ECONOMICS COMMENTARY — 21 May, 2026

Flash PMI shows UK economy sinking into decline in May as prices surge higher

The UK economy is facing a perfect storm as rising political uncertainty adds to the growing impact from the war in the Middle East. Businesses are reporting falling output, surging inflation, supply shortages and job cuts in May.

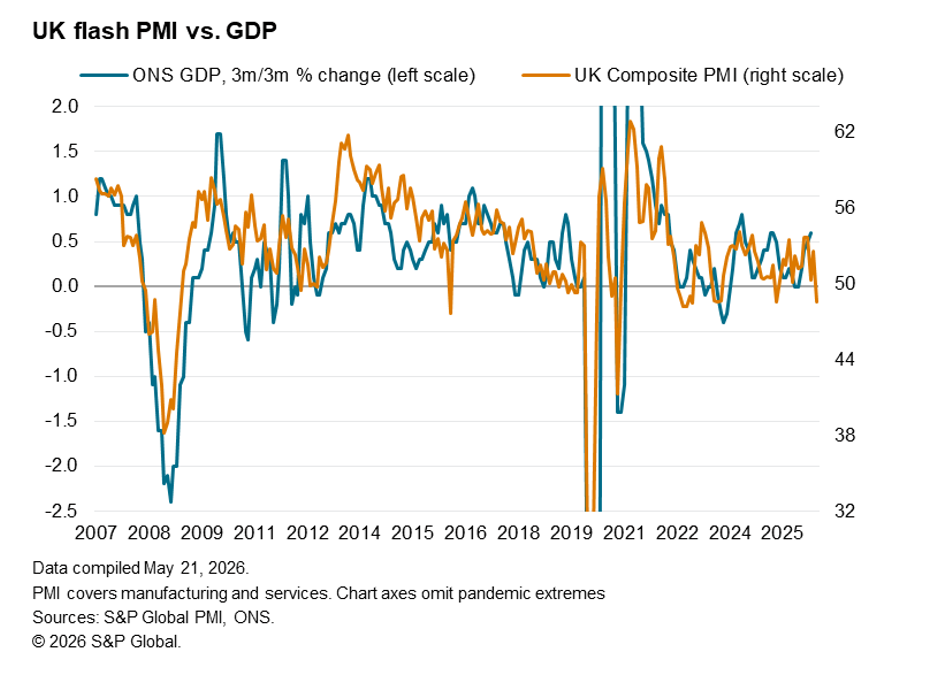

The May PMI data indicate that the economy contracted at a 0.2% quarterly rate, representing a marked contrast to the robust growth seen earlier in the year. The blame lies first and foremost with the war in the Middle East, though companies are also noting that domestic politics are taking an increasing toll, driving uncertainty higher, in turn deterring spending, hiring and investment.

Things could well get worse in the coming months, as we have been seeing some support to manufacturing from precautionary stock building which will inevitably fade once warehouses are full.

