ECONOMICS COMMENTARY — 05 Jun, 2026

Intense commodity price and supply pressures threaten global manufacturing performance

The latest manufacturing PMI survey data point to the war in the Middle East having induced a surge in demand for manufactured goods and inputs.

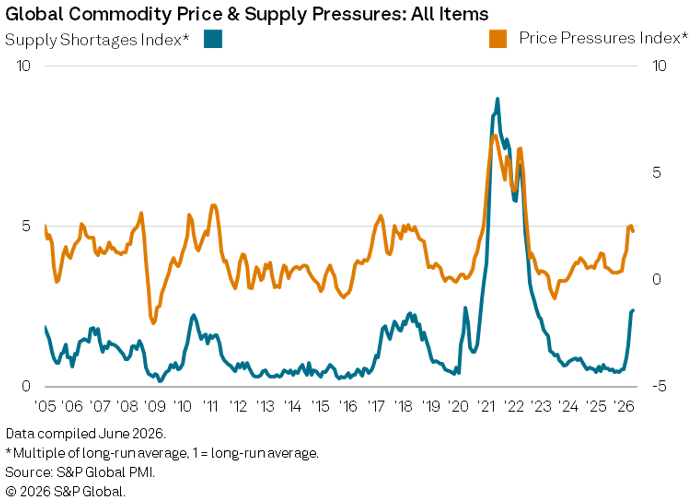

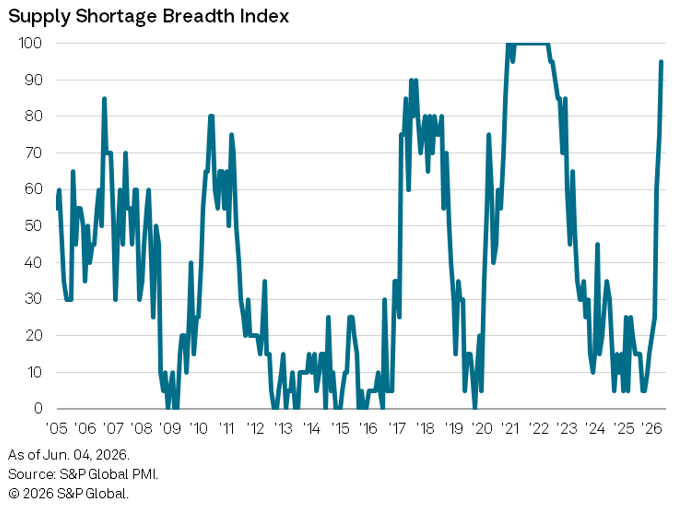

That said, a marked intensification of commodity price and supply pressures since the start of the conflict has pushed manufacturing costs higher and placed considerable strain on supply chains. The S&P Global PMI Commodity Price & Supply Indicators pointed to a potential peaking of price pressures in April, having eased slightly in May, but price inflation remains historically elevated. Reported supply shortages, however, have crept higher in each month since February to now stand at the highest for three-and-a-half years.

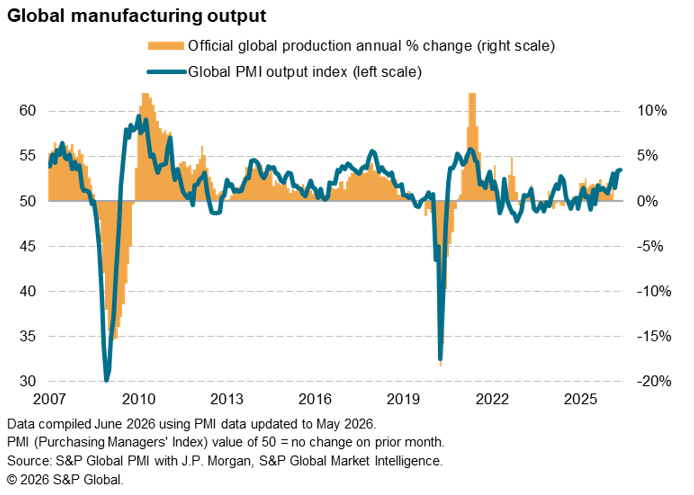

Output growth strengthens despite supply chain pressures

The Global Manufacturing Purchasing Managers’ Index (PMI) survey, sponsored by J.P. Morgan and compiled by S&P Global Market Intelligence, recorded the sharpest rise in worldwide factory production since July 2021 in May. The latest upturn built on a similarly strong increase in April.

The associated Global PMITM Commodity Price and Supply Indicators meanwhile signalled another intensification of supply pressures across the global manufacturing sector midway through the second quarter. The PMI Global Supply Shortages Index reached the highest reading since November 2022, and indicated that reported supplier shortfalls were running at nearly two-and-a-half times the normal level. At the same time, the corresponding PMI Price Pressures Index dipped from the near four-year highs seen in March and April, but still indicated that reports of higher commodity prices were nearly two-and-a-half times above the usual level.

