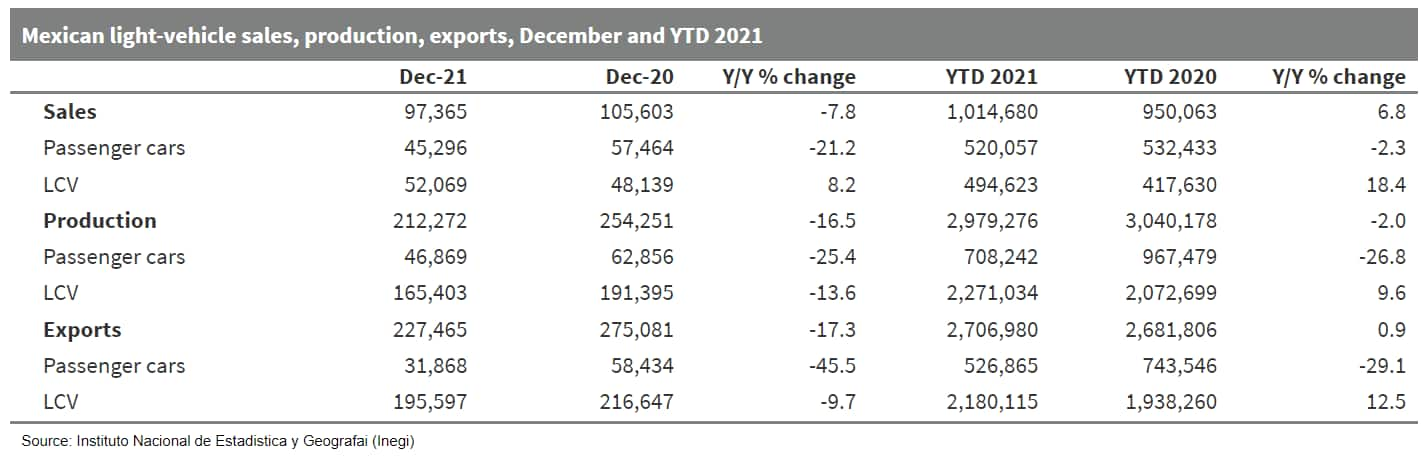

- In December 2021, the impact of the semiconductor shortage continued to constrain sales, production and exports in Mexico; in the full year, sales improved 6.8% y/y, exports were up 0.9% and production declined 2.0%. In 2021, Mexican light-vehicle sales results varied through the year. In 2021, there were market challenges in the first two months, followed by high y/y improvements for several months based on comparisons with the weak results in the corresponding periods of 2020. In the second half of 2021, the semiconductor and other supply chain issues constrained light-vehicle production, exports, and sales. These issues are expected to constrain production throughout 2022. With sales and production constrained in 2021 and 2022, a release of pent-up demand is expected to bring sales improvements in 2023 and 2024. In 2022, although light-vehicle production is forecast to improve compared with 2021, it is not expected to reach the pre-pandemic volume of 2019 until 2023. (IHS Markit AutoIntelligence's Stephanie Brinley)

- At its monthly meeting in January, the Peruvian central bank lifted its key policy interest rate by 50 basis points for the fifth consecutive month, bringing the rate to 3.0%. (IHS Markit Economist Jeremy Smith)

- The monthly Banco Central de Reserva del Perú (BCRP) policy communique contains substantial shifts in tone and language that signals an intention to pursue faster monetary tightening relative to its earlier forward guidance.

- Although the BCRP had previously planned to maintain an "expansionary monetary policy for a prolonged period" with a "gradual withdrawal of monetary stimulus", it now deems it appropriate to "continue with the normalization of monetary policy in the coming months". The January statement has no mention of "expansionary monetary policy" and has removed prior statements clarifying that recent rate hikes need not imply a "cycle of successive [policy rate] increases".

- Nonetheless, the BCRP continues to characterize above-target inflation as "transitory", projecting a return to the 1-3% target range in the fourth quarter of 2022. It maintains this view despite an above-expectation consumer price increase in December 2021, which pushed year-on-year inflation to the highest point in 13 years.