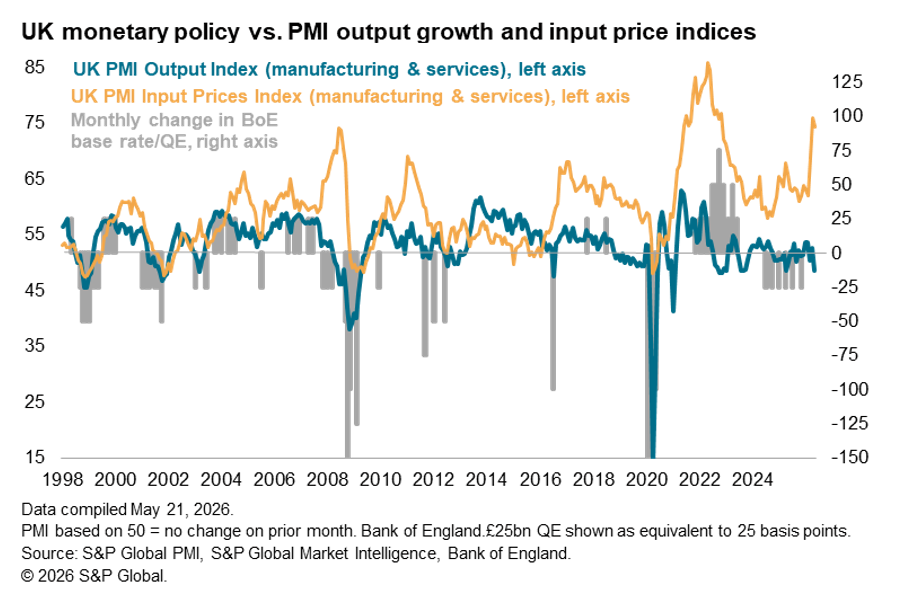

Just as the economy shows signs of sinking into decline, prices are surging higher to herald a marked upturn in inflation in the months ahead as these costs pass through to consumers.

This combination of a faltering economy and spiking price pressures leaves the Bank of England in a major quandary, facing the growing need to hike rates to help contain inflation but thereby adding to recession risks.

Output falls in May

The headline Composite PMI Output Index fell sharply in May, according to the preliminary ‘flash’ reading, down from 52.6 in April to 48.5. Dropping below the 50.0 no change level, the PMI signalled the first fall in output since April of last year, when the US tariff announcement caused a brief downturn. May’s decline matched that seen last April to represent the joint-sharpest fall in output since late 2022.

May’s flash PMI reading is consistent with the economy contracting at a 0.2% quarterly rate.

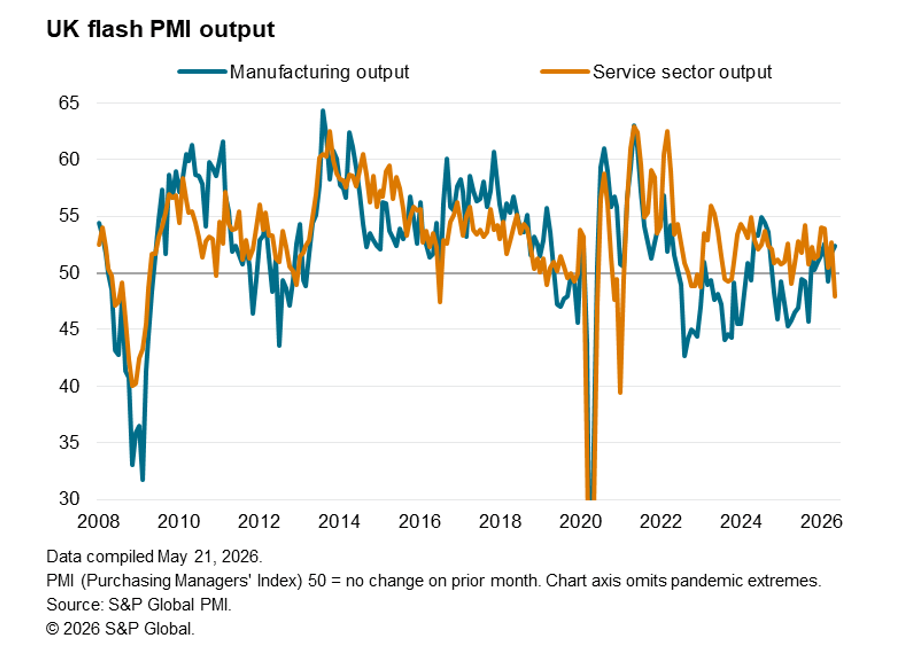

Service sector activity slumps

The decline was led by the service sector, where business activity fell at a rate not seen since the COVID-19 lockdown in January 2021, reversing a growth rebound seen in April. New orders placed at service providers fell for a third straight month, widely liked to rising prices, travel disruptions and uncertainty resulting from the war in the Middle East, exacerbated by heightened domestic political uncertainty.

The steepest downturn in demand was reported in the consumer-facing industries such as leisure and recreation, though an increasingly broad-based drop in activity meant any growth was limited to IT.

