ECONOMICS COMMENTARY — 13 Apr, 2026

UK recruitment survey hints at stabilising labour market, but cost concerns dampen pay growth and demand for staff

The latest survey of UK recruitment consultancies indicated that recruitment activity came close to stabilising at the end of the first quarter. The steadying of the job market marks a contrast to the steep jobs decline recorded over much of the prior three years.

However, rising business costs, which have been exacerbated by rises in the minimum wage and the war in the Middle East and the subsequent surge in energy prices, continued to impact job creation and dampened pay growth. Pay growth was also limited by improved labour supply. Staff availability rose at the quickest pace in three months, with the current stretch of rising labour supply the longest recorded in nearly 20 years of data collection.

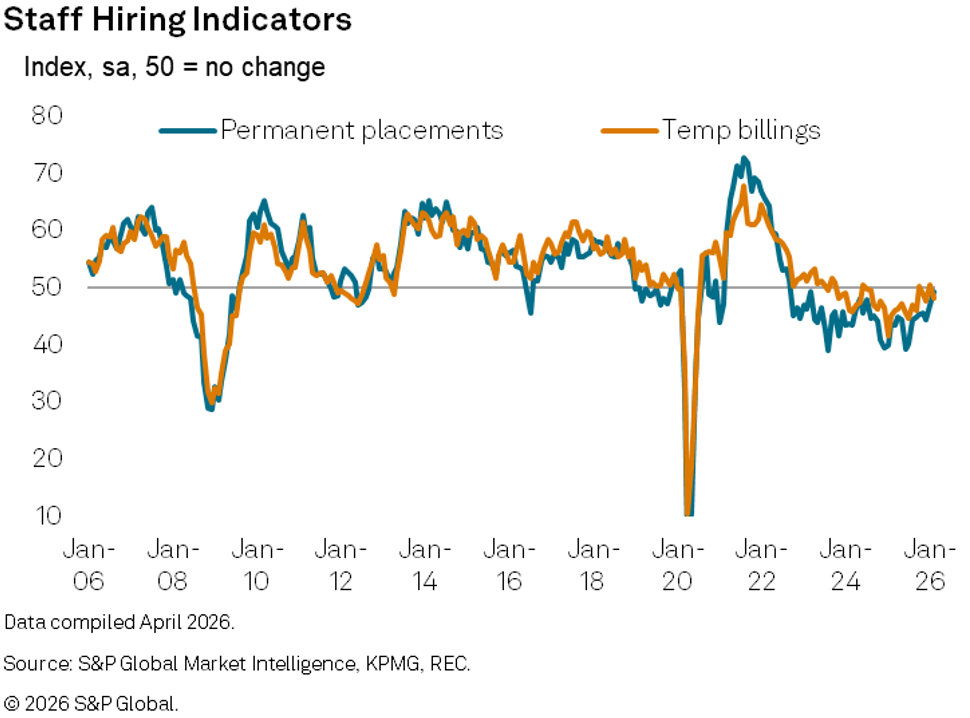

Permanent staff hiring down only slightly in March

March survey data compiled by S&P Global Market Intelligence on behalf of KPMG and REC showed that the number of people placed into permanent job roles across the UK fell at only a marginal pace that was unchanged from February. This cooling in the rate of decline represents a marked contrast to the solid falls in permanent hiring seen for much of the past three years.

While there were reports that employers were generally cautious around taking on new permanent workers, there were also indications that some firms had lifted hiring freezes to fill vacancies in order to support growth plans.

There was also better news in terms of temporary staffing. Billings received from the employment of short-term/contract workers fell at a slower rate in March and one that was modest overall. Notably, the respective seasonally adjusted index has signalled a slight increase in billings in two of the past six months, with demand for more flexible staff often reported in some sectors amid ongoing uncertainty around the economic outlook.