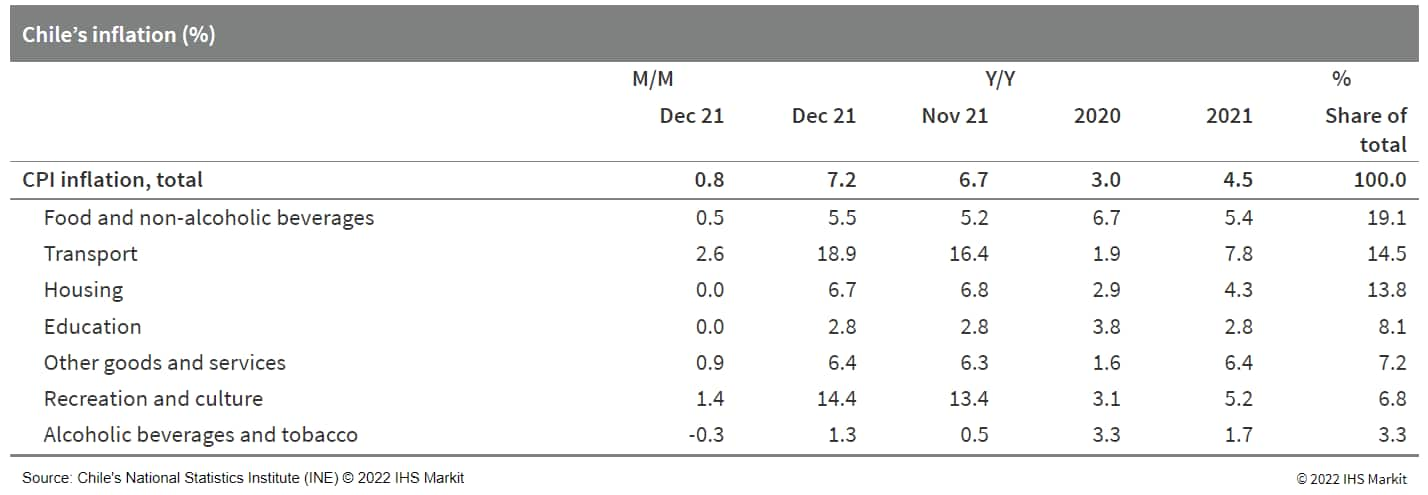

- Chile's month-on-month (m/m) consumer price inflation rate accelerated during December 2021 following a deceleration in the prior month, closing 2021 at 7.2% annual inflation - the highest reading in 13 years. (IHS Markit Economist Claudia Wehbe)

- According to Chile's National Institute of Statistics (Instituto Nacional de Estadísticas: INE), the country's consumer price inflation rate stood at 0.8% m/m in December 2021, accelerating from 0.5% m/m recorded in the prior month, driven mainly by increases in the costs of transportation and food and non-alcoholic beverages. Prices rose in eight of the 12 basket components, while housing and education were unchanged.

- Following the modest November increase, transportation costs jumped in December 2021 mainly because of increases in the costs of ground transportation of passengers, as well as in petrol and lubricant oils for household vehicles. Prices also jumped in the food and non-alcoholic category after a very small upward move in November, largely driven by increases in meats, breads, and cereals. Meanwhile, a drop in the alcoholic beverages and tobacco category partially offset the overall monthly cost increase.

Europe/Middle East/Africa

- All major European equity markets closed lower; Spain -0.5%, UK -0.5%, Italy -1.0%, Germany -1.1%, and France -1.4%.

- 10yr European govt bonds closed mixed; Italy -4bps, France -1bp, Spain flat, and Germany/UK +1bp.

- iTraxx-Europe closed +1bp/52bps and iTraxx-Xover +4bps/257bps.

- Brent crude closed -1.1%/$80.87 per barrel.

