Research — May 25, 2026

Q1 2026 stablecoin monitor: A 100-year-old community bank, tokenized deposits

Momentum for stablecoins and tokenized deposits continued to build in the first quarter of 2026, as banking and payment incumbents pushed deeper into real-world applications. An analysis of corporate filings, earnings calls and press releases reveals a sector in rapid transition.

The GENIUS Act is compelling offshore players to establish a US presence, while banks are splitting into two camps: those forming consortiums to upgrade settlement and those launching proprietary platforms. This report, compiled using S&P Capital IQ Pro's Document Intelligence 2.0 and its associated ChatIQ feature, finds divergent strategies across banks and payments companies.

Register for our upcoming webinar on May 27:

The APAC Stablecoin Playbook: Landscape, Use Cases & Strategy

The banking industry is still far from fully embracing digital assets, but the first quarter offered a glimpse of the multiple options available for incumbents. Some ambitious banks, like Old Glory Bank and VersaBank, see digital assets as the key to a complete digital reinvention. Most, however, seem to prefer safety in collaborations. They are joining consortiums to share the costs and risks of upgrading the settlement rails. Behind the banks making the stablecoin transition is an ecosystem of technology vendors that provide the essential integration work.

Meanwhile, real-world utility is emerging. Visa Inc. is pushing stablecoins as a 24/7 settlement layer between issuers and acquirers. In remittances, the demand is lopsided. Firms like The Western Union Co. see little interest from customers looking to send stablecoins, but a strong appetite from those on the receiving side in inflation-prone economies. A pragmatic focus on solving specific problems, rather than chasing hype, seems to define the current phase of digital asset adoption.

A century-old community bank's digital gambit

While the stablecoin landscape remains dominated by nonbank issuers, some legacy banks appear to see value in creating their own tokens.

A prime example is Texas-based Old Glory Bank (OGB), which describes itself as "an online community bank for all of America." The institution's origins trace back to a small Oklahoma bank from 1903. Following a 2022 acquisition, the bank was rebranded for a national, digital-first audience.

According to a regulatory filing connected to its planned SPAC merger to list on Nasdaq, the bank is developing a "Next Generation Banking Platform" to bridge traditional finance and digital assets. A key component is the creation of its own stablecoin, OGUSD.

The platform's features highlight the bank's ambition:

– A consolidated dashboard allowing customers to view their traditional fiat accounts alongside their self-custodial digital asset holdings.

– Instantaneous exchange between fiat and OGUSD, creating on-ramps and off-ramps.

– Access to crypto-secured credit lines and a patent-pending "Freedom Offramp" feature for conversion of crypto assets to fiat, deposited directly into OGB accounts.

Interestingly, the bank's strategy emphasizes technological independence. The platform is based on proprietary technology developed in-house to avoid vendor dependency.

Still, Old Glory Bank remains an outlier in the sense that it bets on a proprietary token to power its digital reinvention. Most banks seem to prefer the safety of consortiums to upgrade settlement rails.

We increasingly see banks band together to build shared, interoperable infrastructure for a new era of settlement. This collaborative approach allows institutions to pool resources and standardize technology, creating network effects far more quickly. This model is taking hold for both stablecoins and tokenized deposits.

In Europe, the Qivalis consortium recently expanded to 12 members with the addition of Spanish banking giant Banco Bilbao Vizcaya Argentaria SA. In Japan, a group of megabanks is jointly testing an interoperable yen-denominated stablecoin.

Similar propensity toward consortiums is apparent with tokenized deposits.

In a significant development, large American regional banks, including First Horizon Corp., Huntington Bancshares Inc., KeyCorp, M&T Bank Corp., Old National Bancorp and SouthState Bank Corp., formed the Cari Network. The bank-governed group is building a shared tokenized deposit platform on a private version of ZKsync's technology to enable instant, 24/7 interbank payments.

Global banks build their own rails

While consortiums build shared highways, some individual banking giants are leveraging their scale to create proprietary vehicles for their institutional clients. These closed-loop platforms are focused on solving specific, high-value problems in capital markets and cross-border payments.

The quarter's headline launch came from Bank of New York Mellon Corp., a custody titan, which officially began its tokenized deposit service. By creating "on-chain mirrored" versions of client funds, the platform allows for 24/7 settlement of collateral. Its initial client list features Citadel Securities LLC, Intercontinental Exchange Inc. and Ripple Labs Inc.

JPMorgan Chase & Co., an early leader, continued to expand its multi-chain strategy by bringing its JPM Coin to the Canton Network, aiming to create a programmable dollar that moves seamlessly across different blockchains.

Innovation is also emerging from specialists. VersaBank, a Canadian digital bank, added a foreign exchange function to its tokenized deposit platform this quarter. This allows for instant conversion between American and Canadian dollars within its distinct, bank-regulated system.

Stablecoin issuance moving to US-regulated entities

The need to comply with the GENIUS Act has brought some urgency to embed issuance and custody within the US-domiciled and regulated entities.

We previously discussed how several companies — both digital asset-leaning and payments companies — are pursuing OCC charters in the US. Sony Bank Inc., for example, is sponsoring a trust company in the US as it prepares to launch a dollar-pegged stablecoin for its entertainment and gaming businesses.

But a more notable shift came from Tether, the issuer of the world's largest stablecoin. In the first quarter, it teamed up with Anchorage Digital Bank, a federally chartered American institution, to launch a new token for users in the US. The partnership, cemented by a $100 million strategic investment from Tether into Anchorage, underscores a significant move onshore for the industry's biggest offshore player. Since its launch in late January, the new token has grown to a market capitalization of over $143 million, according to CoinMarketCap.