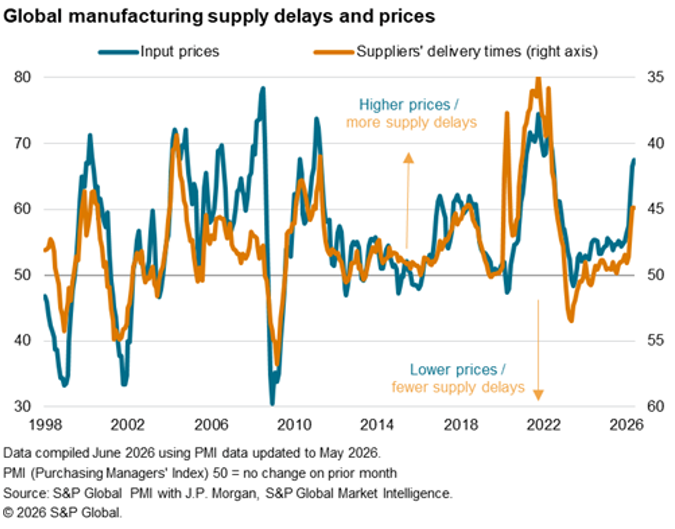

The surge in demand for inventory has exacerbated supply and shipping delays caused by the effective closure of the Strait of Hormuz. As a result, average supplier delivery times have lengthened in April and May to the greatest extents since mid-2022.

With demand exceeding supply for many products, prices have risen sharply again in May. Higher energy and shipping prices have also fed through to increased costs. Factory input prices consequently rose globally at the steepest rate since June 2022 during May, the rate of inflation having accelerated now for four successive months.

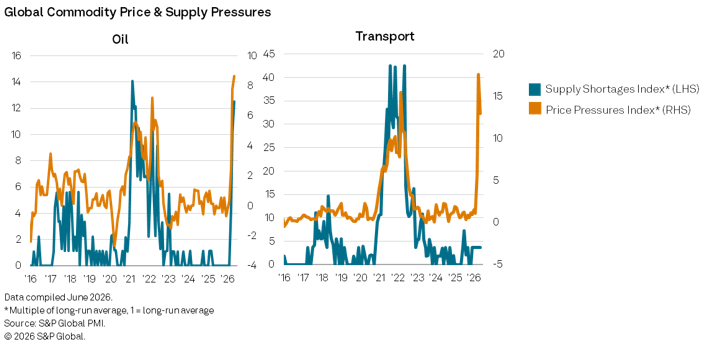

Oil disruptions impact shipping and freight capabilities

May data signalled that all but one of the 20 monitored key commodities registered above-average shortages in May, led unsurprisingly by Oil. The effective closure of the Strait of Hormuz has severely disrupted supply chains and the delivery of a range of commodities, with the impact felt most keenly in oil markets. This in turn has filtered into vendors’ supply capabilities, as Transport also saw a marked number of reported supply availability shortfalls.

On the price front, only one of the 26 monitored key commodities signalled below-average reports of price increases during May. Transport recorded the most intense cost pressures, closely followed by Semiconductors and Oil, with the latter seeing the greatest number of reports of price rises since data collection began in 2005.

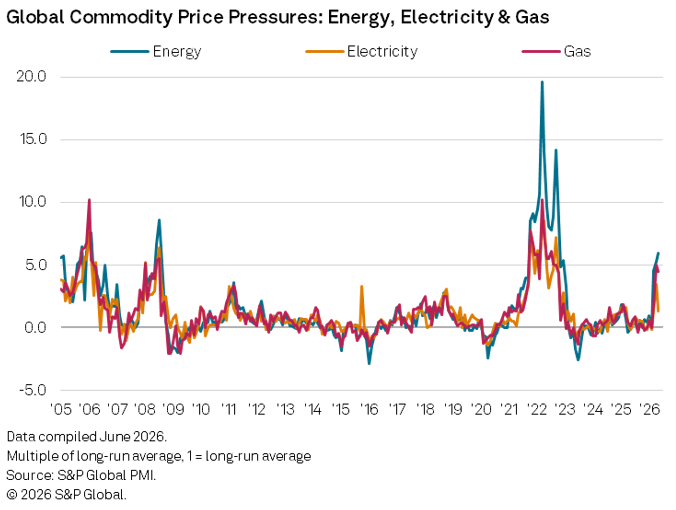

Elsewhere, price pressures reverberated through the wider energy market, tying up with mentions by manufacturers in the Global Manufacturing PMI. In fact, reported price pressures in May were at their highest for nearly four years, after easing only slightly since April. Within this, electricity and gas prices rose to their highest since the Russia-Ukraine war in April, though this has since eased in May.