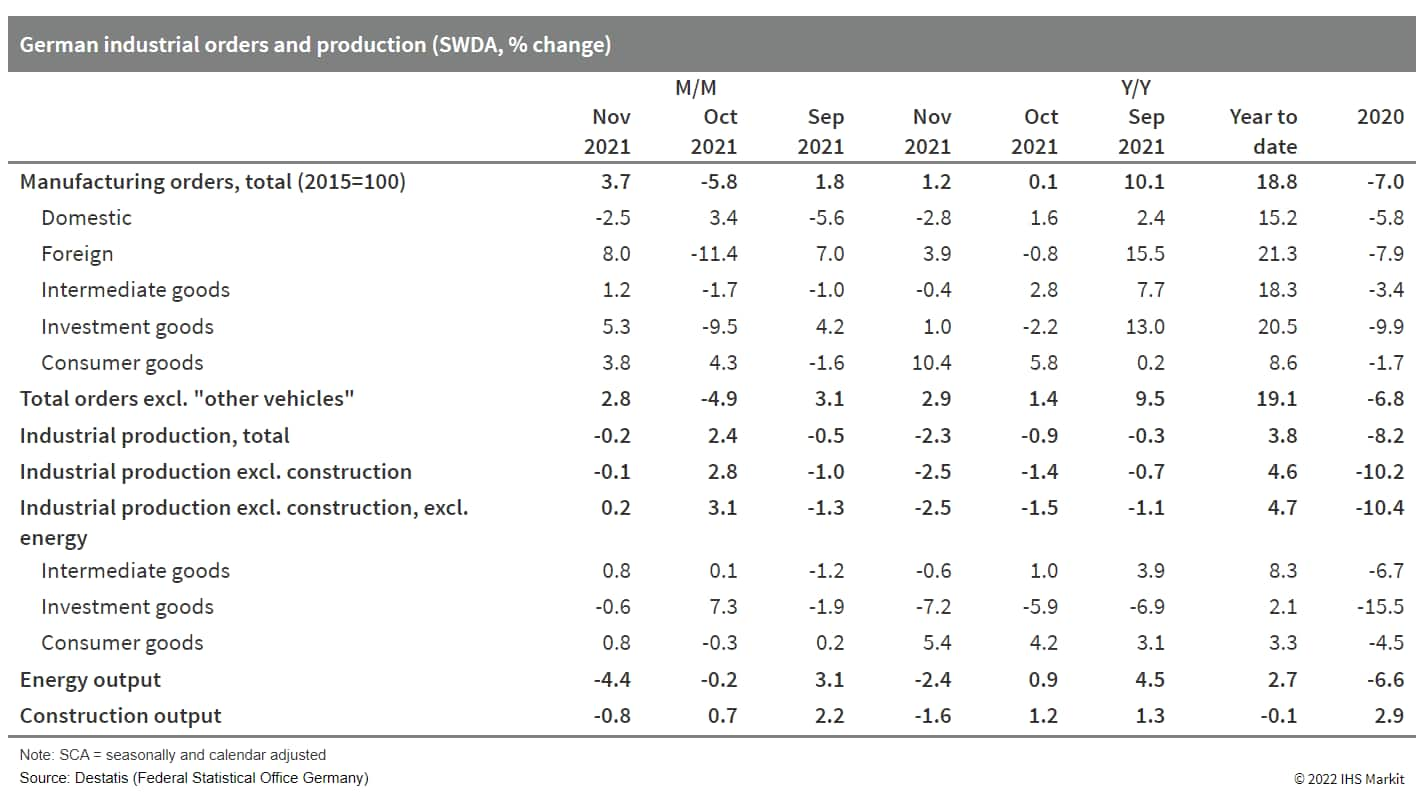

- Seasonally and calendar-adjusted German industrial production excluding construction did not correct for October's unexpectedly large rebound in November, rather remaining broadly flat. Nevertheless, the latest output level thus remained almost 8% below its February 2020 pre-pandemic high. (IHS Markit Economist Timo Klein)

- Total production including construction was slightly weaker in November due to a dip by 0.8% month on month (m/m) of construction output. Energy production declined even more (-4.4% m/m). Since mid-2018, and especially during the pandemic, construction has been a supportive force for overall production, but this was no longer the case during October-November.

