Research — April 27, 2026

Alphabet earnings preview: Q1 2026

By Melissa Otto, CFA

CDS Swap Spreads increase

Source: Christopher Fenske, Primary Markets Group, S&P Global (April 24, 2026)

Alphabet earnings preview: What’s happening to margins?

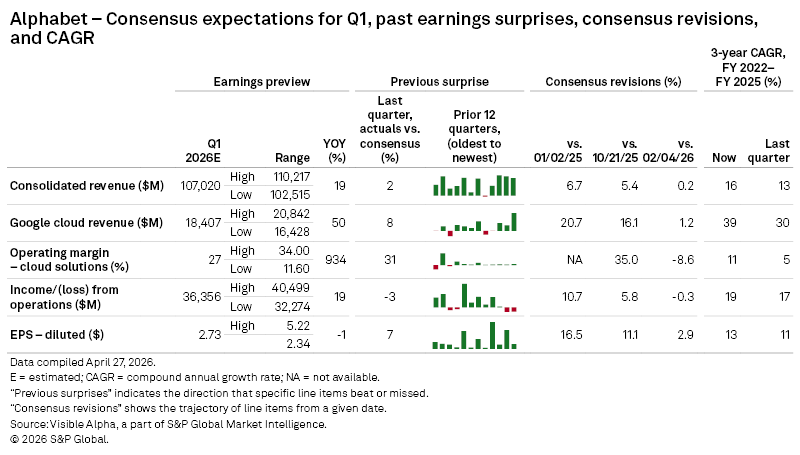

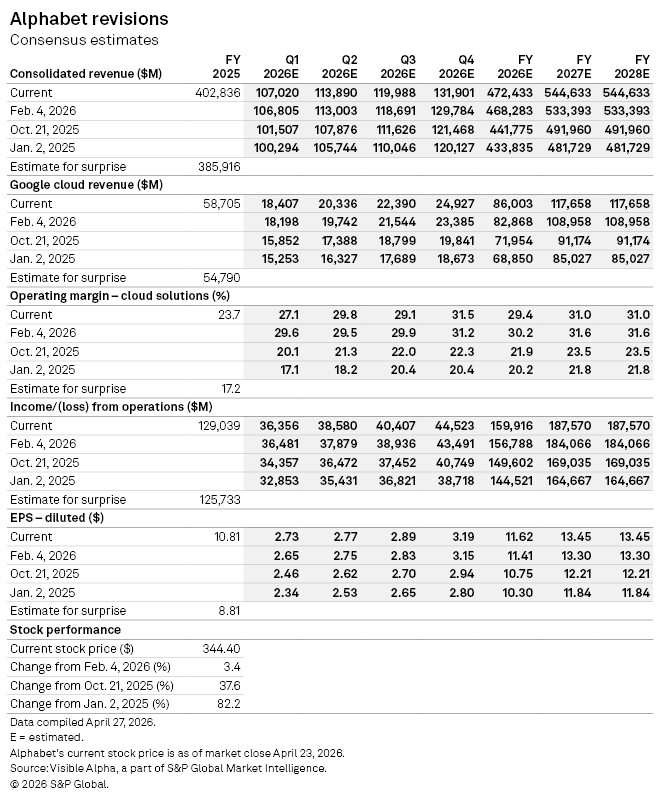

According to Visible Alpha consensus, Alphabet Inc.'s (NASDAQ: GOOG) total revenues expected for Q1 2026 have increased to $106.9 billion from $101.5 billion in the fall, driven by resilience in its ad business and potential strength in Google Cloud. In addition, the Q1 consensus expectations for operating income and EPS have also increased, due to a higher Cloud margin expectation. Since October 2025, the Google Cloud margin has expanded from 20% to 27%, driving consensus EPS expectations up from $2.46 to $2.73 for Q1. There are differing assumptions around costs, particularly in its Cloud business, leading the Google Cloud margin to range from 11.6% to 34%. It will be interesting to hear what Alphabet says about the outlook and where the Cloud margin is likely to settle.