Tech vendors providing the plumbing for banks

Most banks rely on their incumbent technology providers to handle the integration of stablecoin capabilities. These core banking vendors, such as Fidelity National Information Services Inc. and Fiserv Inc., and digital-banking platforms, such as Alkami Technology Inc. and Q2 Holdings Inc., are in turn stitching together partnerships with specialized crypto firms such as New York Digital Investment Group LLC, Bakkt Inc., and Fireblocks Inc.

In the recent quarter, Q2 Holdings announced a partnership with Stablecore, a digital-asset banking specialist, to provide a turnkey solution for its clients. This will allow banks and credit unions, which already use Q2's platform to initiate payments, to offer stablecoin accounts and services without building the infrastructure themselves. Bank of Utah and Amarillo National Bank are among the first to sign on.

Signals from the C-suite

A review of recent earnings call transcripts reveals divergent strategies across the payments industry.

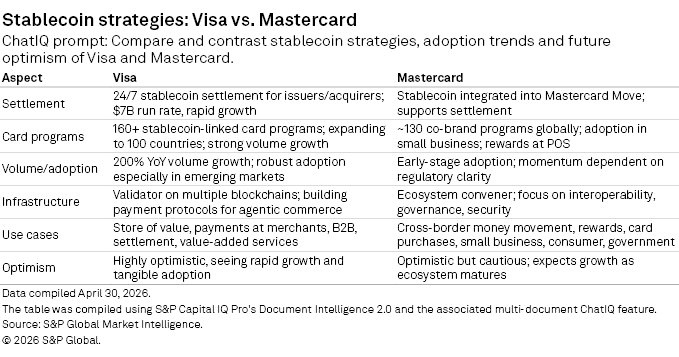

Card networks' contrasting stablecoin strategies

Visa and Mastercard Inc. are embracing stablecoins, with approaches diverging in both pace and posture.

Visa is aggressively building what it calls a "hyperscaling bridge," revealing a $7 billion settlement run rate. That is still a drop in the ocean for the card giant. For perspective, Visa settled close to $13 trillion among its 14,500 FI partners in 2025, all of which settled in fiat currencies from Monday through Friday. But it is now seeking to enable issuers to pay in stablecoins, and acquirers and merchants to get paid in digital dollars, seven days a week.

In contrast, Mastercard seems to adopt a more cautious "enabler" role, positioning for future growth by embedding stablecoins in its Move network. While it supports numerous co-brand programs, it has yet to see a "big pickup" in adoption and is awaiting greater regulatory clarity and ecosystem maturity.

Cross-border specialists' stablecoin posture

Among firms specializing in cross-border payments, there appears to be a clear spectrum of stablecoin adoption.

Payoneer Global Inc., which applied for a US trust bank charter in February, is attracting larger clients to its waitlist. The company seeks to issue its own stablecoin (PAYO-USD) to support stablecoin-enabled infrastructure for global businesses.

DLocal also appears advanced in adoption, with a fully launched infrastructure suite driving volume primarily for digital asset marketplace pay-ins and payouts.

Flywire remains relatively more cautious. Although it is testing a solution, it has not yet seen client demand and views stablecoins as another potential payment rail.

Remittance companies' stablecoin focus

Western Union's commentary reveals both the opportunities and constraints of real-world adoption.

The company sees no "clamoring" from its core consumer base to send remittances using stablecoins. But it is simply leveraging its proprietary stablecoin (USDT) to improve internal treasury and business-to-business settlement.

Where management anticipates consumer demand is on the "receive" side of remittances, such as receivers living in countries with high inflation. The company's Stable Card is designed for these users, allowing them to receive and hold their funds in a US dollar-denominated stablecoin, protecting their value before they spend it.

The money transfer operator is also seeing strong interest from third-party digital asset companies, including crypto wallet providers, whose customers need a reliable way to cash out their digital holdings into fiat currency.

Remitly, by contrast, is using existing stablecoins like USDC as an internal treasury tool to optimize FX costs and improve working capital efficiency.

Crypto-natives pushing stablecoins into new frontiers

Circle is focusing on diverse, real-world applications for USDC. Its payments strategy focuses on B2B use cases like cross-border settlement through its Circle Payments Network (running at a $5.7 billion TPV) and on-chain foreign exchange with StableFX. The company is also betting on the future of machine-to-machine economies and is developing stablecoin infrastructure for agentic AI payments.

Coinbase Global Inc. is embedding stablecoins as the core payment leg for its ambitious "Everything Exchange" vision, aiming to unite all asset classes. Like Circle, Coinbase sees stablecoins as the default payment method for AI agents.

Following the money

The venture capital interest in stablecoin-leaning fintechs remained strong in the first quarter of 2026, according to S&P Global Market Intelligence.

VCs wrote checks worth $574 million across 27 funding rounds, taking the cumulative total of investments directed toward building stablecoin ecosystem to $2.71 billion since the beginning of 2025. Sparking the investor interest in stablecoins was the GENIUS Act, which was introduced in the Senate and the House in the first half of 2025 and signed in July the same year. For a closer look at the broader fintech funding trends, read our recent quarterly funding report.

About the analysis

The S&P Capital Pro Document Intelligence tool, available for S&P Capital IQ Pro subscribers, is excellent for running large language model prompts on up to 20 filings or transcripts at a time. For instance, we selected transcripts for Visa and Mastercard for the last 90 days, and in the ChatIQ prompt, we entered the following text: Compare and contrast stablecoin strategies, adoption trends and optimism of Visa and Mastercard. It created a chart providing a contrast between the two companies, with key performance metrics mentioned where available. Refer to this article for a helpful tutorial on how to run your own analysis.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.