- The split by type of good reveals that the production of intermediate and consumer goods each increased by 0.8% m/m while investment goods output slipped slightly (-0.6%), but to a much lesser extent than feared after October's spike by 7.3% m/m. Intermediate goods remain on a sideways path for now, having declined during June-September 2021. Consumer goods production has shown a sideways tendency since September already. The interim loosening of COVID-19 restrictions since May 2021 boosted the recovery for about three months before losing momentum.

- The November breakdown by industrial branch reveals that motor vehicle production managed to strengthen for the third consecutive month in November, approaching the mid-2021 levels seen prior to the major drop in August (-19.6% m/m). This is still about 30% below its pre-pandemic level, however, reflecting ongoing issues with the availability of semiconductors. In other sectors, production of chemicals/pharmaceuticals sector also increased strongly at 4.0% m/m, unwinding its October setback and therefore resuming its outperformance versus industry as a whole observed during August and September. In contrast, machinery and equipment (-3.6% m/m) and the electronic and electric equipment sector (-1.7%) did less well in November, returning to the pronounced weakness seen during August and September.

- Meanwhile, manufacturing orders continue to display even greater volatility. November's 3.7% m/m rise recoups part of October's plunge of -5.8% m/m, just like September (1.8%) had unwound part of the steep fall in August (-8.8%). The net decline in orders in recent months has corrected for the almost uninterrupted build-up of demand since May 2020, however, so that November's orders level is about 7% above that of February 2020, just before the pandemic took hold. This contrasts with the 8% shortfall noted above for production ex-construction. In fact, October's accumulated stock of orders, a separate statistic, was even 26% higher than in February 2020.

- TotalEnergies opened late last year the second phase of its battery energy storage system (BESS) facility in Dunkirk in northern France, bringing its capacity to 61 MW, the largest site in the nation and part of a gradual increase in storage nationally. The project, known as Dunkirk II, adds to the 25 MW capacity of Dunkirk I, both located at a TotalEnergies oil refinery that's been repurposed for biofuels production and an LNG import terminal. Dunkirk II consists of 27 lithium-ion BESS units supplied by Saft Batteries. (IHS Markit Net-Zero Business Daily's Kevin Adler)

- TotalEnergies has two more BESS properties under development in France that will bring the company's storage capacity to 129 MW countrywide by the end of 2022, the energy major said on 22 December. Those sites are Carling in northeast France (25 MW) and Grandpuits in north-central France (43 MW).

- France lags behind Germany and the UK in battery storage capacity among European nations, with more than 800 MW of capacity, including the addition in 2021 of about 170 MW, according to IHS Markit. (The UK has about 12,000 MW of installed battery storage, and Germany more than 31,000 MW, according to IHS Markit's Energy Storage Geographic Profiles published last year.)

- IHS Markit says that new installations of battery storage systems in France in 2022 could top 200 MW.

- Speaking to Net-Zero Business Daily by email, George Hilton, IHS Markit energy storage senior analyst, said the industry in France is benefiting from new regulations that opened "access to multiple revenue streams" to pay for the installations. Most important among those streams is the long-term capacity auction known as AOLT, which provides generators and storage companies a guaranteed price for energy for seven years.

- AOLT bids were made through the Ministry for the Ecological and Inclusive Transition in February 2020, which yielded winning bids for 253 MW of new storage capacity through 2028.

- RTE is making progress on a major battery storage project of its own, Project RINGO, which will ultimately deploy 100 MW of new storage at three sites. Its initial investment is €80 million ($95 million), the grid operator said when detailing the program in August. Unlike TotalEnergies, RTE is pairing its storage directly with renewable power installations: wind farms in Vingeanne in eastern France; wind and solar sites in Bellac in the west; and solar sites in Ventavon in the southeast. Construction began in April 2021 at Vingeanne, and the first installation could be completed in the first quarter of 2022.

