Research — June 18, 2026

Dollarama postQ: FY2027 estimates edge higher despite margin normalization

By Dharmang Sapariya

Dollarama Inc. (TSX: DOL) reported a stronger-than-expected start to FY2027, with Q1 results coming in ahead of Visible Alpha consensus expectations across revenue, earnings and comparable-store sales, driven by resilient demand for value-oriented retail in Canada and continued execution on expansion initiatives. The beat was driven by solid Canadian performance, early contributions from international operations, and better-than-expected margin outcomes, even as management flagged a more challenging cost and merchandising backdrop in the second half.

Looking at earnings summaries compiled by S&P Global Pronto NLP, along with Visible Alpha pre-quarter consensus expectations and revised outlook, here are some key takeaways.

Key takeaways

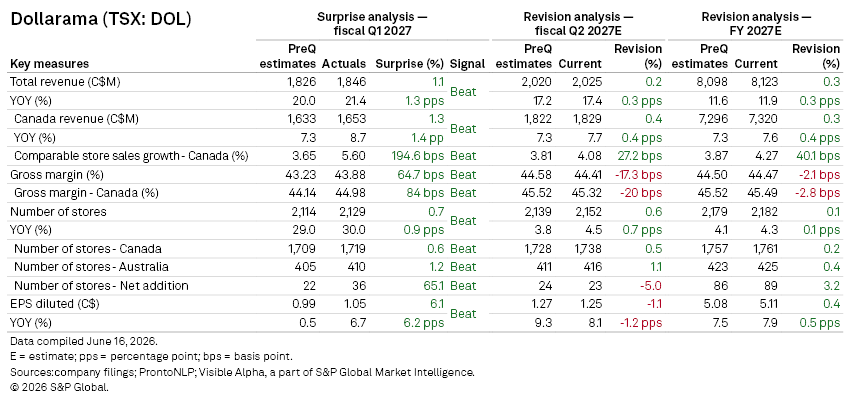

Q1 revenue rose 21.4% year-on-year to C$1.9 billion, modestly ahead of Visible Alpha consensus expectations by around 1%, supported by both network expansion and stronger-than-expected same-store sales.

Diluted EPS of C$1.05 beat consensus by roughly 6%.

Canadian operations remained the core driver. Revenue increased 9% year-on-year to C$1.7 billion, ahead of consensus expectations by 1.3%, while comparable-store sales growth of 5.6% significantly exceeded consensus forecasts, reflecting stronger-than-anticipated underlying consumer demand following a softer Q4 period.

Gross margins also came in ahead of expectations across both Canada and the consolidated group. Canada gross margin of 45% exceeded consensus by ~84bps, while the group margin of 43.9% beat consensus by ~65bps. The outperformance was attributed to smoother logistics execution and favorable operating leverage, partially offsetting ongoing input cost pressures.

Store growth remained a key structural driver. The company added 36 net new stores in the quarter, well above expectations of 22, bringing the total network to 2,129 locations.

Guidance

Full-year guidance was unchanged. Management reiterated:

- Comparable-store sales growth: 3–4%, broadly in line with consensus expectations

- Gross margin: 45.0–45.5%, ahead of consensus despite anticipated cost headwinds

- SG&A ratio: 14.1–14.6% of sales, unchanged

- Net store openings: 60–70 new stores, plus 60–80 renovations

However, management highlighted a key near-term risk: the transition toward lower-priced merchandise is expected to weigh more heavily in Q2 and Q3 as SKU changeovers accelerate. T

Analyst Q&A highlights

Management reiterated that Australia remains in a phased transformation, with rebranding contingent on completion of format conversion. Latin American operations, including Dollarcity, continued to show steady performance, with ongoing expansion in Mexico.

On inflation and costs, management acknowledged persistent pressure in China sourcing costs, particularly plastics, while signaling limited incremental SG&A leverage from here. Competitive intensity was also flagged as elevated in Australia.

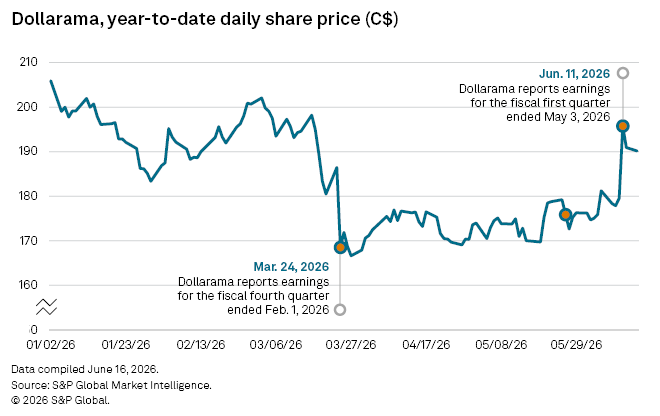

Share price reaction

Dollarama shares rose following the earnings release but later surrendered part of those gains, while remaining comfortably above pre-announcement levels.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Products & Offerings

Segment