ECONOMICS COMMENTARY — 14 Jul, 2026

Global goods trade falls for second month in June as boost from inventory building fades

The worldwide Purchasing Managers’ Index™ (PMI®) surveys indicated that global goods trade flows weakened in June, marking the steepest contraction since December. The Middle East war has dampened demand as customers push back on higher prices and persistent uncertainty reduces export orders. Although these factors moderated in June, and tariff concerns eased, as anticipated a new drag is coming from reduced inventory building.

Japan and Taiwan notably bucked the global slowdown trend, benefiting respectively from a weakened currency and chip demand, but ASEAN exports deteriorated sharply to underscore how trade from these economies has so far been hardest hit by the war in the Middle East.

Global trade flows weakened by Middle East war

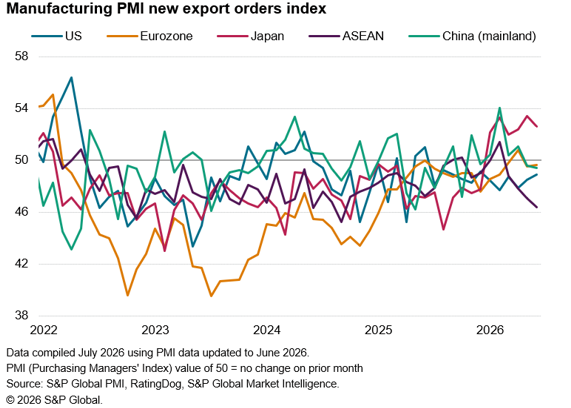

The seasonally adjusted Global Manufacturing PMI New Export Orders, sponsored by J.P.Morgan and compiled by S&P Global, registered 49.4 in June, down from 49.6 in May, running slightly below the 50.0 neutral mark to signal a second successive month of falling goods trade volumes and the steepest decline since last December. The drop in goods trade was accompanied by a further fall in services trade, albeit at a reduced rate, pointing to another month of subdued global trade.

The ongoing weakness of goods exports tracked by the PMI translates into a signal of weakened annual growth of worldwide merchandise trade volumes after growth had picked up earlier in the year. The PMI is indicative of goods trade growing at an approximate 4% annual rate, down from around 8% back in February prior to the outbreak of the war in the Middle East.

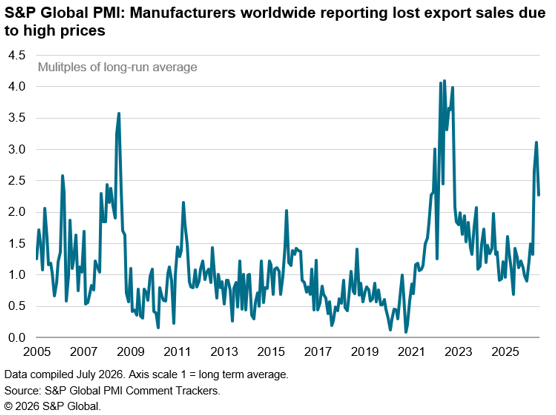

Pushback on prices

A key cause of lower trade volumes has been reduced demand caused by high prices. The number of manufacturers reporting lower export orders due to customer pushback to higher prices has risen since the outbreak of the war. Although June saw some easing of this price-resistance amid some lowering of charges levied, especially in terms of shipping and energy surcharges, customer opposing higher prices for exported goods remains more widespread than at any time since 2022.

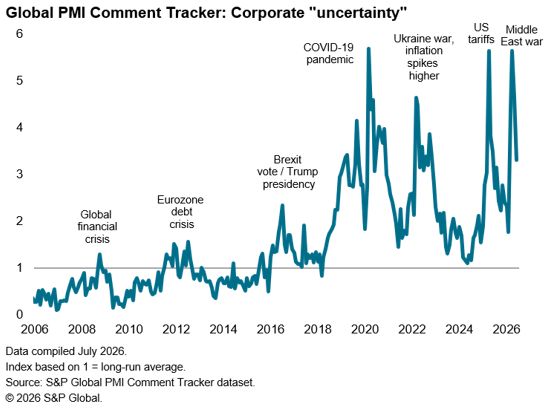

Peak uncertainty?

A further factor we can identify as dragging on global exports is the ongoing prevalence of business ‘uncertainty’, as tracked by PMI surveys in terms of the degree to which uncertainty has reportedly acted as a constraint on orders or optimism regarding future output. Reported uncertainty (covering manufacturers and service providers) peaked in April as the impact of the Middle East war exacerbated existing geopolitical worries. However, reports of uncertainty fell since, albeit remaining elevated by historical standards, due to the improved news flow out of the Middle East during the survey data collection period.

