ECONOMICS COMMENTARY — 21 May, 2026

Japan flash PMI signals cooling economy as price index hits record high

The S&P Global Flash PMI® data showed output growth cooling in Japan to a five-month low in May, with the resulting modest rate of expansion representing a marked contrast to the near-record growth spurt seen just prior to the outbreak of war in the Middle East.

The war has seen prices surge higher, the PMI survey signalling a record rate of selling price increase across goods and services in May. Price rises were often linked to supply concerns stemming from the conflict, with supplier delays over the past two months running at some of the highest levels recorded by the survey.

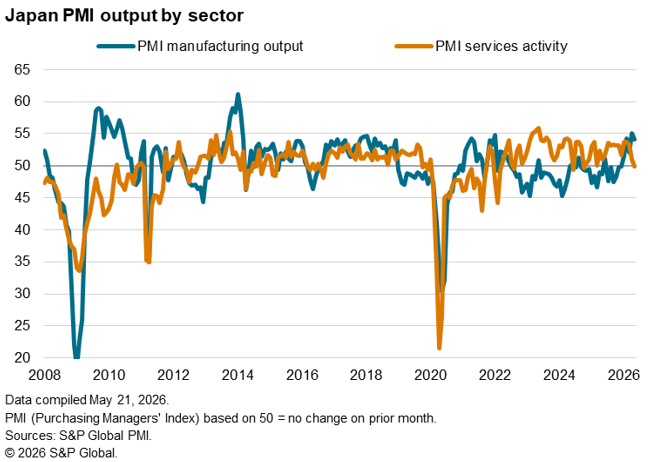

Inventory building to safeguard against further supply constraints has meanwhile helped boost manufacturing growth over the past two months to 12-year highs, but a more realistic picture of the economy’s health likely lies with the service sector Business Activity Index, which signalled a stagnation in May for the first time in 14 months amid the growing toll on demand from high prices.

Growth fades further

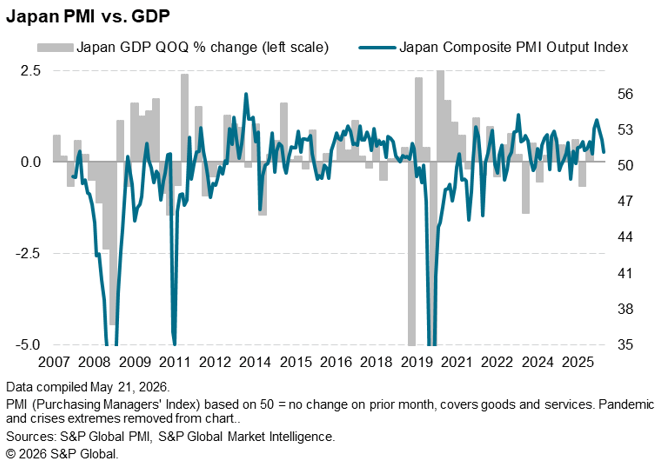

Weaker economic growth is signalled for May, as the headline S&P Global Japan PMI Composite Output Index slipped to a five-month low, according to the ‘flash’ reading, dropping for a third successive month from 52.2 in April to 51.1.

While February’s PMI had been a 33-month high, signalling one of the fastest rates of economic expansion yet recorded by the survey, growth has since slowed sharply alongside the ongoing conflict in the Middle East, which has caused both a surge in energy prices and spike in supply chain delays.

