ECONOMICS COMMENTARY — 23 Jun, 2026

Japan flash PMI shows brighter growth picture in June but price pressures run close to survey highs

The S&P Global Flash PMI® data showed output growth staging a welcome improvement in Japan during June, rounding off a solid second quarter to point to encouraging resilience of the economy in the face of headwinds created by the war in the Middle East. However, inflationary pressures remained elevated, with input costs rising at one of the sharpest rates yet recorded by the survey.

High prices, concerns over supply availability and sluggish economic growth have meanwhile ensured that business confidence about growth in the year ahead remain subdued, though confidence has at least lifted off the recent low seen in May amid brightening news out of the Middle East.

Faster growth in June rounds off solid second quarter

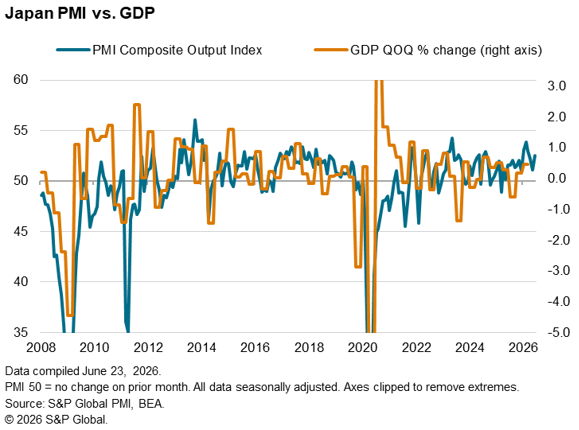

Business activity growth picked up in June. The headline S&P Global Japan PMI Composite Output Index rose from a five-month low of 51.1 in May to 52.5 according to the ‘flash’ reading. While failing to match the impressive high seen back in February, prior to the outbreak of the war in the Middle East, the June reading rounds off a solid second quarter, indicative of the economy growing at an approximate 0.5% quarterly pace.

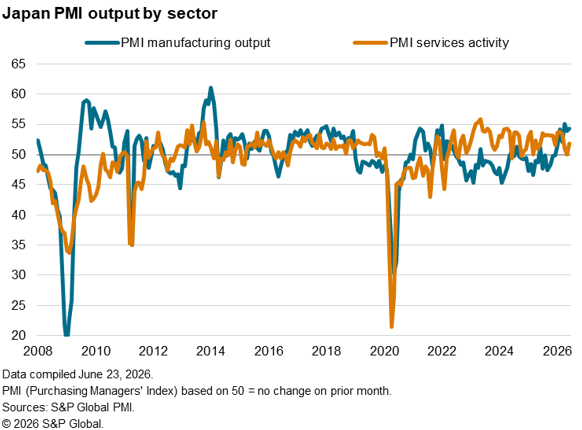

Manufacturing continued to grow at an especially encouraging pace, having in recent months enjoyed one of its best growth spurts seen over the past decade. Inflows of new orders into manufacturing rose in June at the fastest pace for nearly four-and-a-half years. However, the expansion was again boosted by customers ordering additional purchases ahead of war-related price and supply worries, with manufacturers also encouraged to boost production while input cost and availability were favourable.

This stock building therefore poses a downside risk to manufacturing growth in the coming months once the inventory cycle moves into reverse.

It was therefore encouraging to see the service sector report renewed growth after its expansion had stalled in May. However, the rate of growth remained subdued, ending a second quarter which has seen the service sector expand at a much-reduced rate compared to that seen in the opening quarter of the year.