Other key raw materials see pressures intensify since outbreak of war

The only exception to above-average reports of supply shortfalls in May was Timber.

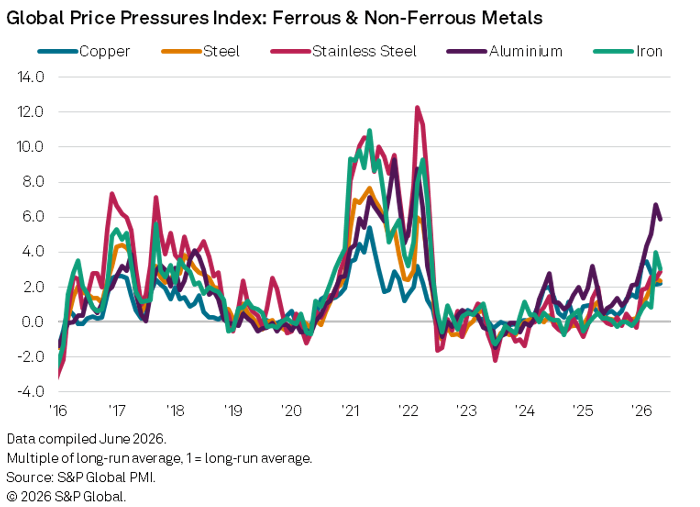

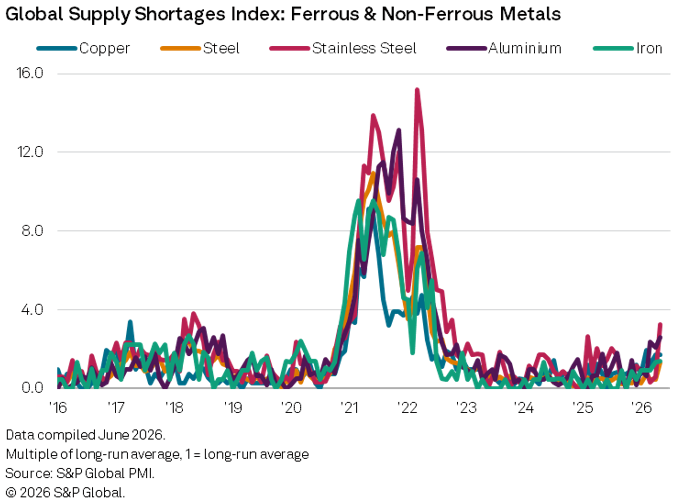

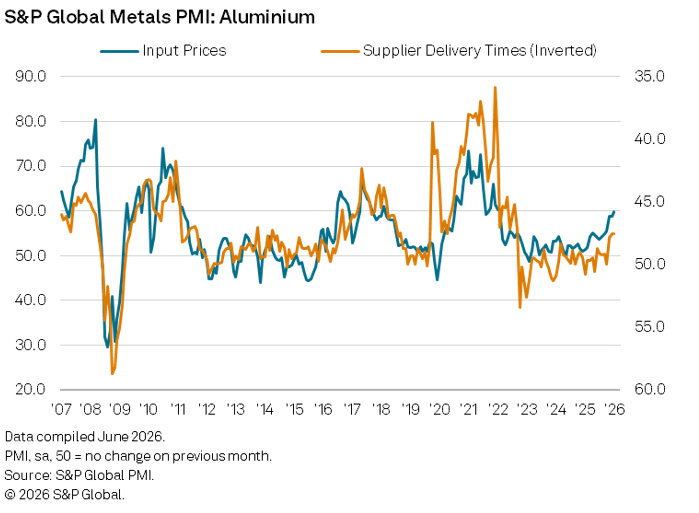

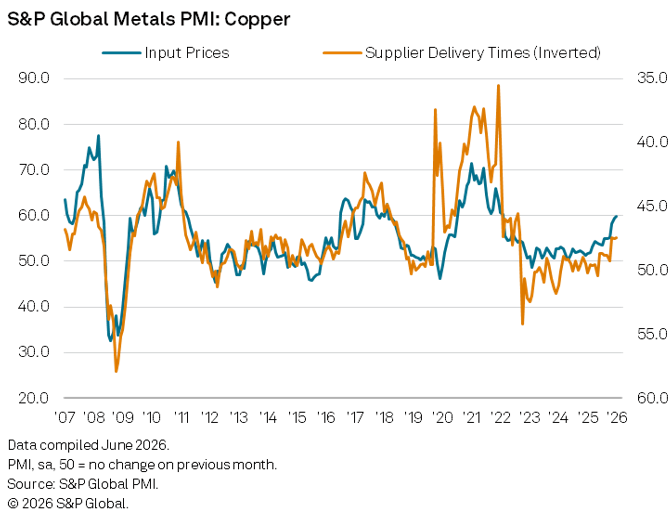

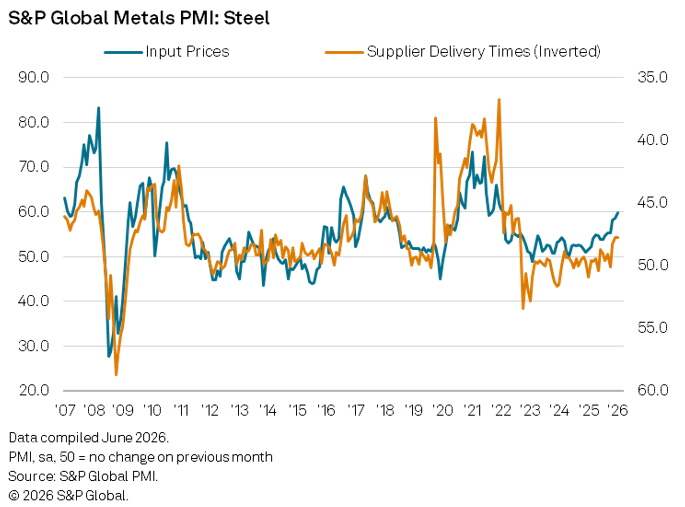

Global metal markets were among those which also saw disruptions during April and May. Both ferrous and non-ferrous metals registered higher-than-average reports of both rising prices and supply shortfalls. The steepest price increases were reportedly seen for Aluminium, which were around the highest since the surge in prices seen during the pandemic recovery period and outbreak of the Russia-Ukraine war amid the most marked number of reports of shortages in nearly four years. That said, Stainless Steel looks to be the metal facing the strongest supply pressures, leading the five metals monitored, with the respective index posting its highest reading since October 2022.

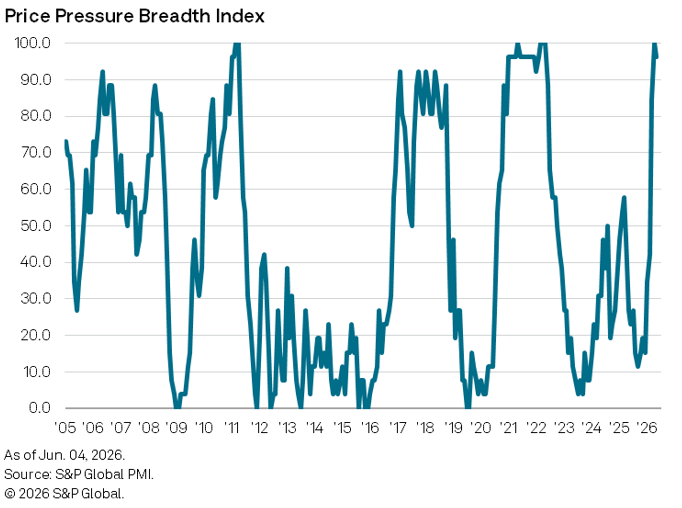

Moreover, data detailing the breadth of the impact on commodity markets shows that this is not just a purely oil-based shock. May data found that 95% of commodities monitored by the survey displayed above-average reports of supply shortages, while the corresponding figure for price pressures was 96.2%.

