Research — April 14, 2026

Visible Alpha breakdown of US airlines’ first-quarter 2026 earnings expectations

By Mrunalini Mandore and Neha Jain

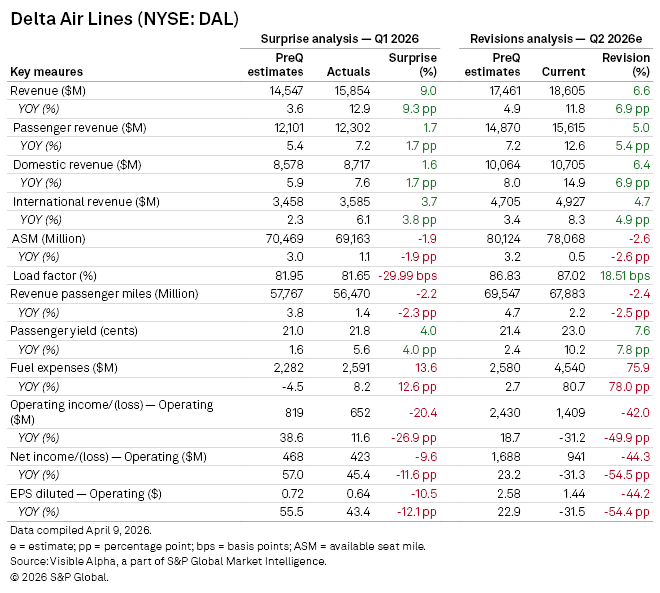

Delta reports Q1: Revenue strength masks margin strain as fuel costs bite

Delta Air Lines Inc. (NYSE: DAL) has set the tone for the US airline's earnings season with first-quarter results that highlight resilient demand supporting revenues, but rising costs eroding profitability and clouding the near-term outlook.

On the surface, Delta delivered a robust performance. Total revenue of $15.9 billion in Q1 beat Visible Alpha consensus preQ estimates of $14.5 billion. This upside was broad-based across passenger segments, with domestic and international revenues both exceeding estimates and showing stronger-than-expected growth. The beat is consistent with what Delta Air Lines highlighted in its release: resilient travel demand, particularly in premium and international markets, continuing to support top-line momentum.

However, the operating backdrop was less constructive. Capacity (available seat mile), load factor, and traffic (revenue passenger mile) fell short of consensus expectations, highlighting that revenue outperformance was driven primarily by pricing rather than volume growth.

The more pronounced negative surprise came on costs. Fuel expenses for Q1 came in 14% above consensus expectations, swinging to 8.2% year-on-year growth versus an expected decline. This drove a significant miss at the operating income level (-20%) and flowed through to EPS, which fell short of expectations by over 10%.

Importantly, the revisions to Q2 expectations suggest that these pressures are not transitory. While revenue estimates have been revised meaningfully higher with growth now expected at 11.8% year-on-year, this optimism is more than offset by a sharp increase in cost expectations, most notably fuel. As a result, operating income, net income, and EPS estimates have all been cut materially (by ~50%+), with growth expectations swinging into negative territory.

Delta’s postQ picture is one of stronger-for-longer revenue but weaker-for-longer margins. The carrier appears well-positioned to capitalize on sustained demand and pricing strength, but cost inflation, particularly fuel, is eroding incremental revenue gains, leading to a reset in profitability expectations.

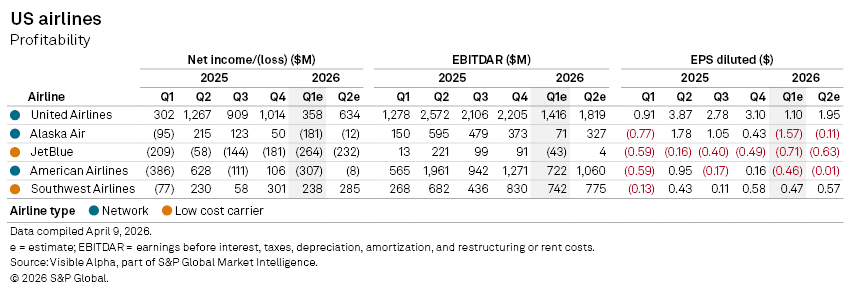

Industry outlook: Q1 expectations for other US airlines

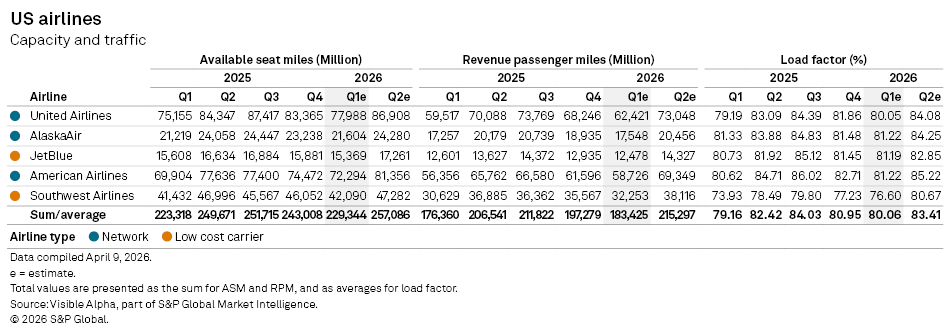

Q1 2026 expectations across other US airlines reinforce and broaden the trend seen in Delta’s results. Analyst expectations reflect that while the demand environment remains solid, profitability is increasingly dictated by cost control and operating leverage rather than pure revenue growth.

