Research — March 13, 2026

Lithium price gains improve margins, prospects for unconventional supply

By Shunyu Yao

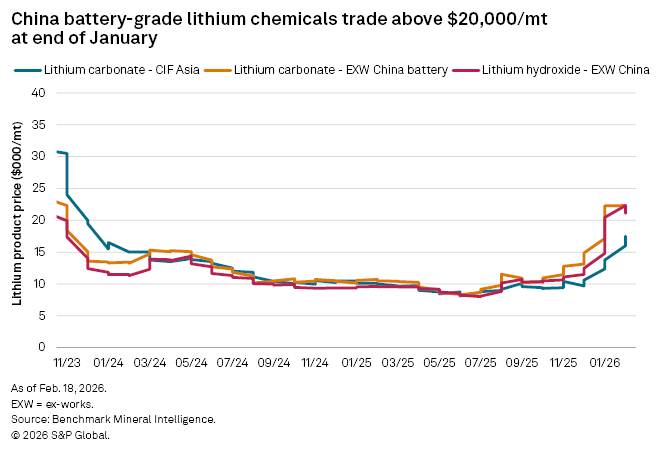

Lithium prices have begun to recover after hitting a five-year low in the summer of 2025, with the lithium carbonate CIF Asia price reaching $17,500 per metric ton on Feb. 18 — the highest level since January 2024. This rebound has increased margins for operating lithium miners and may open the door for shuttered operations. According to our analysis, however, current lithium prices may not be sufficient to incentivize unconventional extraction projects.

➤ Existing lithium mines are benefiting from rising prices, leading to improved margins.

➤ Halted or idled lithium assets are evaluating options of how to progress.

➤ An analysis of 54 technical studies indicates that unconventional extractions require higher incentive prices.

Operating mines see margins grow

The 2025 cash margin curve shows that 15.5% of global lithium production operated at a loss, the majority originating from hard rock mines. Looking back to the price lows of June 2025, when the lithium carbonate CIF Asia price was $8,100/mt, nearly half of production was unprofitable. As lithium concentrate requires further processing into lithium carbonate or hydroxide to meet market demand, marginal production is primarily from hard rock assets. In fact, all lithium assets that entered care and maintenance over the past two years due to price pressures were hard rock operations, including three properties in Australia: Finniss, Bald Hill and Mt Cattlin.

The rise in lithium prices has markedly improved margins, however. As of Feb. 4, the highest end of the cost curve fell below the CIF Asia benchmark for lithium carbonate. This indicates that if all existing mines manage to keep costs unchanged, they should be able to generate positive revenues, at least on a cash margin basis. If prices can be sustained, this profitability will allow miners to amass sufficient capital for future development plans, including capacity expansion, process upgrades or new projects. It is worth noting that expansion activities can also elevate costs, thereby introducing risk. For example, following the expansion at Salar de Atacama between 2021 and 2023 by Sociedad Química y Minera de Chile SA (SQM), costs doubled due to a slow ramp-up. Rising costs were only brought under control once the new capacity stabilized.

Assets undergoing maintenance seek to restart

Not only are operating assets benefiting from the rising prices, but mines under care and maintenance are also seeking opportunities to restart. Core Lithium Ltd. released a restart study in May 2025, saying Finniss will be repositioned as a low-cost asset with a 20-year life. Mineral Resources Ltd. is evaluating its options and prevailing market conditions for the potential restart of Bald Hill, which was placed into care and maintenance in November 2024. Although Mt. Cattlin has not yet stated any plan to reopen, a continued market shift will undoubtedly support a revival case. Prior to entering maintenance, these three mines incurred the highest costs among concentrate producers, rendering them sensitive to price downturns.

Restarting high-cost operations is challenging. The Altura mine in Western Australia ceased at the end of 2020 when the owner went into administration due to low prices. However, it was later merged into Pilbara Minerals Ltd.'s Pilgangoora mine and resumed production at the end of 2021, before entering another maintenance period in December 2024.

Projects that were previously delayed or went bankrupt also merit attention. Kemerton and Kwinana lithium refineries halted construction of their lithium hydroxide plants in July 2024 and January 2025, respectively, due to economic unviability. Lepidico Ltd. entered administration in December 2024 but its Karibib project in Namibia was acquired by ILC Critical Minerals Ltd. in October 2025. The current price provides an opportunity to reassess these projects, but a redevelopment decision will still depend on capital expenditure requirements, funding conditions and the ability to secure credible offtake in a market that remains cost-competitive.

A lithium pipeline study: Unconventional extractions will need higher incentive prices

To assess whether recent prices are sufficient to incentivize a future lithium pipeline, we analyzed 54 studies of projects that had at least reached the preliminary economic assessment stage. Many studies were launched between 2023–25 following the high prices in 2022–23, reflecting renewed optimism and a broader range of resource concepts. Unconventional lithium extraction — including soft rock, oilfields and geothermal resources — accounts for 40% of the production capacity covered by these studies.

To ensure comparability of pre-production capital across different years, we used 2025 as a baseline in this analysis and applied an 8% annual growth rate to each year prior to 2025 — a blunt and relatively aggressive assumption that reflects COVID-19 pandemic-induced global supply chain disruptions. The results showed that hard rock projects have the lowest initial capital intensity, essentially because they produce low-value-added concentrate products rather than refined chemicals. However, when products are considered at the chemical level — lithium carbonate and lithium hydroxide — the capital intensity of integrated hard rock refineries exceeds that of conventional brines. Whether using evaporation ponds or direct lithium extraction (DLE), brines have essentially the same capital intensity in this dataset. Unconventional extractions are shown to be more capital-intensive, indicating they require higher prices to stimulate project advancement.

In this analysis, we used lithium carbonate prices of $20,000, $30,000 and $40,000/mt, combined with average total cash cost for lithium concentrate and chemicals in 2025, to measure the payback period for each extraction route. We used five years as the payback cutoff, which is an ideal figure for the mining industry. The results indicate that the $20,000/mt price is insufficient to promote unconventional lithium mining, even if these projects skip the ramp-up stage and reach full capacity directly. At $20,000/mt, hard rock projects can recoup initial costs within five years, but their refining stage is a concern; high initial capital extends the payback cycle, and refining costs also need to be monitored. A report from IGO Ltd. states that its hard rock refinery's conversion fee (excluding raw materials) exceeded $10,000/mt in 2025. At $30,000/mt, the average payback period for soft rock projects can be shortened to five years. A price of $40,000/mt is required for incentivizing oil fields and geothermal projects. It is worth noting that if the expected payback period is shorter than five years, a higher incentive price is required.

Overall, brine represents the most promising production pathway in terms of incentive economics, particularly when paired with disciplined expansion schedules and well-managed operating costs. Furthermore, DLE offers a faster production cycle than regular pond extraction, which takes around 13–16 months, making the commercial utilization of DLE in brine operations highly anticipated.

Cost competition continues

Despite the improvement in market profitability, the current environment is not favorable for everyone. Unless a significant and unexpected surge in demand occurs, future demand growth can still be satisfied by low-cost assets, meaning that higher‑cost supply will remain vulnerable to price volatility. Projects already in production and those slated to come online will benefit from the price recovery, but they must also carefully reassess their plans from a cost perspective, as current prices are insufficient to incentivize all projects in the market.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.