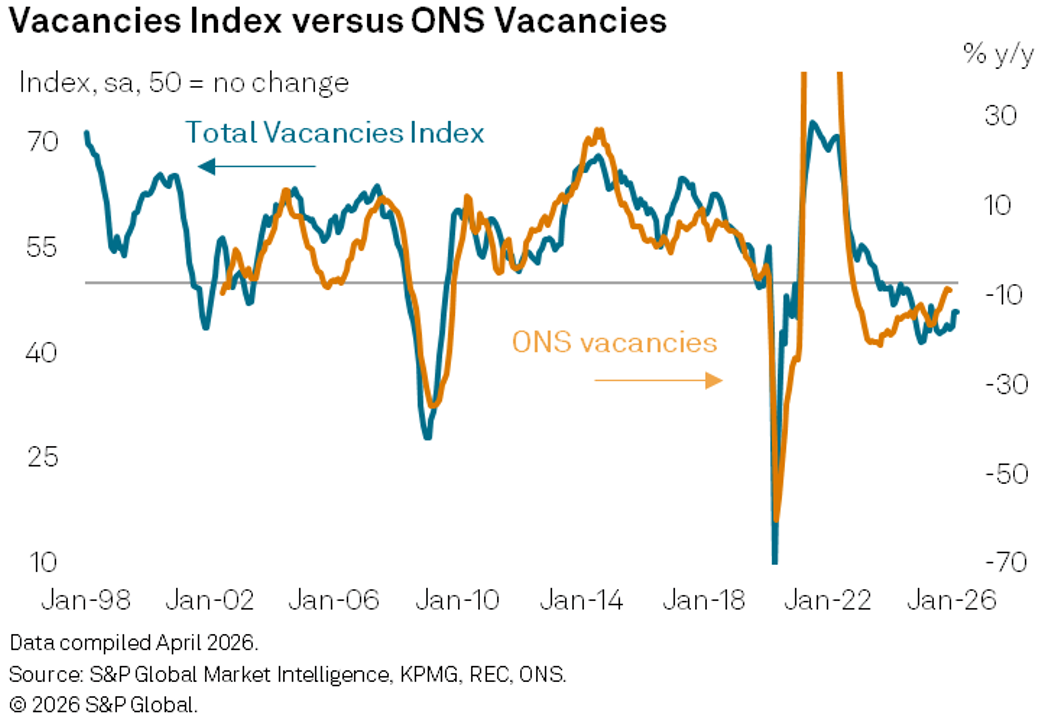

Downturn in vacancies eases but remains solid

Although hiring trends became more stable, overall demand for workers continued to fall solidly at the end of the first quarter. That said, the latest reductio in vacancies was the softest recorded since last May and weaker than the trend seen over 2025. Demand for both permanent and temporary staff fell at fractionally slower, but still marked, rates in March.

