ECONOMICS COMMENTARY — 23 Jun, 2026

Flash PMIs signal diverging growth trends among the major developed economies

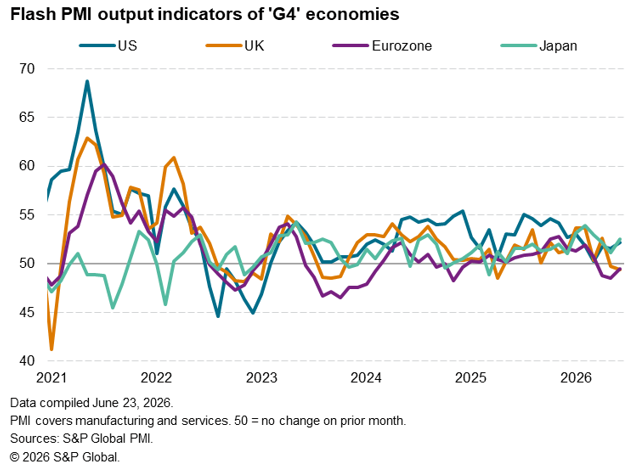

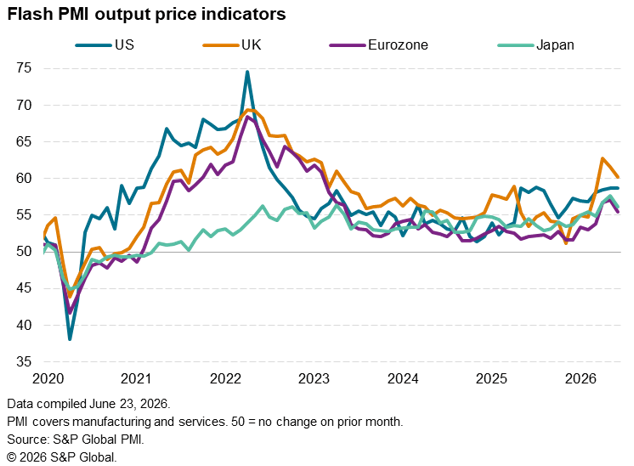

S&P Global’s flash PMI surveys showed business growth accelerating in both the United States and Japan in June while further declines were recorded in both the eurozone and UK. These output indicators are likely to map out the route for central bank policy in the coming months, being key gauges of the extent to which the recent energy-driven spikes in inflation could persist via second-round inflation effects.

US and Japan pick up pace as Europe contracts

Business activity growth across the four largest advanced economies – the US, eurozone, Japan and the UK (the ‘G4’) – grew in June at the fastest rate since the outbreak of the war in the Middle East, according to flash PMI data, though trends varied markedly among the four economies.

While growth accelerated in the US and Japan, hitting five- and three-month highs respectively, both the UK and eurozone reported falling output, albeit registering only modest declines.

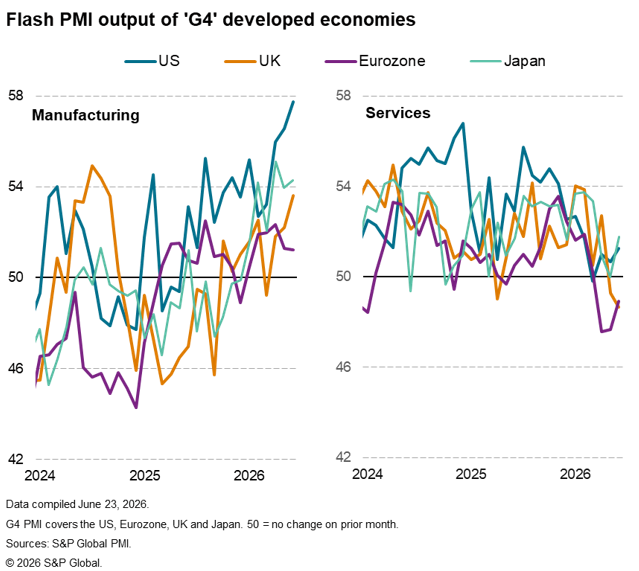

The standout performer was the US manufacturing economy, where output growth accelerated to its fastest since July 2021. However, goods production growth also remained solid in Japan and the UK. Japan notched up its second-best performance in four-and-a-half years, while UK goods producers also reported a marked acceleration of growth. More modest, but still positive, manufacturing growth was seen in the eurozone,

A divergence in services growth was meanwhile characterised by falling activity in Europe contrasting with modest upturns in the US and Japan. However, in all cases, service growth has taken a hit from the outbreak of the war, with growth stymied across the board by high prices in particular. In manufacturing, some insulation against the demand-sapping impact of higher prices has been evident thanks to further precautionary stock piling, with buyers often keen to secure supplies despite increased costs.