PMI data covering aluminium, copper and steel markets meanwhile signalled a sharp deterioration in vendor performance, coinciding with elevated reports of supply shortages during May. Moreover, anecdotal evidence collected from firms identified as heavy users of aluminium, copper and steel pointed to the impact of the war across the metals market, mentioning that output growth was bolstered by efforts to build inventories to protect against ongoing disruption to supply chains. That said, the expansion in new orders in May due to some companies highlighting that the intensification of price and supply disruption had stunted demand growth.

In fact, the rise in the number of reports of supplier shortfalls for these monitored metals directly coincided with global metal users registering solid deteriorations in vendor performance. As a result, the rate of input cost inflation accelerated again across all three markets, with all three metals recording similarly marked increases.

Outlook

It is clear that events in the Middle East will be key to determining the trajectory of commodities in the near-term. Uncertainty regarding the timing of any agreement to end the conflict and resume shipping through the Strait of Hormuz is a key headwind to the alleviation of price and supply pressures in the coming months. Moreover, while the PMI Price & Supply Indicators point to a potential turning point for prices, reported shortfalls continue to edge higher, potentially placing additional strain on commodity prices and global manufacturing companies if buffer stocks deplete.

© 2026, S&P Global. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

Read our latest PMI commentary here.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Theme

Location

Products & Offerings