Research — June 3, 2026

Pan American Silver leans on prices and Juanicipio ramp-up to drive 2026 growth

By Monika Panchal and Sonam Sidana

Pan American Silver Corp. (TSX: PAAS) has delivered a volatile near-term share price performance, slipping 0.9% over the past week even as momentum remains firmly positive over longer horizons, with gains of 7.1% over the past month, 8.8% year-to-date and more than doubling over the past year. In Q1 2026, the Canadian miner reported revenues of $1.2 billion, marking a near 50% year-on-year increase, while silver segment all-in sustaining costs fell sharply to $6.63 per ounce, positioning the company among the lower-cost producers and enhancing its leverage to elevated metal prices.

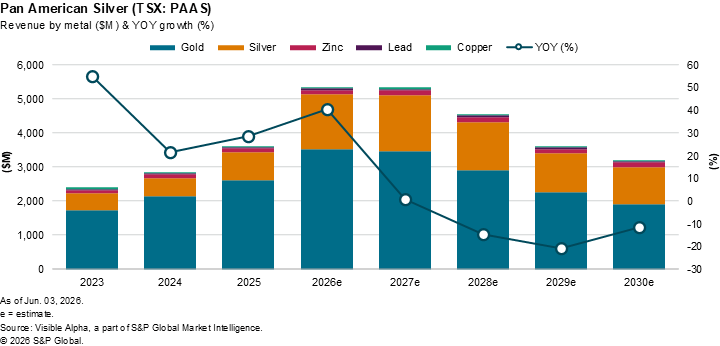

Based on Visible Alpha consensus estimates, Pan American is poised for strong growth through 2026. Revenues are expected to rise 41% year-on-year to $5.1 billion, driven primarily by a 96% surge in silver revenues to $1.6 billion and a 36% increase in gold to $3.5 billion. Copper, while a smaller contributor, is also projected to expand 27% to $27 million. By contrast, revenues from other metals such as zinc and lead are expected to decline modestly.

The outlook is driven by a favorable pricing environment. Gold and silver prices have remained elevated over the past year, providing a strong tailwind for producers with scale exposure to both metals. Operationally, Pan American is also benefiting from an expanded asset base following its acquisition of MAG Silver in September 2025. The deal significantly strengthened its silver reserves and added a 44% stake in the Juanicipio project, a high-grade, large-scale operation that is rapidly ramping up.

Revenue from the Juanicipio mine is expected to climb to $543 million in 2026, up from $81 million a year earlier, highlighting the asset’s growing contribution.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Products & Offerings

Segment