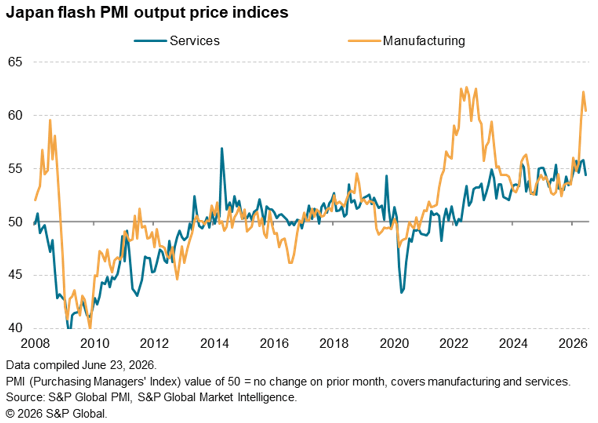

Elevated price pressures

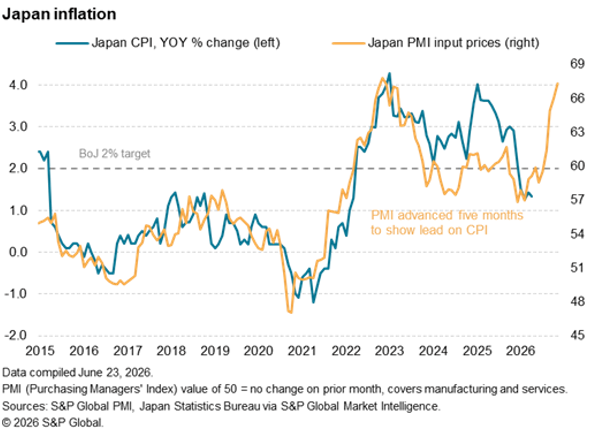

While the June flash PMI brought better news on economic growth in Japan, the news on inflation remained concerning. Firms’ input costs – measured across both goods and services – rose at the joint-fastest rate since data were first available in 2007, only exceeded by that seen in June 2022. The surge in input cost inflation seen since the start of the war points to consumer price inflation rising markedly in the coming months as these higher costs are passed down supply chains.

There are signs that margins are being squeezed as companies seek to soak up some of the cost increases to remain competitive, with selling price inflation cooling slightly in June across both goods and services. However, the overall rate of increase remained one of the highest recorded over the survey history.

War developments to shape outlook

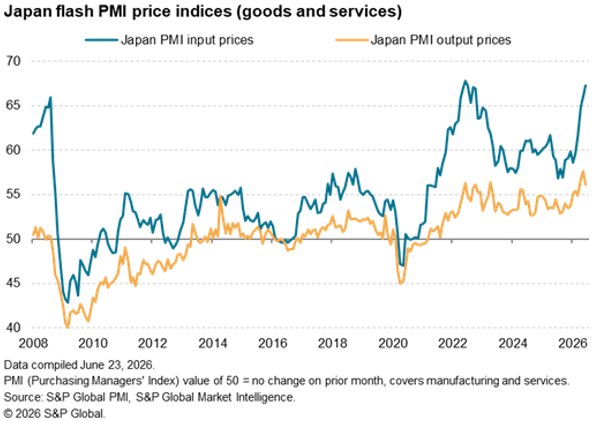

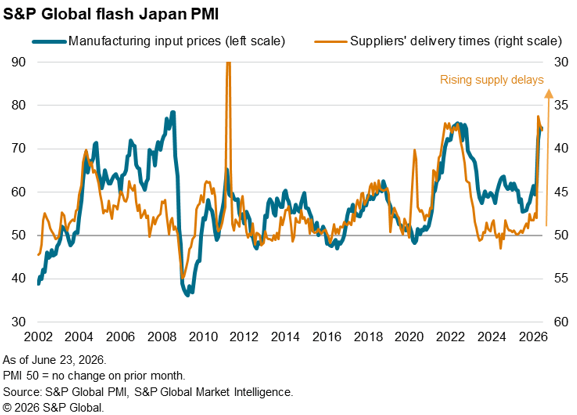

Many of the recent cost pressures reflect higher energy prices resulting from the war in the Middle East, which have cooled notably in recent days. Similarly, goods prices have spiked higher amid supply chain disruptions (and an associated jump in demand for safety stocks) emanating from the closure of the Strait of Hormuz. The lengthening of supplier lead times over the past three months has been among the steepest seen in the history of the PMI in Japan, though the incidence of delays in June was the least pronounced since March. The extent to which these factors ease in the coming weeks will play an important role in determining the outlook for inflation, and whether the recent spike in prices tuns into something more long lasting.

Companies’ expectations of output growth in the year ahead meanwhile remained among the lowest recorded since the pandemic, largely reflecting concerns over the combination of inflation, supply shortages and slower economic growth both at home and abroad. However, signs of better news out of the Middle East and lower oil prices played a role in helping lift future sentiment of the recent low in May (the lowest since 2020).

Access the press release here.

© 2026, S&P Global. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

Read our latest PMI commentary here.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Theme

Location

Products & Offerings