ECONOMICS COMMENTARY — 14 Jul, 2026

Romanian goods producing sector outperforms wider CEE as signs of stabilisation emerge

Despite a range of internal and external challenges, the Romanian manufacturing sector showed signs of stabilisation in June as the BCR Manufacturing PMI survey, compiled by S&P Global, reached its third anniversary.

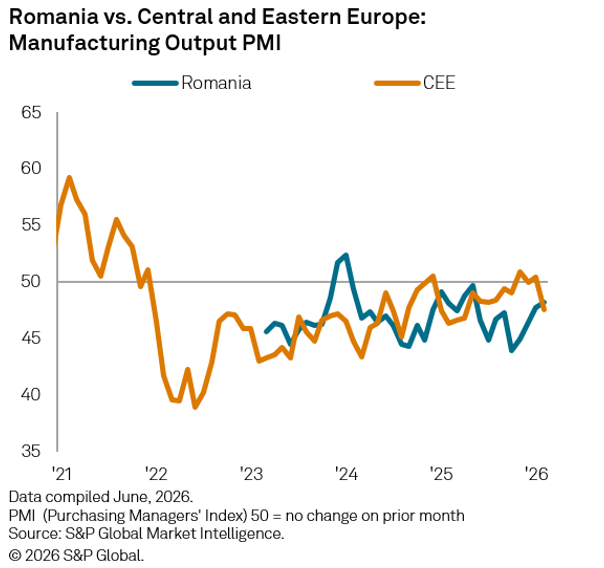

Across the past three years we have seen a contraction in manufacturing output in all but two months, though more recently the decline has sustained a trend of softening. In fact, for the first time since September of last year, the Romanian manufacturing sector outperformed the wider Central and Eastern Europe (CEE) region. The outlook remains uncertain, however, and heavily dependent on the political landscape, both globally and domestically.

Romanian manufacturing downturn moderated despite Middle East conflict

Up from 47.8 in May, the seasonally adjusted BCR Romania Manufacturing PMI Output Index posted 48.2 in June, to signal a sustained decline in production. Panellists widely attributed the latest fall to high energy costs caused by the conflict in the Middle East. Having indicated a slowing rate of contraction, however, the sector again moved closer toward stabilisation. A fourth consecutive monthly increase pushed the reading to its highest in nine months – a notable improvement on February’s survey-low.

Across the wider Central and Eastern Europe (CEE) region, June data marked a renewed contraction in manufacturing output, owing to a sharp fall in Poland. At 47.6 in June, the GDP-weighted CEE PMI Manufacturing Output Index dropped below the crucial 50.0 mark, signalling its first decline in four months (May: 50.4). The fall in the index can be attributed to a sharp reduction in Poland, while a softer decline in Romania and stronger growth in Czechia cushioned the fall. Notably, June marked the first time in nine months in which Romania has outperformed the wider CEE region.

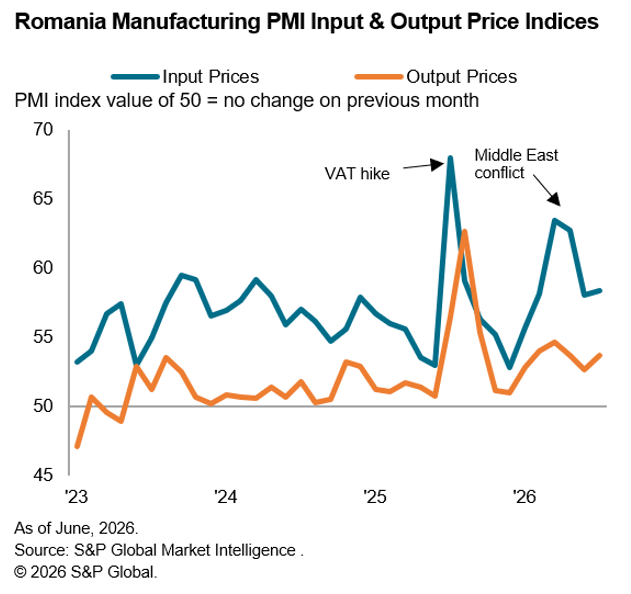

Energy price spike keeps cost pressures elevated, but less marked than last August’s VAT hike

The cost environment facing manufacturers in Romania has been turbulent over the past year. Last August saw the first increase in the standard rate of VAT since July 2010 amid the fall-out of the 2008 Global Financial Crisis. The recent increase saw the standard rate rise from 19% to 21%. In addition, the reduced rate for excluded products and services rose to 11% (up from 5% or 9%).