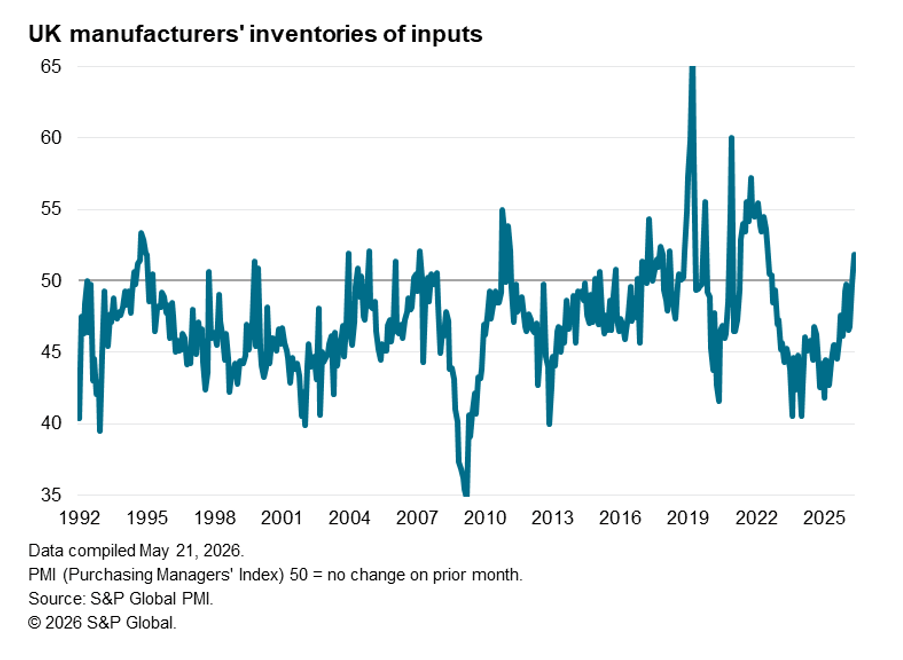

Manufacturing sees respite amid stockbuilding

Manufacturing fared better than services, though its improved performance looks unsustainable. While factory growth accelerated to a three-month high, with output rising for a second month after a brief fall in March at the start of the war, this heightened activity in the goods-producing sector was again in part a reflection of manufacturers and their customers building safety stocks amid concerns over future price hikes and supply shortages.

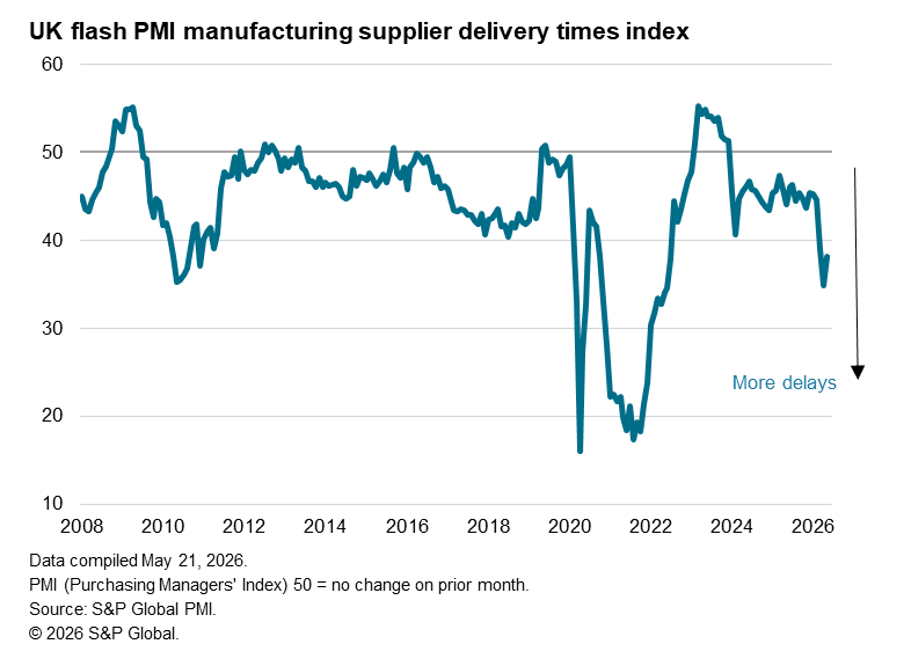

Manufacturers’ concerns over supply availability are highlighted by May seeing a further marked lengthening of supplier delivery times. Although less severe in May than seen in April, the lengthening of supplier lead-times since the outbreak of the war in the Middle East represents the biggest supply chain shock since Russia’s invasion of Ukraine in early 2022.