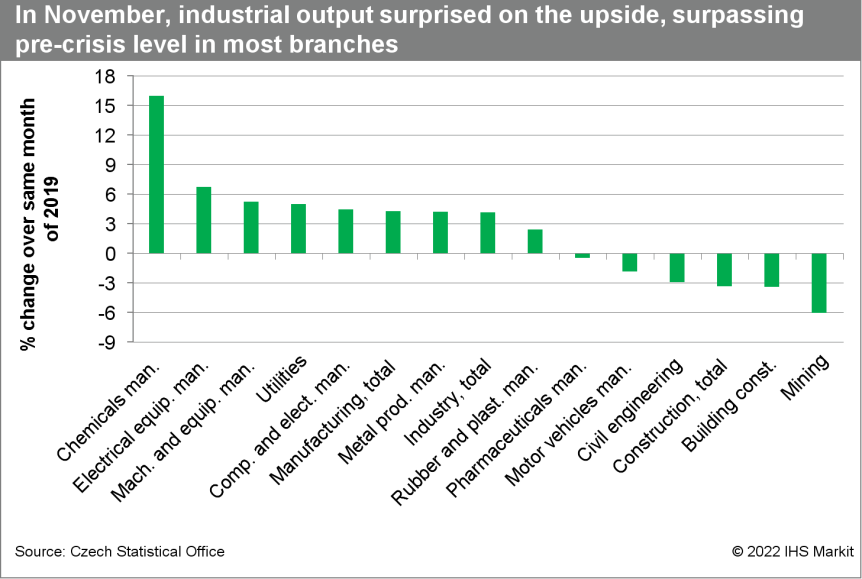

- Seasonally adjusted Czech production surged 4.9% month on month (m/m) in November, recovering to the level from February 2020, before the pandemic. While industrial results were favorable, construction activity continued to disappoint. (IHS Markit Economist Sharon Fisher)

- Working-day-adjusted industrial production rose 1.6% year on year (y/y) in November, driven by machinery and equipment (up 11.3% y/y), utilities (up 5.2%), and food (up 10.5%). Although motor vehicles output continued to decline, the drop (at 7.0% y/y) was much less severe than in August-October, when it plunged about 30% y/y.

- The value of new industrial orders surged 9.3% y/y in November, with export orders up 10.5% y/y, the fastest rate since July. Industrial orders were boosted by strong demand for basic metals, metal products, and chemicals, while automotive orders fell only slightly.

- In other encouraging news, Czechia's trade balance shifted to a small surplus in November after five straight months in deficit. Nevertheless, exports (up 8.1% y/y) continued to rise slower than imports (up 17.1%), as the latter were boosted by higher prices of fuel and natural gas.

- Construction activity continued to disappoint on the downside in November, rising 2.0% y/y, while seasonally adjusted results remained at the October level. Although building construction rose 5.1% y/y, output from the civil engineering sector fell 4.0% y/y.

- On the labor front, employment in industry was flat in a y/y comparison in November, while average monthly nominal wage growth reached 5.5% y/y, below the rate of inflation (at 6.0%). In construction, employment fell 0.6% y/y, and wages rose 7.8% y/y.

Asia-Pacific

- Major APAC equity indices closed mixed; India +1.1%, Hong Kong +1.1%, Mainland China +0.4%, Australia -0.1%, and South Korea -1.0%.

- Meat consumption appears to be peaking in many developed countries, with beef taking the biggest hit in demand. A study from the Curtin University Sustainable Policy (CUSP) Institute in Australia investigated whether meat consumption grows as income increases and found that demand appears to peak in countries when they reach a certain level of gross domestic product (GDP). (IHS Markit Food and Agricultural Policy's Steve Gillman)

- "After analyzing data for 35 countries, we identified such a tipping point at around US$40,000 of GDP per capita," the researchers said, adding that 26 of these countries had a clear correlation between GDP growth and their level of meat consumption.

- Using data from the UN Food and Agriculture Organization (FAO) and the Organization for Economic Co-operation and Development (OECD), six countries appeared to have reached peak meat consumption for beef, poultry, pork and sheep.

- The researchers explain that countries like Canada, New Zealand and Switzerland may have reduced meat consumption because of conscious preferences for plant-based food, while the peak in three other countries (Paraguay, Nigeria and Ethiopia) peak was more involuntary and due to economic downturns, extreme weather and virus outbreaks.