Record price rises fuelled by supply concerns

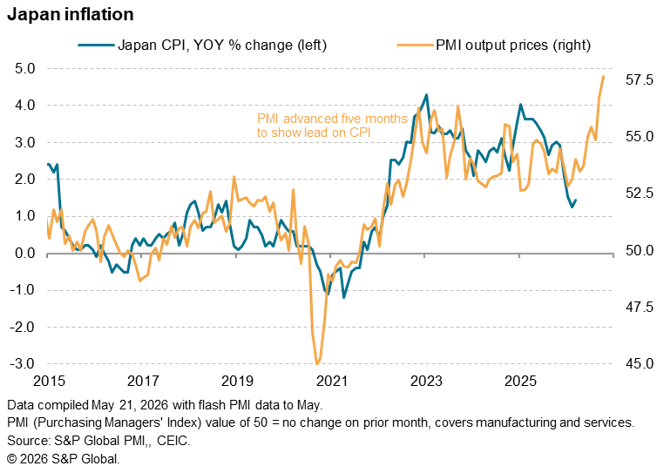

The inflationary impact of the war has exceeded anything previously recorded by the PMI. Firms’ input costs in May – measured across both goods and services – rose at the sharpest rate since late-2022, which in turn fed through to higher selling prices as firms sought to protect margins. The rate of selling price inflation hit the highest recorded in almost two decades of comparable survey history (since 2007).

It remains to be seen how the PMI data feed through to consumer prices. While higher inflation is anticipated, government measures such as the gasoline tax abolition and curbs on electricity and gas prices should help cap the headline rate of inflation.

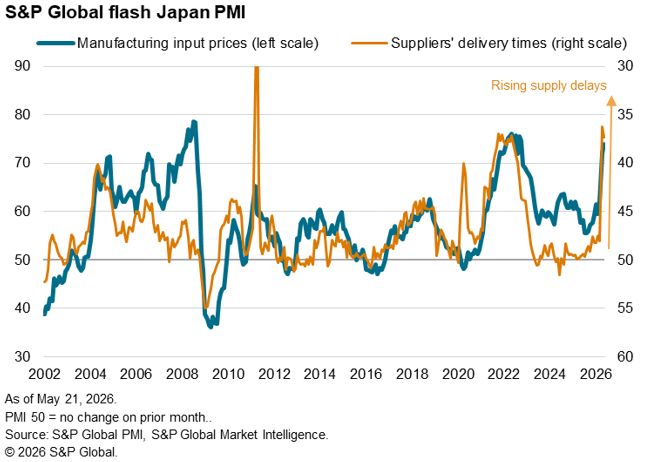

Price rises often reflected supply concerns, notably for energy, following the shipping disruptions emanating from the war in the Middle East. However, supply issues were by no means limited to energy, causing manufacturers’ supplier delivery times to lengthen sharply on average. Although less marked than in April, May’s lengthening of lead times was among the steepest seen in the history of the PMI in Japan.

Stock building boost

A near-term upside to the war has been a surge in stock building by companies reflecting concerns over future price hikes or supply availability issues. Input buying by Japanese manufacturers rose at the fastest pace for four years in May, resulting in a rare rise in inventories for a second successive month.

Such precautionary stock piling has boosted manufacturing output growth in many economies in recent months, most notably buoying Japan’s factory output growth to its highest for over 12 years in April, with growth remaining almost as strong again in May. Such inventory building will be temporary, however, posing downside risks to production in coming months once warehouses fill.

Meanwhile, the war has eroded growth in the services economy, notably hitting consumer spending, where business activity stagnated in May to end a 13-month spell of continual growth.

Outlook

The surge in price pressures adds to speculation that the Bank of Japan looks set to hike its policy rate to 1.0% in July. Higher borrowing costs will add to the growth headwinds created by the war in the Middle East in the coming months, notably via high prices for energy and shipping-related supply and cost factors, though much clearly depends on the duration of the conflict and associated supply disruptions.

We would meanwhile stress that the overall rate of growth signalled by the PMI is flattered somewhat by the temporary stock building that has been evident in manufacturing, reminiscent of COVID-era inventory accumulation. Production growth will fade once this inventory-fuelled demand wanes, potentially moving into reverse in a “bull-whip” stock cycle scenario.

Whether the service sector can avoid a slide into contraction remains a key near-term risk, which will be further heightened by rising borrowing costs. The possibility of the manufacturing sector moving into a cyclical downturn once stock building fades represents a secondary downside risk, which policymakers will need to monitor closely.

Access the press release here.

© 2026, S&P Global. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

Read our latest PMI commentary here.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Theme

Location

Products & Offerings