As expected, the impact of last August’s tax reform was most evident upon implementation, suggesting it was passed through quickly to consumers, though the rate of inflation eventually faded to a survey-low at the end of 2025. The gap between the two PMI price indices was the greatest on record last August, with input cost pressures far exceeding selling price inflation. Although manufacturers absorbed most of the higher cost burdens in the month of the VAT increase, this trend was reversed in September as firms hiked selling prices in response. In fact, this was the only month on record in which output charge inflation has been stronger than that of costs.

More recently, the outbreak of war in the Middle East and its impact on energy prices and supply chains has placed further upward pressure on costs faced by Romanian manufacturers. Although softer than the spike caused by the VAT hike, cost pressures have remained above trend since February, amid ongoing difficulties finding a resolution to the conflict.

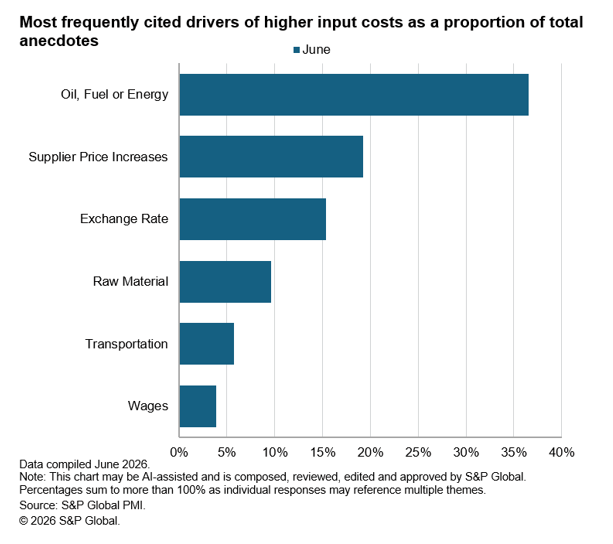

Oil, fuel and energy ranked as the leading drivers of cost inflation, cited by 37% of companies, with disruption from the closure of the Strait of Hormuz leading to higher global energy prices. Concurrently, one-in-five firms (19%) linked increased input costs to hikes in supplier price lists in June. Unfavourable exchange rate movements was also a key theme in June (15%), with a drop in the value of the leu against the euro adding to the costs of imported inputs.

Raised levels of uncertainty and subdued demand, amid frequent reports from panellists of tight customer budgets, have limited firms’ ability to pass through higher costs to customers – suggesting some margin loss at manufacturers.

Political instability weighs on currency, confidence and outlook

A loss in the early May vote of no-confidence following the withdrawal of the Social Democratic Party (PSD) from the ruling coalition saw the collapse of the Romanian minority government. The political stalemate increases the likelihood of the first snap election in Romanian history. The prospect of greater political instability adds another layer to the already challenging international climate and economic conditions. The impact of the unstable landscape was felt immediately through a depreciation of the currency. With early May seeing the leu per euro exchange rate reach an all-time high, the central bank looks set to hold policy rates through 2026 as it continues to try to limit the currency’s depreciation.

Indeed, the PMI’s forward-looking sentiment indicator showed that manufacturers in Romania were only cautiously optimistic in the outlook for the next 12 months. The PMI Future Output Index bottomed out at a survey-low in April and has only seen slight improvements in subsequent months. Hopes for a more stable business environment were frequently reported by panellists.

© 2026, S&P Global. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

Read our latest PMI commentary here.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Theme

Location

Products & Offerings