- Overall, the study found that the average amount of meat a person ate each year still increased from 29.5kg in 2000 to 34kg in 2019, but many consumers in richer countries have begun to replace beef with poultry.

- Nearly all countries studied (30 of 35) experienced a steady increase in annual per capita poultry consumption between 2000 and 2019, which doubled in 13 countries and amounted to more than 20kg eaten each year in Peru, Russia and Malaysia. This was alongside 15 countries experiencing absolute decreases in per capita beef consumption between 2000 and 2019, such as a 12 kg/per capita drop in New Zealand.

- For pork, 19 countries experienced increased consumption per capita, while in seven countries consumption decreased.

- Bloomberg and several news websites in Hong Kong reported on 7 January that mainland Chinese banking regulators, which include the People's Bank of China (PBOC) and the China Banking and Insurance Regulatory Commission (CBIRC), have asked banks to increase the loan amount granted to real estate companies. Furthermore, there have been reports that banks have been asked to not include lending towards property project M&A under mainland China's three red lines policy. However, some banks have refuted this, stating that they have been asked to continue considering all lending under the three red lines. (IHS Markit Banking Risk's Angus Lam)

- Mainland Chinese regulators began to push healthy developers to purchase good-quality housing projects from cash-strapped players in the sector at the end of 2021 (see China: 21 December 2021: Mainland Chinese authorities encourage banks to lend towards property companies' M&A, potentially reducing asset quality deterioration).

- The latest news, although not confirmed by all parties, suggests that it is the first sign of loosening financing for developers by relaxing the M&A finance for healthy developers to purchase from weaker parties. This is the first relaxation since the three red lines were introduced at the start of 2021 (see China: 4 January 2021: Mainland China's central bank further caps lending for real estate to curb financial risk, limited impact on overall banking sector).

- Since the fourth quarter of 2021, banks have improved the loan amount granted to retail customers to purchase properties. According to a press release by the CBIRC on 6 January, mortgage loans had risen by 8.4% year on year in November 2021, with 90% of the loans granted to first-time buyers, suggesting the continuing of the "housing for living, not for flipping" policy.

- IHS Markit assesses that the relaxation of loans for the M&A of property projects is a short-term liquidity solution, while a restructuring of the sector, alongside poor assets, would be likely to be a more long-term outcome. However, since stability is key, it is likely that the regulator will ensure that retail customers are protected adequately by introducing a system to ensure that funds received from home purchasers are used to complete the developments.

- China's booming electric vehicle (EV) sector is set to attract more investments from automakers despite a deep subsidy cut announced by Chinese authorities that has slashed subsidies on new energy vehicles (NEVs) by up to 30% from the levels of 2021. The 2022 edition of China's NEV subsidy program, which took effect on 1 January, makes the last one of those subsidy programs launched to accelerate adoption of battery electric vehicles (BEVs) and plug-in hybrid electric vehicles (PHEVs) among Chinese consumers. China's move to slash subsidies on NEVs, however, will have a limited impact on automakers' investment plans centering on product development and production ramp-up. Although last year's NEV sales data have not been released yet, China Association of Automobile Manufacturers (CAAM) estimates that NEV sales last year in China will reach 3.4 million units, up 150% year on year (y/y). To tap into growing demand for NEVs, Chinese startups Li Auto and Xiaomi Corporation, which specialize in consumer electronics products, have secured the backing of the government of Beijing to locate their manufacturing plants in the capital city. Li Auto has committed to invest CNY6.5 billion (USD1.02 billion) in a new plant in Shunyi district (Beijing. The plant, to be completed by the end of 2023, will be dedicated to the production of Li Auto's BEVs based on its new generation EV platforms. Xiaomi, meanwhile, will invest in a manufacturing site in Beijing for the production of Xiaomi-branded EVs. The project will be constructed in two phases with 150,000-unit capacity planned for each phase. Total investment involved in the Xiaomi plant is still unknown, however given the company's pledge to begin production of its first car in the first half of 2024, construction of this new plant is likely to begin in 2022. Compared to Li Auto and Xiaomi, EV-maker NIO is making an even bolder move in capacity expansion, encouraged by surging demand for its EVs. NIO's second manufacturing site, the NeoPark, is said to be a CNY50-billion project. Construction is already under way. This new project, one of the biggest investments in the Chinese EV sector in recent years, will not only bring online a new production facility for NIO but also help Heifei, which has participated in NIO's previous financing rounds, to flesh out the city's plan to building an industry cluster for intelligent electric vehicles manufacturing. The NeoPark project, led by NIO and Anhui Jianghuai Automobile Group (JAC Group), is expected to create more than 10,000 R&D jobs related to EV and components development by 2025 and the site will house a range of companies engaged in whole car and parts manufacturing including semiconductor manufacturing, EV battery production, and electric motor design. China will continue to play a central role in advancing the auto industry's transition to electrification in the next few years. IHS Markit's latest forecast anticipates China's NEV production output to reach over 4 million units this year and further grow to 5.5 million units in 2023. (IHS Markit AutoIntelligence's Abby Chun Tu)

