ECONOMICS COMMENTARY — 23 Jun, 2026

Eurozone flash PMI points to flatlining economy in June but price pressures cool

The eurozone economy is showing enough resilience to just about stay out of recession, according to fresh survey data from S&P Global. The flash PMI registered only a slight drop in business activity in June, meaning the survey is indicative of unchanged GDP over the second quarter.

There is welcome news of an easing in the recent downturn in services activity, with tourism and leisure related industries seeing signs of recovering demand after the initial disruptions from the war in the Middle East.

Manufacturing meanwhile continues to benefit from inventory building as customers front-run future prices rises or supply issues amid ongoing supply fears linked to the war. However, although widespread supply chain delays contributed to further upward pressure on prices, there are signs that concerns over supply and price trends are starting to moderate.

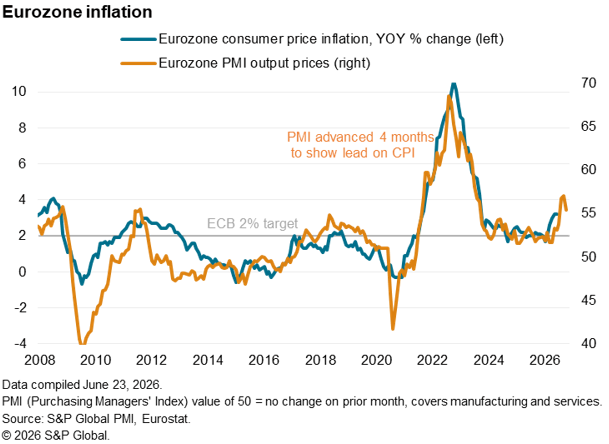

Encouragingly, lower energy prices are already filtering through to businesses and rates of input cost and selling price inflation have moved lower in June to hint at a potential peaking of the price spike.

The June survey was conducted largely before the announcement of the MOU between the US and Iran.

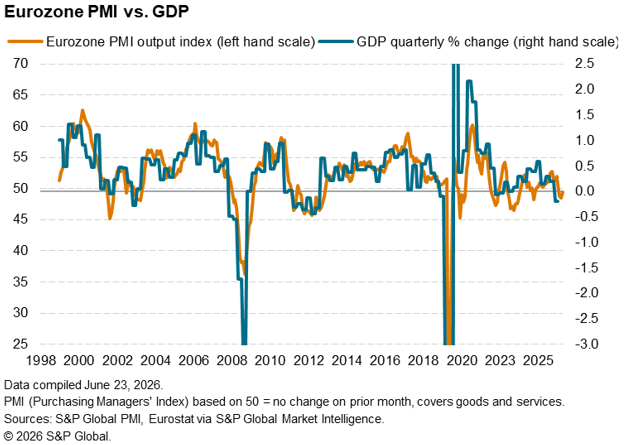

Flat picture for GDP in second quarter

The Eurozone PMI, compiled by S&P Global, indicated an easing in the pace of economic contraction, according to the early ‘flash’ estimate. The PMI rose from 48.5 in May to 49.5 in June. Although indicating a fall in business activity for a third successive month, the decline in June was only marginal and consistent with broadly flat GDP.

Similarly, while the average PMI reading of 48.9 over the second quarter is indicative of a small drop in business activity, it too is historically consistent with a flat picture for the broader economy as a whole.

Coming in the heels a reported 0.2% drop in eurozone GDP for the first quarter, a flat reading in the second quarter would indicate that the economy has avoided a dip into a technical recession (widely seen as being signalled by two successive quarters of falling GDP).

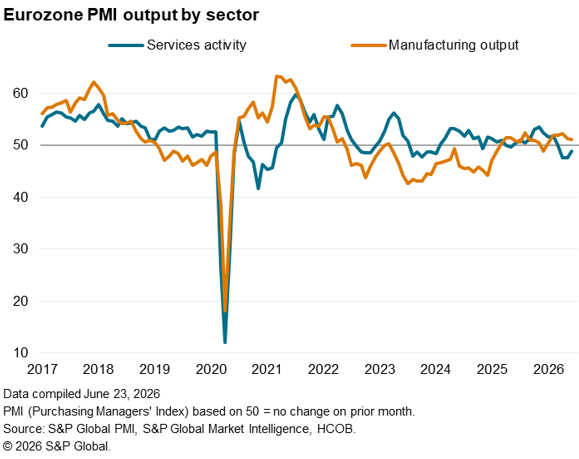

Service sector output contracted for a third successive month in June, though the rate of decline was the weakest seen over this period, buoyed by rising activity outside of France and Germany.

Manufacturing output rose modestly, helping offset some of the service sector weakness.