In addition to the direct impact on supply lead-times of shipping being affected by the closure of the Strait of Hormuz, the buying of buffer stocks due to war-related concerns has piled further pressure on suppliers. To illustrate, the amount of inputs stocked by manufacturers rose in May at the sharpest rate since July 2022.

Confidence sinks lower

The combination of the war and domestic political uncertainty also pulled companies’ growth expectations for the year ahead lower. Business confidence about the next 12 months is now the lowest since April of last year and among the lowest readings seen since comparable data were first available in 2012.

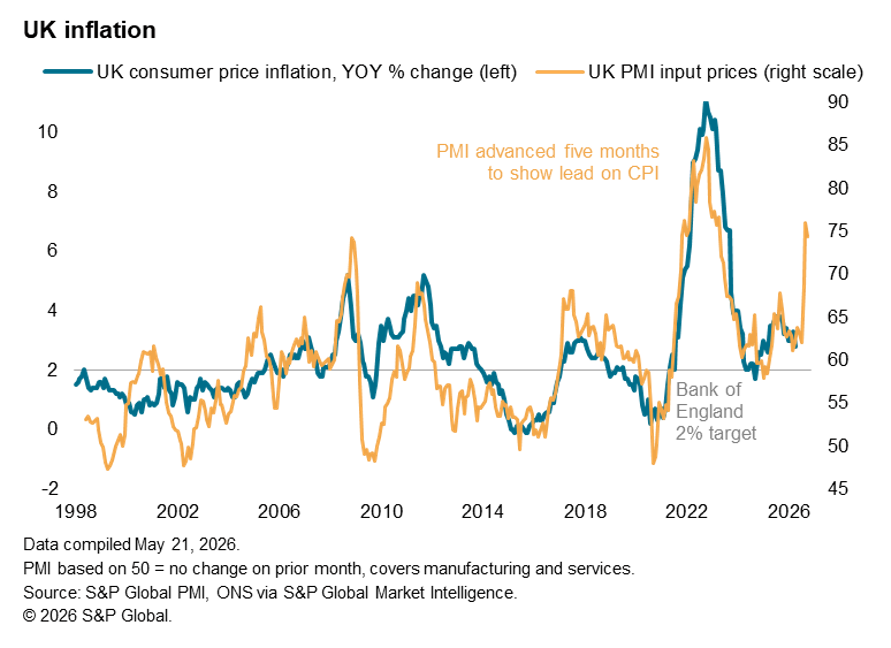

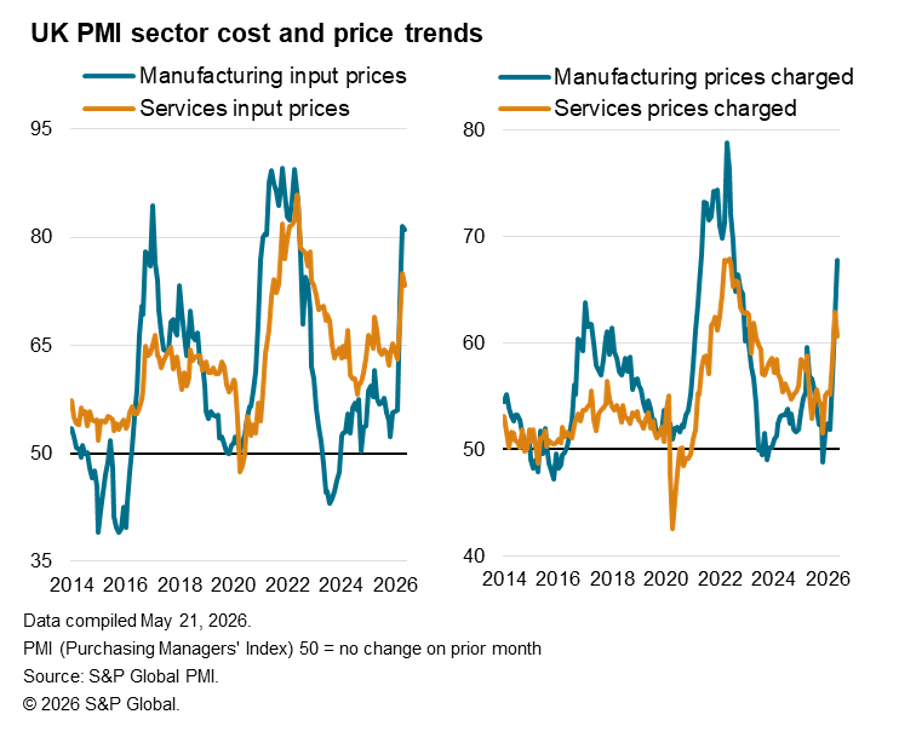

Inflation set to rise sharply

Prices meanwhile jumped higher again in May, largely in response to the impact of higher energy prices filtering through the economy.

Average input costs across both manufacturing and services surged at a rate only slightly below that seen in April, the past two months having seen the steepest price rises since the energy shock