- Autonomous vehicle (AV) solution developer DeepRoute.ai has announced strategic co-operation with Chinese LiDAR supplier RoboSense, reports Gasgoo. The two companies plan to jointly build a cost-effective LiDAR solution to enable Level 4 autonomous capability. DeepRoute.ai offers solutions that focus on Level 4 autonomous operations and has research centers in Shenzhen and Beijing (China) and Silicon Valley (United States). The company recently unveiled its new production-ready Level 4 AV system, DeepRoute-Driver 2.0, which costs USD10,000. Last year, DeepRoute.ai opened its robotaxi pilot service to the public in Shenzhen. The company's long-term strategy involves developing medium-duty trucks for urban logistics, enhancing transit for shipments and freight delivery. (IHS Markit Automotive Mobility's Surabhi Rajpal)

- WeRide has launched a fully driverless minibus service for public on Guangzhou International Bio Island in China, according to a post on the Medium website. The WeRide robobus, which has no steering wheel, accelerator, or brake, is based on automaker Yutong Group's purpose-built electric vehicle (EV). It is powered by WeRide's full-stack software and hardware solutions for Level 4 autonomous capability and can travel at a maximum speed of 40 km/h. The WeRide robobus has launched two routes covering the popular spots on the island and operates seven days a week, from 8am to 10pm on weekdays, and from 9am to 6pm on weekends. Users can access the "WeRide Go" App mobility service platform to check real-time information about the robobuses. (IHS Markit Automotive Mobility's Surabhi Rajpal)

- BYD is expected to introduce its DM-i plug-in hybrid technology to its Han sedan. According to d1ev, the Han DM-i will have two battery options: an 18.315-kWh battery pack and a larger 37.555-kWh battery pack. The 18.315-kWh battery will only be offered in a front-wheel-drive model, which will have a range of 101 km under the Worldwide harmonized Light vehicles Test Cycles (WLTC). The 37.555-kWh version will be available with four-wheel drive and the model will boast a range of up to 206 km under the WLTC. The Han DM-i will continue to be powered by a 1.5-litre turbocharged engine that BYD developed specifically for its hybrid models. The Han, BYD's flagship sedan, has already become one of the best-selling models in China's full-size sedan market. The launch of a DM-i-powered variant to the Han line-up is expected to further boost Han's sales, which had already exceeded 117,000 units in 2021. (IHS Markit AutoIntelligence's Abby Chun Tu)

- The consortium led by South Korean electric bus manufacturer Edison Motors today (10 January) filed for court approval to take over a controlling stake in bankrupt SsangYong Motor and the court approved the move, reports the Yonhap News Agency. After the court's decision, the consortium signed a final deal with SsangYong to take over the sport utility vehicle (SUV)-focused automaker. Under the final agreement, Edison has agreed to acquire SsangYong for KRW304.8 billion (USD254.4 million), and the acquisition money will all be spent to repay some of the automaker's debt with financial institutions. It has also agreed to lend KRW50 billion in operating capital to SsangYong to help it stay afloat amid the extended COVID-19 virus pandemic and low demand for its models, highlights the report. Edison is required to submit its rehabilitation plans for SsangYong to the court by 1 March. It will establish a special-purpose company to raise KRW800 billion to KRW1 trillion this year to invest in a stake in SsangYong through the issuance of new shares in order to achieve a turnaround in three to five years. Edison plans to transform SsangYong into an electric vehicle (EV)-focused automaker over the next decade in line with changes in the automotive market. It aims to produce 10 new EVs by the end of 2022, including the Smart S, 20 EVs by 2025, and 30 EVs by 2030. Meanwhile, SsangYong will remain under court receivership until the court approves Edison's rehabilitation plans and SsangYong's creditors accept the automaker's initial debt settlement plans. (IHS Markit AutoIntelligence's Jamal Amir)