Supply shortages persist but price pressures moderate

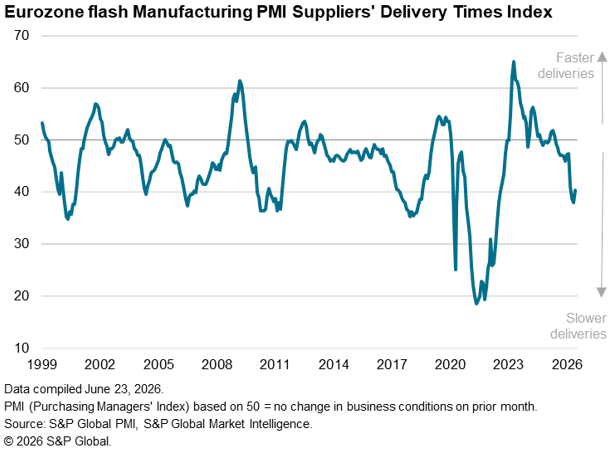

The lack of growth reflected a drop in new orders across goods and services for a fourth successive month, albeit with the rate of loss of service sector new business moderating. However, only a modest rise in factory orders was reported, suggesting that some of the recent war-related inventory building has started to fade. We note that the amount of inputs bought by manufacturers dipped slightly in June, having risen over the prior three months amid precautionary stock-building. That said, widespread supplier delivery delays continued to be reported, and in some cases, production was constrained by supply limitations.

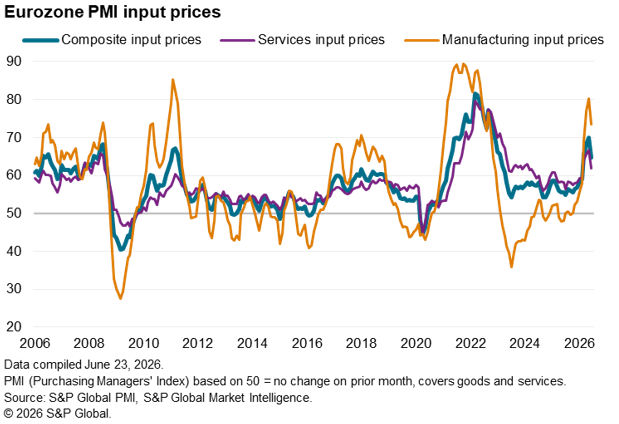

Supply shortages were also again commonly seen as the source of higher prices, leading to a further sharp increase in firms’ input costs that was among the largest seen over the past three years. The rates of increase nevertheless cooled notably in both manufacturing and services, aided in part by lower energy prices during the latter stages of survey data collection.

Slower cost growth fed through to the lowest rate of inflation for prices charged for goods and services seen for three months, pointing to a potential peaking of consumer price inflation.

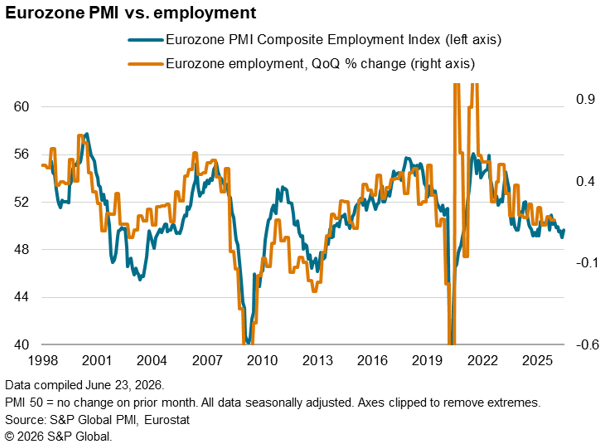

Falling employment

The PMI’s flash employment index meanwhile signalled a net loss of jobs for a sixth month running in June. Companies cited high operating costs and uncertainty about the demand environment as key drags on hiring.

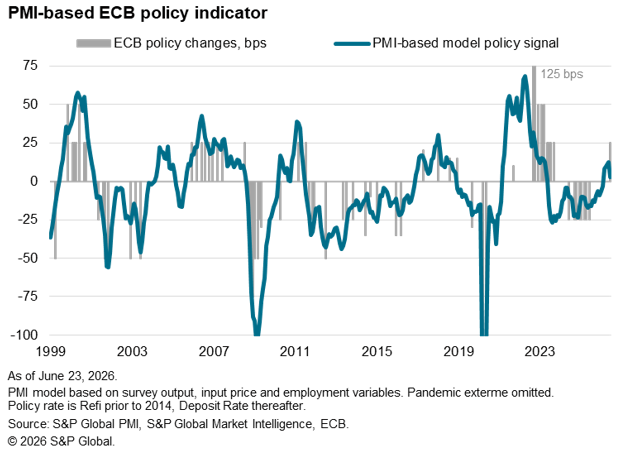

ECB rate hike “one and done”?

The flash PMI data come on the heels of the first rate hike from the ECB since 2023, taking the Deposit Rate from 2.0% to 2.25%, as policymakers erred on the side of caution with respect to managing inflation expectations. However, a simple policy indicator derived from PMI output, price and employment gauges has moved back closer to neutral policy territory in June, hinting that June’s data will add little support to any calls for any additional rate hikes in the near future.

Access the press release here.

© 2026, S&P Global. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

Read our latest PMI commentary here.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Theme

Location

Products & Offerings