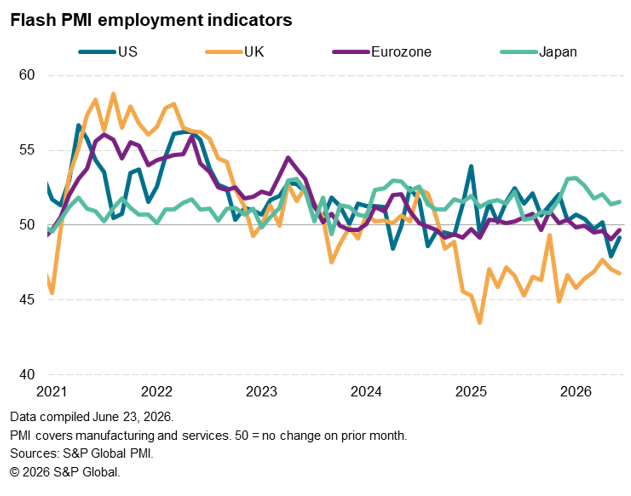

Headcounts under pressure from rising costs

Of the four economies, only Japan continued to report jobs growth in June, with employment again falling especially sharply in the UK and declines seen in the US and eurozone. Job losses were commonly blamed on high operating costs, in turn widely linked to recent increases in energy and raw material prices, though in the UK, existing government policies have added more permanently to companies’ costs. The US notably reported one of the steepest factory job falls witnessed in the two-decade history of the S&P Global PMI.

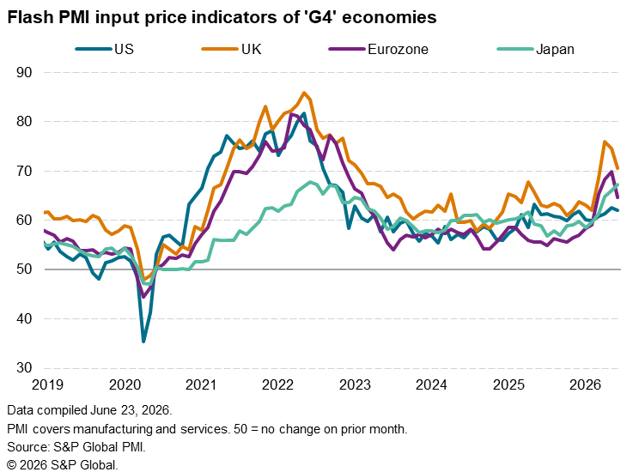

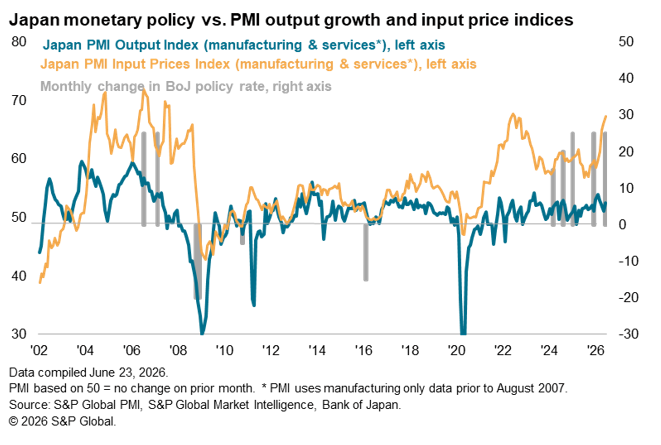

Record cost growth in Japan

There was also mixed news on price trends. Whereas rates of input cost inflation eased in Europe and to a lesser extent the US, thanks in part to lower energy prices toward the end of the June PMI flash data collection period, the rate of cost inflation accelerated in Japan to the highest for four years as the impact of high energy costs was exacerbated by the weaker yen. The rise in Japanese producer prices was in fact the joint-fastest since data were first available in 2007, only exceeded by that seen in June 2022.