- VinFast has announced that 25,000 reservations for its new VF 7 and VF 9 were placed within 48 hours of opening, as well as a 100-unit US corporate order. Separately, VinFast also confirmed it will work with HERE Navigation and HERE SDK for navigation and a VinFast mobile application. The VF 8 and VF 9 reservations - 15,237 for the less expensive VF 8 and 9,071 for the larger VF 9 - were placed from global markets. The company did not provide a breakdown for how many reservations were in which country. (IHS Markit AutoIntelligence's Stephanie Brinley)

- In addition, and separate from the reservations, VinFast announced a corporate order in the US. A company called Artemis DNA has ordered 100 VinFast vehicles; including units of all five of the company's newly announced products, although production timing for three of them is not confirmed. Artemis DNA is a clinical diagnostics laboratory company in the US that aims to have a fully electric vehicle fleet. It expects to take delivery of its first units in the fourth quarter of 2020 and will be VinFast's first corporate customer in the US. Working with HERE Navigation will enable VinFast to leverage a navigation-as-a-service model and enable it to update and upgrade navigation offerings with new features and services throughout the vehicle's lifecycle, which VinFast says lowers costs and improves scalability. VinFast will integrate the HERE SDK (software developer kit) into the VinFast mobile application as well.

- Having previously announced plans to work with Cerence, in January 2022, VinFast announced that it will use Cerence Connected Vehicle Digital Twin (CCVDT) platform for cloud connected in-vehicle technology. Cerence will provide cloud and AI capabilities. With Cerence, VinFast says it will offer extended digital cockpit capabilities and deeper information about the car; possibilities include enabling in-car delivery services; providing electric vehicle (EV) charging network information; reminders to close doors and windows; calendar reminders; driving suggestions; and others.

- South Korea's Lotte Chemical has resurrected plans to construct a $3.95 billion petrochemical project in Indonesia's Banten Province, the company announced last Friday. Lotte Chemical signed a memorandum of understanding (MOU) with the Indonesian government, intending to complete this "Lotte Chemical Indonesia New Ethylene" (LINE) petrochemical project by 2025, Lotte Chemical said in a press release. (IHS Markit Chemical Market Advisory Service's Chuan Ong)

- The Indonesian government is in turn expected to provide incentives such as lower raw material import tariffs, exemptions on construction equipment and facilities, and tax benefits for successful implementation and commercial production.

- This project has was first mooted more than ten years ago. Lotte Group had proposed a plan to invest in a Merak petrochemical project in 2011 after its Chairman met former Indonesia's former President, Susilo Bambang Yudhoyono. It planned to spend $5 billion on a new plant to augment existing facilities in Merak, which were producing 450,000 mt/yr of linear low density polyester (LLDPE) or high density polyethylene (HDPE), and 38,000 mt/yr of biaxially oriented polypropylene (BOPP).

- According to South Korean broadsheet The Korea Economic Daily, Lotte had targeted commercial production by 2016 but suspended plans as talks with the government dragged and Lotte group was caught up by infighting between its Chairman and his sibling. The Chairman was subsequently arrested for a separate bribery case in 2018. A project ground-breaking in December 2018 slated commercial production in 2023, before the project stalled again due to the COVID-19 outbreak.

S&P Global provides industry-leading data, software and technology platforms and managed services to tackle some of the most difficult challenges in financial markets. We help our customers better understand complicated markets, reduce risk, operate more efficiently and comply with financial regulation.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.