With United Airlines Holdings Inc. (NASDAQ: UAL), Alaska Air Group Inc. (NYSE: ALK), JetBlue Airways Corp. (NASDAQ: JBLU), American Airlines Group Inc. (NASDAQ: AAL), and Southwest Airlines Co. (NYSE: LUV), reporting later in the month, consensus expectations point to resilient top-line growth, but with margin compression emerging as the defining theme, as strong demand and pricing power are increasingly offset by elevated fuel and operating costs, driven in part by geopolitical disruptions, most notably the Iran conflict and its impact on crude oil markets.

Demand to hold up, with disciplined capacity

On the demand side, analysts expect year-on-year capacity growth across the group to remain measured, largely in the low-single-digit range. Notably, JetBlue is expected to see a pullback in capacity with a 1.5% year-on-year decline in available seat mile (ASM), signaling a broader shift toward supply restraint to protect yields.

Traffic is expected to track slightly ahead of capacity growth, with revenue passenger miles projected to increase across most carriers, as demand remains intact, particularly in domestic and leisure segments, while the industry avoids overcapacity.

Load factors are consequently expected to edge higher, with the group average rising to 80.4%, up around 80 basis points from Q1 last year.

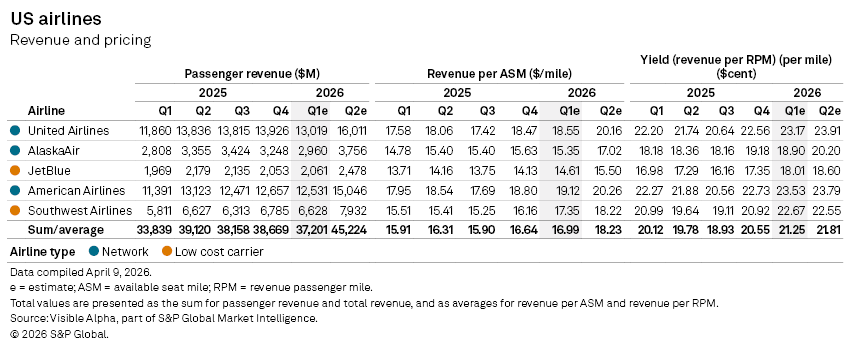

Revenue growth to remain pricing-led

Analysts expect continued strength in passenger revenues across US airlines, but as seen in Delta’s Q1 performance; this is being driven more by pricing than volume.

Revenue per available seat mile (RASM) growth is expected to remain positive across all carriers, while yields (revenue per passenger mile) are expected to climb, indicating that airlines are continuing to extract higher fares, supported by premium cabin demand, segmentation strategies and constrained capacity.

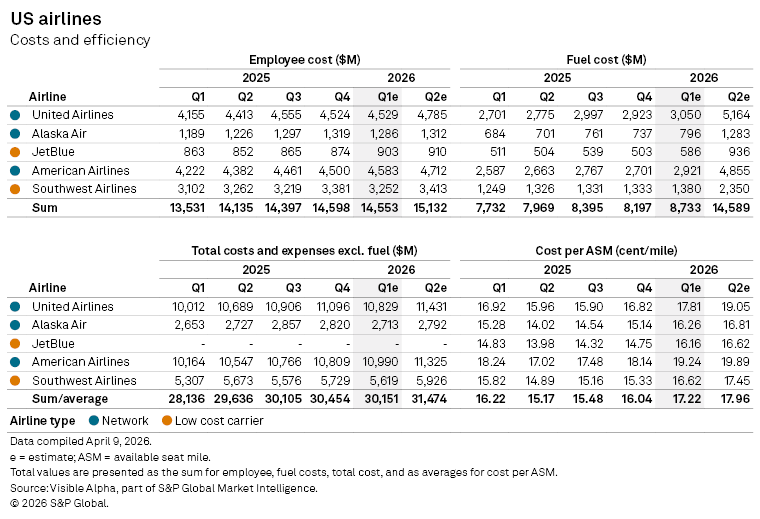

Costs seen rising, but not yet overwhelming in Q1

Fuel remains the key swing factor for the industry. Crude oil prices have risen meaningfully amid supply concerns linked to the conflict in the Middle East, resulting in rising jet fuel prices feeding into airline cost structures at a time when most US carriers have limited hedging exposure. While oil prices have been contracting as of Wednesday, April 8, on the back of a ceasefire announcement in the US/Iran conflict, jet fuel prices are unlikely to adjust as quickly.

Against this backdrop, Q1 represents a period where airlines still benefit from a partial lag in fuel cost inflation. While jet fuel prices have risen meaningfully and are expected to feed into rising fuel expenses for the carriers in Q1, the full incremental impact of higher fuel costs is expected to be more visible in Q2 and beyond.

Profitability remains under pressure

The profitability outlook for early Q1 points to a more challenging earnings environment despite healthy demand, as rising costs, particularly fuel, begin to erode the benefits of sustained revenue strength.

At a carrier level, profitability remains mixed. United is expected to deliver a solid improvement in net income and earnings per share compared to Q1 last year, supported by its scale and premium exposure, while Southwest stands out as a relative bright spot, returning to profitability with positive earnings after a loss in the prior year, driven by its company-wide transformation plan finalized in late 2025.

Overall, the early read on Q1 points to an industry still benefiting from solid demand and disciplined capacity management, but increasingly constrained on the cost side. Revenue growth remains healthy and largely pricing-driven, supported by stable load factors and modest traffic expansion across carriers. However, elevated fuel costs are emerging as the key pressure point, driving margin compression and resulting in earnings misses and downward revisions to near-term profit expectations.

While top-line momentum is expected to persist in the near term, the numbers suggest that profitability will be more uneven across carriers, with performance increasingly dependent on each airline’s ability to control costs, manage exposure to fuel volatility, and sustain pricing power in a more challenging operating environment.

Content Type

Products & Offerings

Segment