ECONOMICS COMMENTARY — 22 May, 2026

Flash PMIs signal stagflation among the major developed economies as growth falters amid price hikes

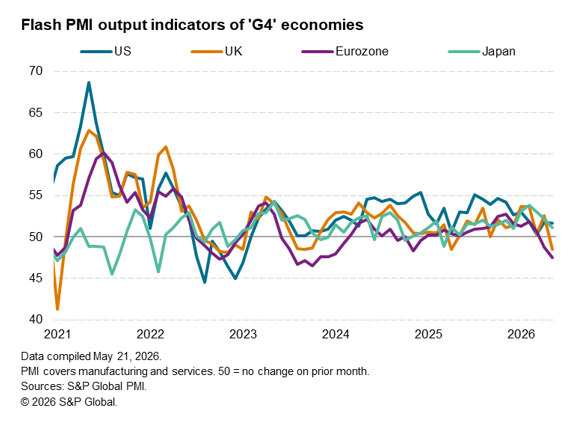

S&P Global’s flash PMI surveys showed business growth grinding to a halt in May as the ongoing war in the Middle East exerts a growing toll. Europe is hardest hit, with the UK and eurozone economies now both in decline, but the US and Japanese expansions have also shifted down gears since the onset of the conflict.

Services have generally reported the worst deterioration in demand conditions, whereas manufacturers have continued to benefit in May from stock piling. This precautionary stock build will only be temporary, however, and reflects growing concerns over supply conditions (with supply availability having deteriorated markedly again in May) as well as worries over prices hikes. Manufacturing input price inflation accelerated sharply among the major advanced economies to reach a four-year high, with energy prices also pushing up service sector inflation.

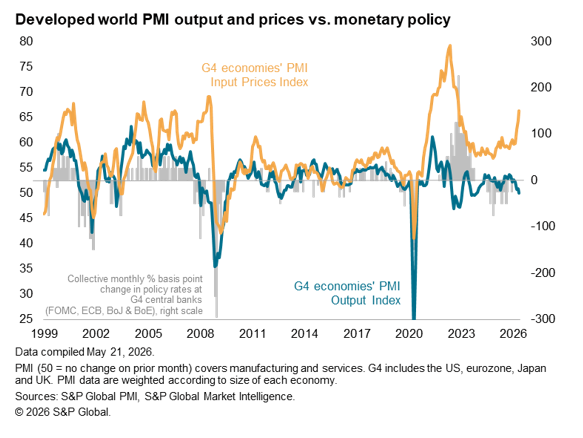

These indications that the major economies are already facing stagflationary conditions poses a major challenge to central bank policymakers.

Major advanced economies stagnate as war hits growth

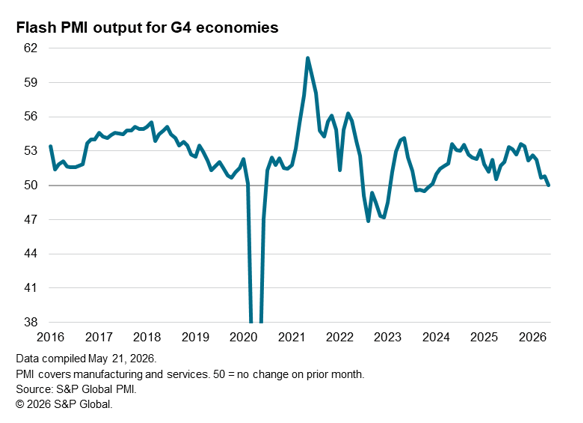

Business activity growth across the four largest advanced economies – the US, eurozone, Japan and the UK (the ‘G4’) – ground to a halt in May. The stagnation ends a period of continual expansion seen since December 2023, attributable to a growing toll from the war in the Middle East.

S&P Global’s PMI’s output index for the G4 economies fell to 50.0 in May, a level signifying no change in activity on the prior month, down from 50.8 in April. The stalling of growth contrasts markedly with the robust rate of expansion seen throughout the second half of last year and into the start of 2026, with the outbreak of war at the end of February having been widely cited by surveyed companied as a key cause of weaker growth in recent months.

The survey data indicate that, among the G4, Europe has so far been hardest hit by the war. Business activity fell in both the eurozone and UK during May, the former seeing a second successive monthly decline with the rate of contraction accelerating to the fastest since October 2023. The UK’s decline was the first recorded since April of last year and was the joint-steepest recorded since November 2022.

Growth meanwhile weakened for a third successive month in Japan, taking the pace down to the slowest seen so far this year and representing a substantial slowdown from the 33-month peak rate of growth seen in February.

While the US was consequently the best performing of the G4 economies, its growth rate remained unchanged from the lacklustre rate seen in April, putting the economy on course for its weakest quarterly expansion since 2023 unless growth picks up in June.

