Research — May 28, 2026

Ghana's gold mining reforms: Resource nationalism by regulation

By Jason Holden

Ghana is not nationalizing its gold mines; it does not need to. The country's Minerals Commission has found a more elegant mechanism: mandating that all mining operations be conducted by Ghana-owned contractors, effectively separating the license holder from the physical act of mining. The result is a transfer of control — and the economic value that flows from it — from foreign mining companies to domestic firms without the headline risk or legal complexity of expropriation.

In January 2025, the commission issued the sixth edition of its Local Procurement List, requiring that all surface mining operations be conducted by completely Ghanaian-owned companies and all underground operations by firms with at least 50%-Ghanaian ownership. Most large operators — including Gold Fields Ltd. at Tarkwa and Damang — had already transitioned to contract mining models in anticipation of the rules. Three holdouts remained: Newmont Corp. (Ahafo North and South), AngloGold Ashanti PLC (Iduapriem) and Zijin Mining Group Co. Ltd.'s Ghanaian subsidiary. In letters sent between October 2025 and January 2026, the Minerals Commission gave all three companies a deadline of December 2026 to comply or face sanctions, including fines and potential mine shutdowns. The directive was reinforced in April 2026 when the government rejected Gold Fields' lease renewal application for the Damang mine and awarded the mining contract to Engineers & Planners, a Ghanaian contractor. Lands Minister Emmanuel Armah-Kofi Buah confirmed that only fully Ghanaian-owned firms would be eligible to apply for the asset. The message to foreign operators was clear: you may hold the license, but Ghana's citizens will do the mining.

While the government has stated that the contractors have demonstrated access to financing that meet the government's requirement that bidders show funding capacity of at least $500 million, there are questions around whether the local contractors will really get the capital to buy the earthmoving fleets required to operate these large assets. A significant funding gap could arise because lenders will want high risk premiums, and Ghanaian banks generally lack the balance sheet for this level of heavy equipment financing. Foreign operators will likely have to act as de facto financiers to avoid production halts, either by leasing their current fleets to the local contractors or by offering corporate guarantees for the contractors' debt. This is a high-risk situation in which the foreign miner gives up operational management of the pit but is still responsible for the underlying debt.

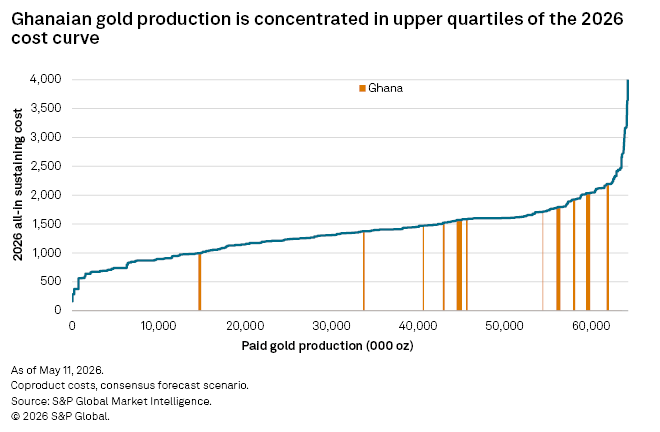

Ghana is already a high-cost gold producer, estimated to have an average all-in sustaining cost (AISC) of $1,676 per ounce in 2026 — the second-highest in Africa behind South Africa. Some of the largest mines, such as Ahafo and Akyem, are already grappling with increasing depth and lower grades, requiring more intensive mining activity. Ghana's AISCs are expected to increase 0.67% in 2026, but that is before accounting for the full extent of the surge in fuel costs from the US-Israel war with Iran. Alongside the transition in mining contractors and resulting operational efficiencies, our modelling suggests Ghana's AISC could climb close to $1,800-$1,900/oz.

Ghana's new approach to resource nationalism could achieve many of the same economic objectives of full nationalization while avoiding the catastrophic production collapses seen in Zambia and the Democratic Republic of Congo. There are risks, however, as contract mining introduces a principal-agent problem. The license holder loses direct control over the mining operations — specifically, the drill-and-blast, load-and-haul and ground support — which determine ore recovery, dilution and cost. If the Ghanaian contractors lack the technical capacity, equipment or management systems to operate at the same standard as the foreign operator's own teams, mine performance will deteriorate.

Ghana's reforms are part of a broader continental trend. Mali enforced a revised mining code against Barrick Mining Corp. in November 2025, Tanzania renegotiated its fiscal terms with Barrick in 2017, and the DRC revised its mining code in 2018. What distinguishes Ghana's approach is its sophistication: rather than seizing assets or raising royalties to punitive levels, it is restructuring the industry's operational organization to ensure that Ghanaian firms perform the physical work of extraction. It is resource nationalization by regulation rather than by decree. Whether it produces better outcomes than the nationalization model it seeks to improve upon will depend on whether Ghana's domestic mining contractors can deliver the operational performance that the geology demands.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.