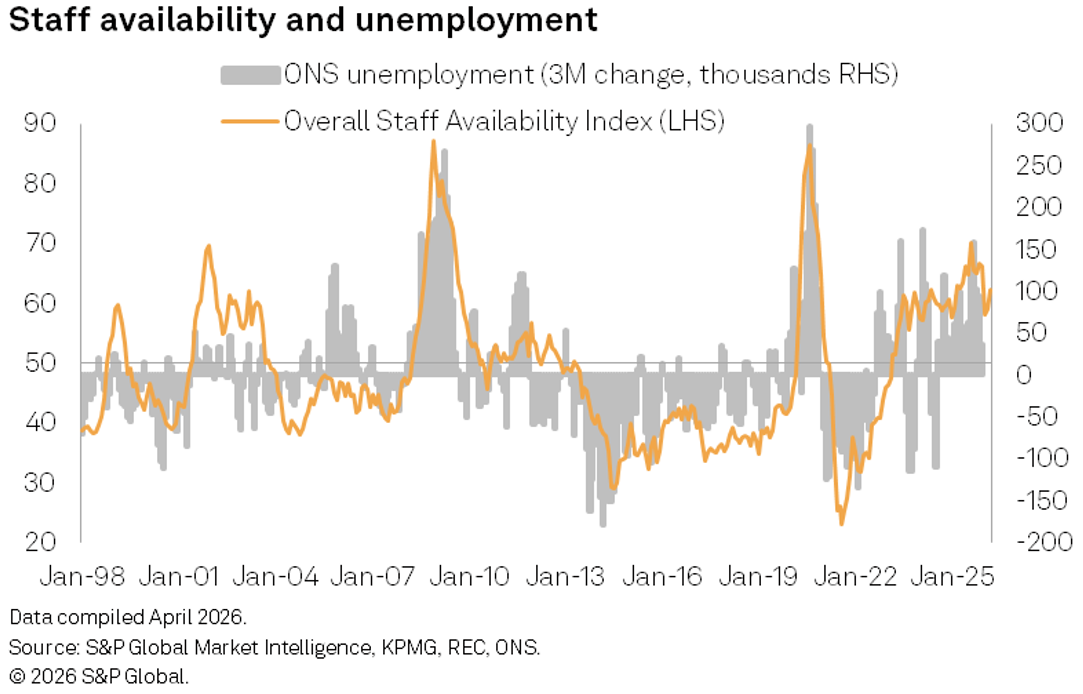

Sharper rise in candidate numbers amid reports of redundancies

There were once again widespread reports of redundancies in the latest survey period, as employers often looked to streamline operations and reduce costs where possible. Consequently, the overall availability of candidates increased at a rapid pace that was the quickest in three months. Furthermore, the current 37-month period of rising labour supply is the longest seen since the survey began in October 1997.

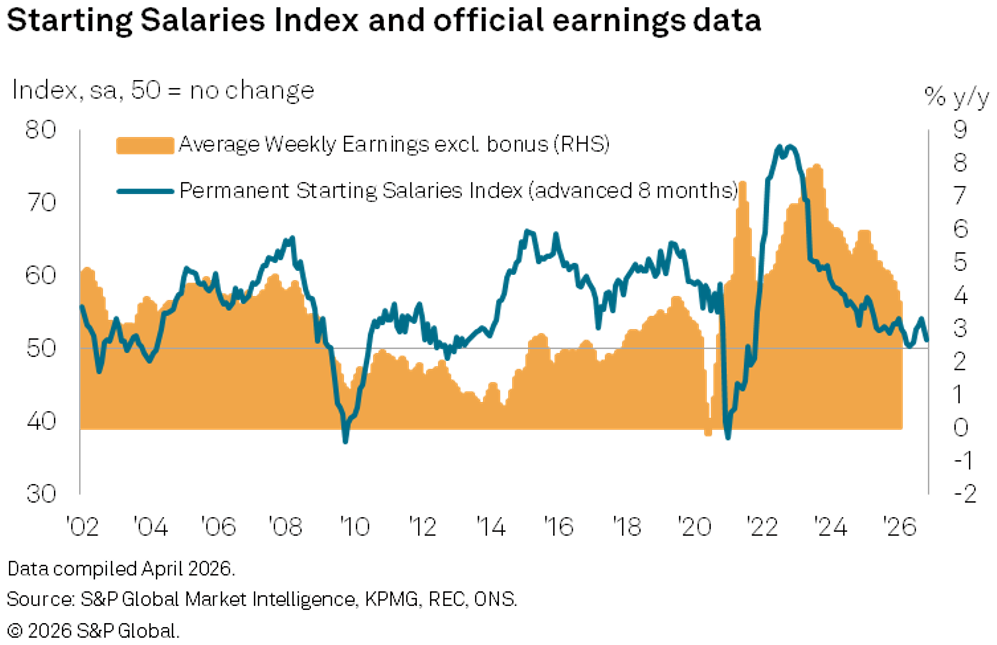

Pay growth set to cool further

The survey data also hint at a further slowing of pay growth. Recent earnings data published by the Office for National Statistics (ONS) showed that pay growth continued to ease across the UK into 2026. Notably, average earnings (excluding bonuses) increased by 3.8% on an annual basis in the three months to January, marking the slowest rates of expansion since the three months to November 2020.

This slowdown in the official rate of earnings growth was signalled in advance by the weaker pay trends recorded by the UK Report on Jobs Permanent Starting Salaries Index. Notably, the latest survey pointed to only a marginal increase in starting salaries. Temp wages have likewise risen only slightly in March. The softer pay trends coincide with signs of greater slack in the labour market, as demand for staff has weakened while the availability of candidates has risen sharply, but also marked increases in costs. Recruiters have often commented that cost pressures – which stemmed from a range of factors including day-to-day running costs such as energy and fuel, but also higher staffing costs via increases in the national minimum wage – continued to squeeze hiring budgets and pay offers.

While the Starting Salaries Index has remained above the post-pandemic low seen last October 2025, it continues to signal a further easing of official pay growth to approximately 3% in the coming months. This would mark the slowest rate of increase since the initial wave of the pandemic, but one that remains stronger than the pre-pandemic trend.

Access the latest PMI press release here.

© 2026, S&P Global. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

Read our latest PMI commentary here.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Theme

Location

Products & Offerings