ECONOMICS COMMENTARY — 10 Apr, 2026

Week Ahead Economic Preview: Week of 13 April 2026

The following is an extract from S&P Global Market Intelligence's latest Week Ahead Economic Preview. For the full report, please click on the 'Download Full Report' link.

UK and mainland China GDP plus inflation data for the US and eurozone

Highlights of the economic data flow in the coming week include the publication of GDP data for both mainland China and the UK, as well as industrial production and inflation numbers for the US and eurozone.

A key economic release in the coming week is the publication of first quarter GDP data for mainland China. The release includes detailed data on industrial production, retail sales and investment, and is preceded by trade data, all of which will provide an insight into whether growth has proven resilient in the face of global events. The current consensus is for GDP growth to have accelerated from a 4.5% pace in the fourth quarter to 5.0%, according to LSEG polling. The detail will also be eyed for clues as to the extent to which any expansion is being driven by manufacturing and trade, which we expect to have provided a major boost to GDP, or whether domestic consumption is picking up to help rebalance the economy. A concern is that any purely export-led growth will fade in the second quarter as the war in the Middle East hits trade and impacts demand.

Official GDP data are also updated for the UK, adding to the economic picture in the lead up to the outbreak of war. Prior data indicated no growth in January, albeit with the three-month-on-three-month growth rate accelerating slightly to 0.2%. The PMI survey data pointed to an uptick in February, though the more recent March PMI survey data have pointed to a return to stagnation due to the energy price rise and uncertainty caused by the war.

Eurozone industrial production, trade and inflation data will also be important to assess for policy implications. The ECB has shifted to a more hawkish stance following the energy price rise, and an April rate hike remains very much on the table. However, much will depend on the degree to which growth might weaken further in April after the PMI signalled a near-stalling of the eurozone economy in March.

In the US, the economic data include fresh insights into both growth and inflation. The industrial production numbers for March are accompanied by survey data from the NFIB as well as New York and Philly Feds for April. However, a key focus will also be on producer price data, revealing the impact of war-related price increases on businesses, as these costs will provide an important hint to the developing inflation picture.

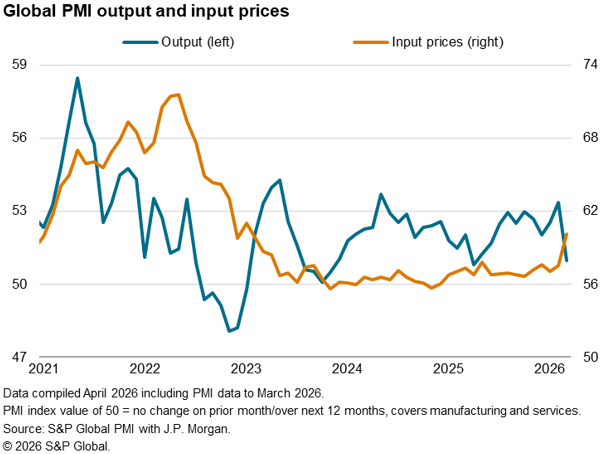

Chart of the week: War drives global PMI lower as prices surge

March’s PMI surveys produced by S&P Global provided the first indication of changing economic conditions since the outbreak of war in the Middle East, and signalled an unwelcome combination of markedly slower growth and accelerating inflation.

Output growth moderated worldwide to one of the greatest extents seen since the global financial crisis of 2008-9, cooling to its weakest since last April. Firms’ input costs meanwhile rose sharply for both goods and services thanks principally to surging energy and other raw material costs, rising globally at the fastest rate since January 2023.

Read more here.

© 2026, S&P Global. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

Read our latest PMI commentary here.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Theme

Location

Products & Offerings