in 2022. Barring the pandemic and invasion of Ukraine, the outbreak of war in the Middle East has seen the biggest surge in companies’ costs since comparable data were first available in 1998. These cost increases are indicative of consumer price inflation spiking sharply higher in the coming months.

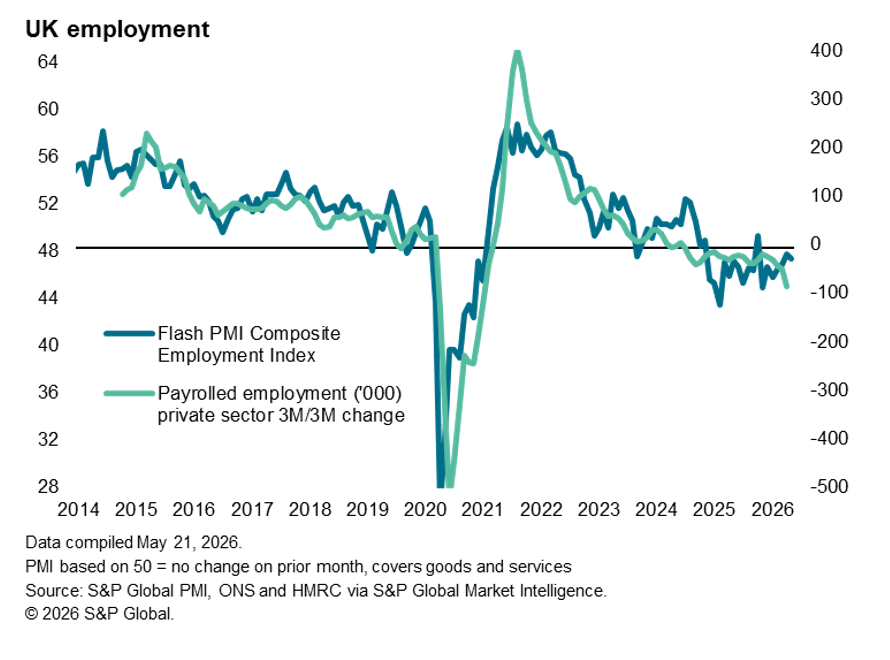

Employment cut further

Companies meanwhile cut back on payroll numbers in May, with employment declining for the twentieth straight month. Jobs have now been cut continuously since the autumn 2024 Budget, with employers commonly blaming a combination of higher staffing costs linked to government policies such as higher NI contributions and hikes in the Minimum Wage, alongside weak sales and heightened uncertainty. Job losses in May were focused on the service sector, led by leisure industries such as hotels and restaurants.

Read the press release here.

© 2026, S&P Global. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

Read our latest PMI commentary here.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Theme

Location

Products & Offerings