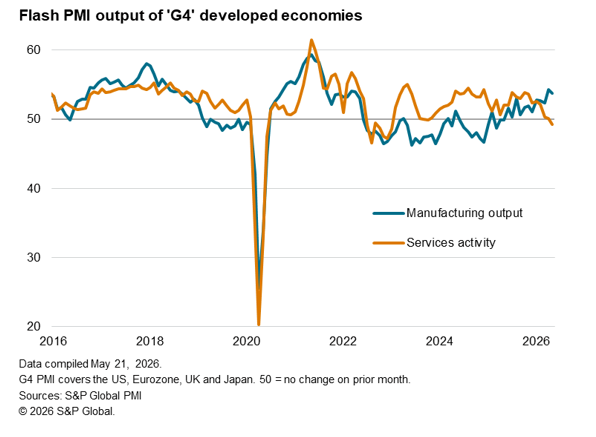

Service sector malaise contrasts with factory growth spurt

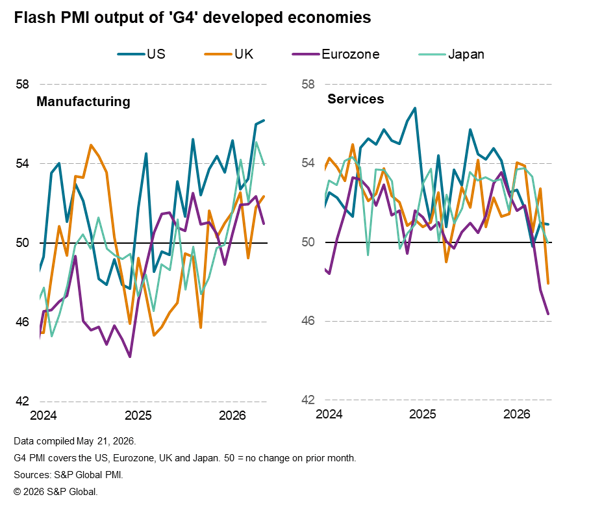

The deterioration in growth among the major advanced economies was led by the service sectors, which collectively reported a fall in output in May for the first time since October 2023. An especially steep fall in eurozone services activity was accompanied by a marked reduction in the UK. Both declines were the sharpest since the COVID-19 lockdowns of early 2021. Japan’s service sector growth meanwhile stalled and the US reported only a modest upturn, registering the third-weakest performance since 2023.

Weakened service sector activity rates were commonly blamed on the rising cost of living, which dampened spending power, notably via higher fuel and energy prices. However, activity growth looks to have also slowed in financial services (notably real estate linked businesses) amid concerns over higher interest rates, and a broader slowdown in corporate spending on services is also signalled, reflecting heighted uncertainty and rising costs.

In contrast, robust manufacturing output growth was again reported across the G4 economy as a whole, the rate of expansion dipping only slightly from April’s growth surge, which had seen the largest monthly improvement in factory output since August 2021.

Factory output gains were seen in all four economies, led by the US, where production growth hit a four-year high.

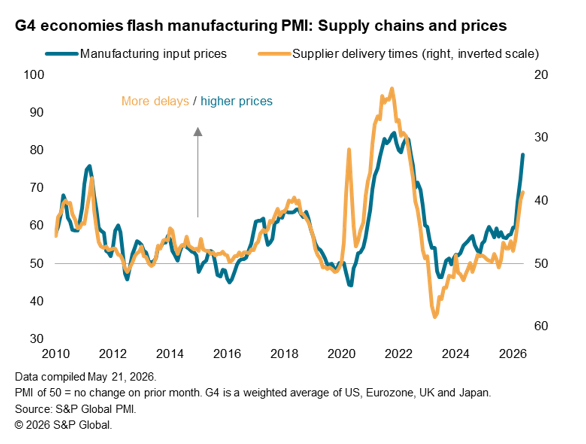

Supply shock

Survey responses indicate that the manufacturing sector’s improved performance since the outbreak of war is partly tied to an increase in precautionary stock building as companies seek to safeguard against war-related supply disruptions and potential further price hikes.

In this respect, supply delays across the G4 economies were more widely reported than at any time since July 2022. Although the incidence of delays is not as extreme as that seen during the pandemic, the war otherwise represents the biggest supply chain shock since the Japanese earthquakes and tsunami of 2011 (read more about the PMI Suppliers’ Delivery Times Index as a gauge of supply chain stress here).

Price pressures intensify

Companies report that prices have meanwhile risen not just on the back of the energy price spike caused by the war, but also due to increased shipping rates and the scramble for supplies more generally. Measured across the G4 economies, manufacturing input prices rose in May at the sharpest rate for four years.

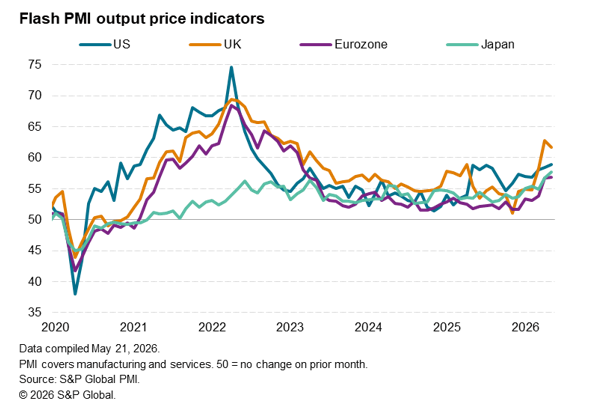

While the services sector reported a more muted rise in input cost inflation than manufacturing, the rate of cost growth across the G4 services economies nonetheless rose to its highest since February 2023, widely linked to higher energy prices.

These increased costs again fed through to higher selling prices for both goods and services, with overall rates of inflation climbing sharply higher in all G4 economies bar the UK, though the latter nonetheless still reported the sharpest increase of the four economies.

Stagflation

In all cases, the PMI data point to marked increases in consumer price inflation in the coming months as war-related price hikes feed through to households. However, at the same time, economic growth in the advance economies as a whole has stalled, with Europe now in contraction. This stagflationary environment poses a major challenge to central banks, who will need to decide whether the inflation spike warrants rate hikes, or whether slowing growth will prevent inflation from becoming entrenched and avoid a tightening of policy.

© 2026, S&P Global. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

Read our latest PMI commentary here.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Theme

Location

Products & Offerings