There was also a divergence in selling price trends. Whereas rates of selling price inflation across goods and services moderated in the eurozone, UK and Japan, it held steady at May’s elevated rate in the US, hinting at potentially stickier price pressures. However, some US pricing power was linked to the FIFA World Cup.

Policy divergence

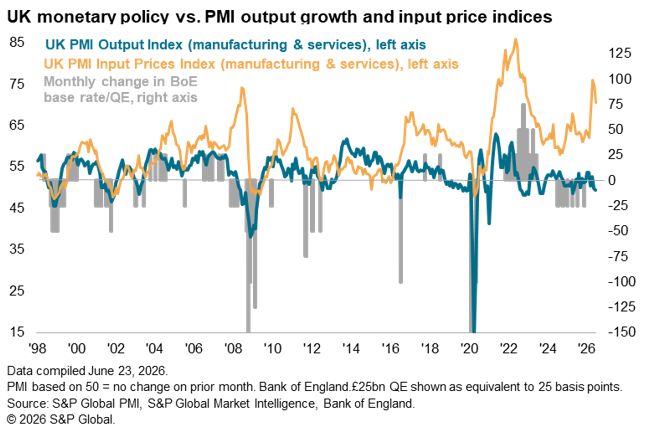

The survey data therefore indicate how, among the major developed economies, Europe has so far been hardest hit by the outbreak of war in terms of lost output, with the UK also notably suffering a particularly steep cost burden increase as war-related cost growth exacerbated existing business expenses increases stemming from government policy on employment law.

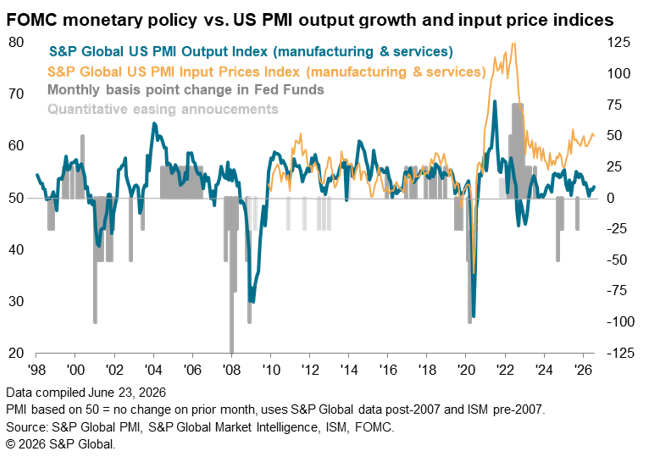

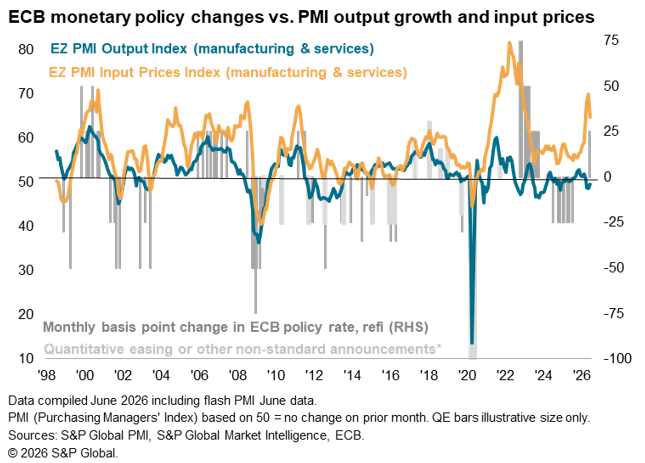

From a policy perspective, the sustained robust output growth in the US hints at interest rates running higher than in both the eurozone and UK. Although near-term price increases have added to hawkish pressures in Europe, with the ECB even hiking rates in June, the weakness of output and employment growth in Europe point to diminished risks of second round inflationary effects compared to the more robust growth picture still being seen in the US.

However, with jobs also coming under pressure again in the US during June, and temporary factors of the FIFA World Cup and stock building boosting US services and manufacturing respectively in June, the resilience of the US economy will likely be tested in the coming months.

The Bank of Japan has meanwhile also hiked, taking its policy rate to a 31-year high, albeit of just 1.0%. Whether further rate hikes can be justified will depend not just on the inflation trajectory but also on the resilience of output growth.

© 2026, S&P Global. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

Read our latest PMI commentary here.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Theme

Location

Products & Offerings