Research — July 13, 2026

Axon’s software business to account for nearly two-thirds of revenue by 2030

By Shweta Pandey

Axon Enterprise (NASDAQ: AXON) is evolving from a hardware-focused supplier of Tasers and body cameras into a broader public safety technology platform, with software and cloud services becoming an increasingly important driver of growth.

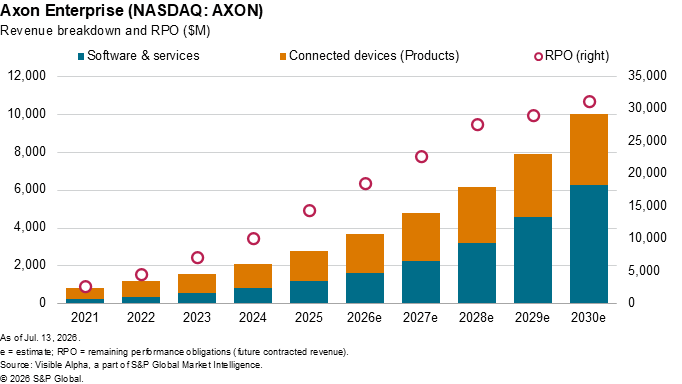

Visible Alpha consensus estimates show revenue from Axon’s Software & Services segment rising more than sixfold, from $255 million in 2021 to $1.6 billion in 2026, accounting for nearly 45% of total revenue. By 2030, the segment is expected to generate $6.3 billion in sales, representing 63% of company revenue and becoming Axon’s largest business line.

The shift reflects growing adoption of Axon’s subscription-based ecosystem, including digital evidence management, records management, computer-aided dispatch, and AI-powered tools. The company has increasingly positioned its cloud platform as a way for law enforcement agencies to manage the full public safety workflow.

Axon’s hardware business, however, remains a key contributor to growth. Revenue from its Connected Devices segment is projected to reach $2 billion in 2026, up 29% year-on-year, driven by continued demand for its core public safety products. Taser devices are expected to generate $1.1 billion in sales in 2026, while personal sensors and platform solutions are forecast at $492 million and $457 million, respectively.

The company’s expanding subscription base is also reflected in its contracted backlog. Remaining performance obligations (RPO) are expected to reach $18.5 billion in 2026, up 29% year-on-year.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Products & Offerings

Segment