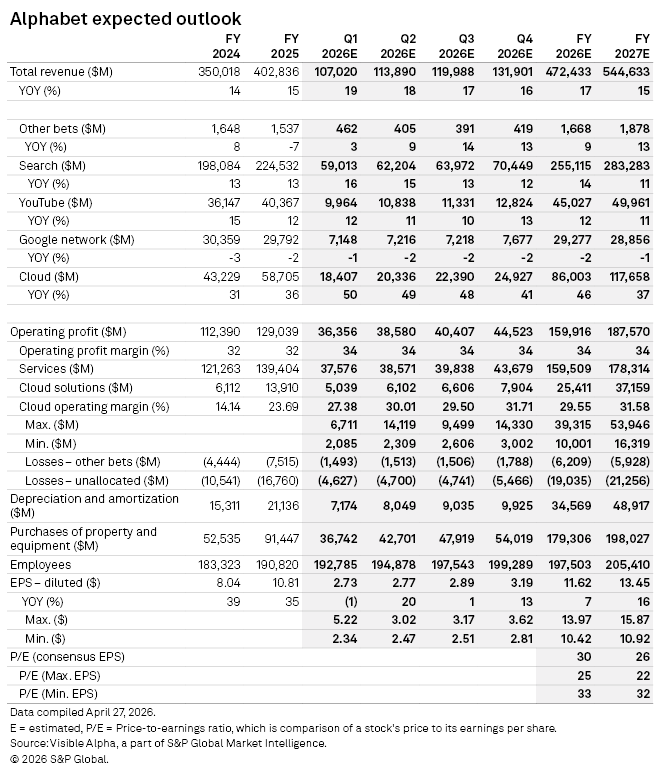

We are closely monitoring the trend of the Cloud business. The operating profit margin has been trending better. Looking ahead to Q2 2026, analysts now expect the Cloud business to generate a 29.8% operating profit margin, up 900 bps year over year. Longer term, analysts are also split in their views. For the Cloud business, Visible Alpha consensus expects the operating profit margin to hit 29.4% in FY 2026 but with a significant range of estimates. If the core Search and Ads business remains resilient, the performance of Alphabet stock is likely to be driven by the Cloud segment once again.

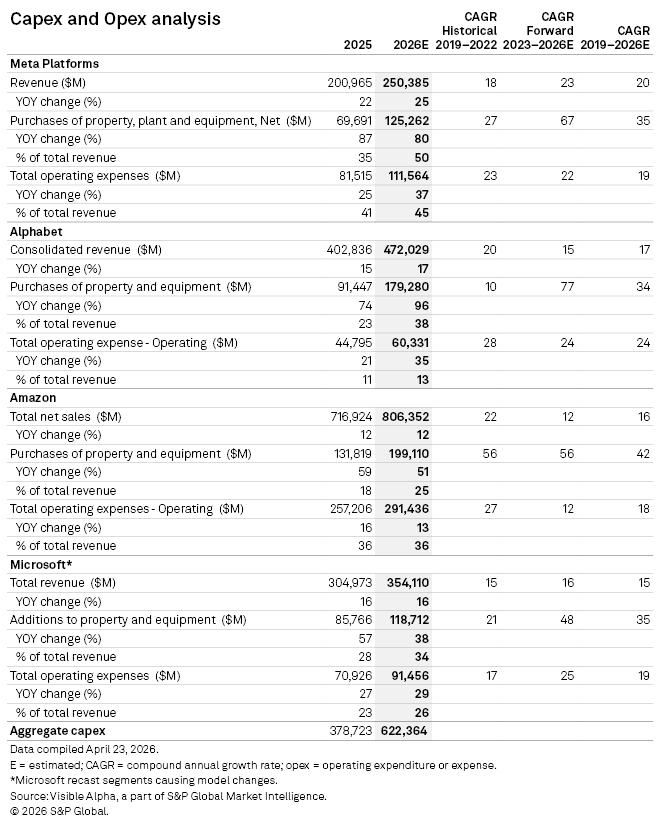

We are closely watching what the company will say about its investments into AI, as Alphabet’s FY 2026 CapEx numbers have continued to increase. According to consensus projections, CapEx estimates have surged over 5x from $32.3 billion in FY 2023 to $179.3 billion in FY 2026. While Alphabet’s overall debt remains healthy, it is worth noting that levels are increasing. Also, the market has been critical of the excessive use of cash without a clear ROIC.

Alphabet stock has traded up 35.4% since the October release. The consensus P/E for 2027 is 29x with a target price of $381. The stock has remained resilient, driven consistent growth in ads and by margin expansion in its Cloud business. Could the Q1 release provide more visibility into the trajectory of 2026 profitability and give shares a further boost?

Content Type

Products & Offerings