Research — June 1, 2026

Walmart postQ: Revenue strength offset by margin pressure, cautious guidance

By Aarti Karwa

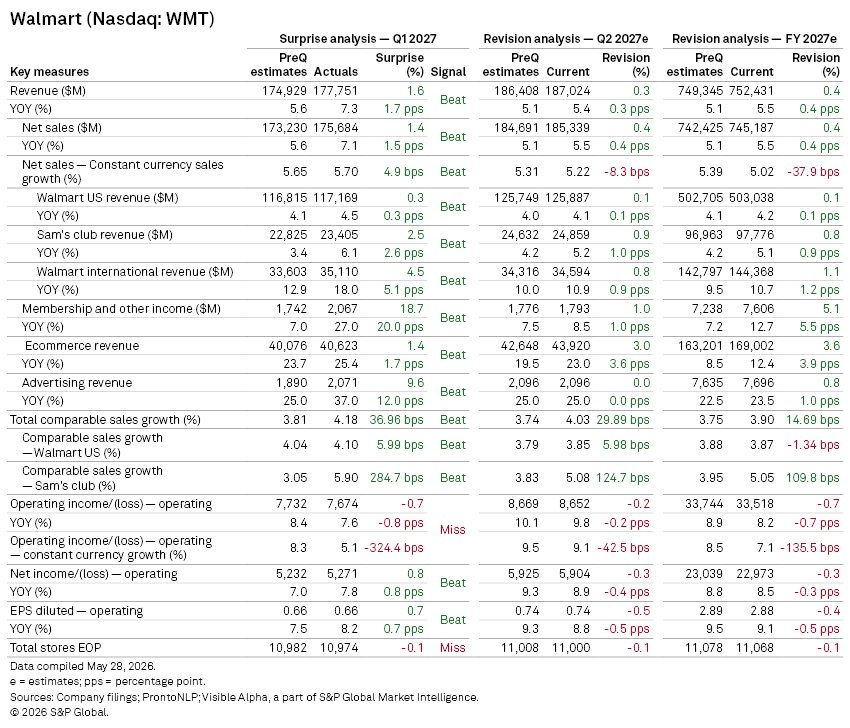

Walmart (NASDAQ: WMT) delivered a broadly solid Q1 2027 on May 21, with revenue and sales modestly coming in ahead of Visible Alpha consensus expectations, supported by sustained momentum across its US retail operations, membership model, advertising platform and international businesses. However, stronger-than-expected growth at the top line was offset by margin pressure and a more cautious profit outlook, triggering a sharp post-earnings share price decline.

Looking at earnings summaries compiled by S&P Global Pronto NLP, along with Visible Alpha pre-quarter consensus expectations and revised outlook, here are some key takeaways.

Key takeaways

Q1 revenue of $177.8 billion and net sales of $175.7 billion came in ahead of consensus expectations by 1.6% and 1.4%, respectively. Growth was broad-based across segments, with Walmart US revenue rising 4.5% year on year to $117.2 billion and comparable sales up 4.19%, reflecting steady demand and continued traffic gains.

Membership-focused Sam's Club remained standout, with revenue up 6.1% to $23.4 billion and comparable sales growth of 5.9%, materially ahead of consensus expectations, driven by strong traffic and accelerating e-commerce penetration. International operations also contributed meaningfully, with revenue up 18% to $35.1 billion, led by Asia-facing digital growth and improving execution across key markets, including continued momentum at Flipkart.

Enterprise e-commerce sales rose 26% to $40.6 billion, supported by faster delivery capabilities and stronger integration across stores and digital platforms. Higher-margin adjacencies continued to scale, with advertising revenue increasing 37% year-on-year to $2.1 billion, and membership and other income rising 27%.

However, profitability trends were less supportive. Non-GAAP operating income rose 7.6% year-on-year to $7.7 billion but slightly missed expectations, driven in part by around $175 million of higher fuel costs. Constant-currency operating income growth of 5.1% came in below consensus expectations by 325bps. Adjusted EPS of $0.66 was broadly in line, while non-GAAP net income rose 8% to $5.27 billion, slightly ahead of expectations.

Store count remained stable at 10,974 locations.

Guidance

Management guided Q2 constant-currency net sales growth of 4%–5%, below preQ expectations of 5.3%, while operating income growth of 7%–10% broadly aligned with consensus.

Full-year guidance also disappointed, with constant-currency net sales growth guidance of 3.5%–4.5% and operating income growth of 6%–8% both trailing pre-quarter expectations.

EPS guidance of $2.75–$2.85 also came in below consensus expectations, reinforcing concerns around margin pressure and cost headwinds despite healthy demand trends.

Management commentary

Management highlighted continued strength in traffic across Walmart U.S. and Sam’s Club, supported by value-oriented consumer behaviour and convenience-led shopping patterns. However, it reiterated that guidance assumes no tariff relief and continues to reflect uncertainty around tariffs and fuel costs.

Strategically, the company pointed to sustained momentum in higher-margin businesses, including advertising, marketplace and membership, where faster delivery capabilities are improving seller participation and customer engagement. Private label expansion, particularly “Better Goods” and Member’s Mark, continues to support both margin resilience and trade-down dynamics among higher-income households.

Pharmacy normalization remained a headwind during the quarter, contributing roughly a 100bps drag on Walmart US comparable sales growth.

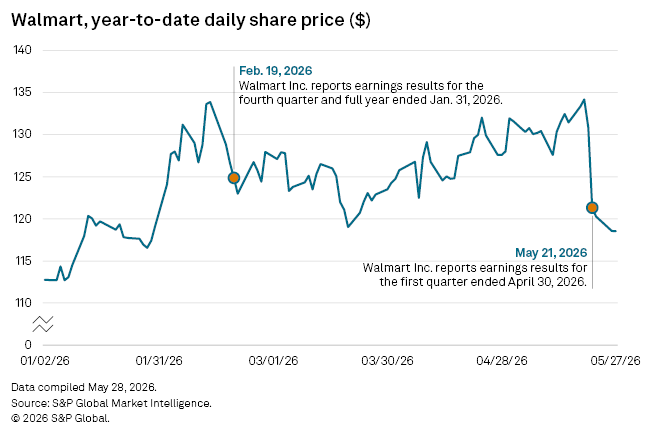

Share price reaction

Despite the revenue beat, Walmart’s shares fell sharply after results, as investors reacted to weaker-than-expected forward profit guidance and concerns that elevated fuel and distribution costs could continue to constrain margin expansion.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Products & Offerings

Segment