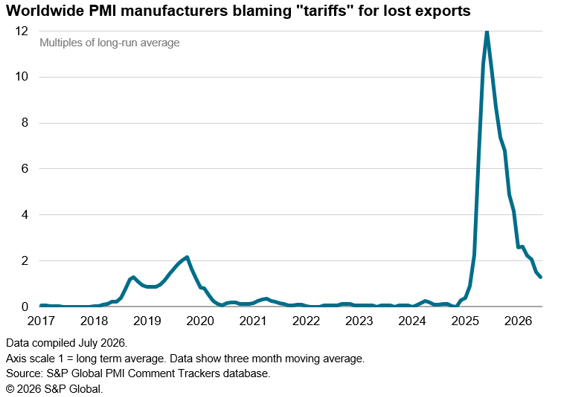

Tariff worries ease

Goods exporters also report a reduced detrimental impact from tariffs, with the incidence of exports being lost directly as a result of tariffs or related policy running close to its long run average again in June, having peaked at 12 times the long run average back in June of last year.

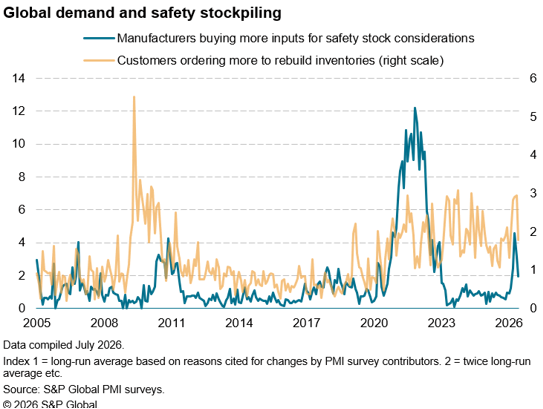

Inventory boost fades

However, while the drags from high prices, uncertainty and tariffs can be seen to have moderated in June, a fresh drag is emanating from the inventory cycle. Manufacturers continue to benefit from precautionary ‘safety stock’ building from their customers, linked in turn to concerns over supply availability and the potential for further price hikes. However, anecdotal evidence collected from PMI survey contributors indicated that this stock building boost faded markedly in May and June from a peak in April.

Japan benefits from weaker yen to buck wider trade slowdown

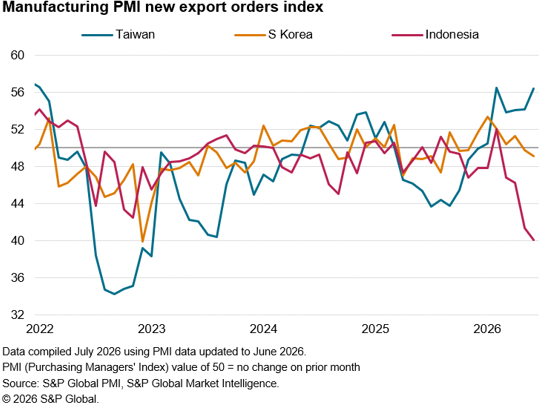

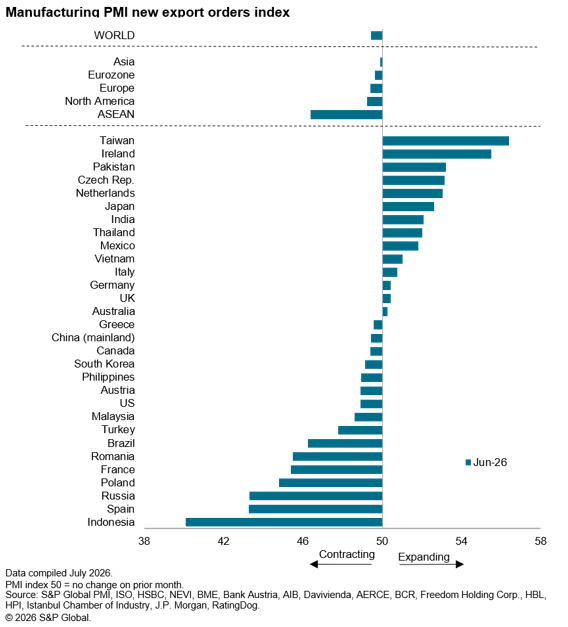

Among the major economies, goods export volumes fell in the US, mainland China and eurozone in June, as well as in South Korea, Canada, Brazil and Russia, but Japan reported a further improvement, with export orders rising so far this year to a degree not seen for five years. Japanese exporters again reported the benefit of a weakened exchange rate, with the yen hitting near four-decade lows against the US dollar. However, the strongest export growth of all economies monitored by the S&P Global PMI was seen in Taiwan, where stock building and chip demand pushed export growth to its second-highest since January 2022, followed by Ireland and Pakistan.

In contrast, the ASEAN region has seen an especially sharp deterioration in goods exports since the onset of the war in the Middle East, led by falling trade out of Indonesia, which reported the largest drop in exports of all economies in June. ASEAN exporters have been hit by lost energy supply as well as broader trade policy uncertainties, causing volumes to deteriorate at the fastest rate for 21 months in June.

© 2026, S&P Global. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

Read our latest PMI commentary here.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Theme

Location

Products & Offerings