ECONOMICS COMMENTARY — 24 Mar, 2026

Inflation spike and growth slump signalled as flash PMI tracks war impact in March

The war in the Middle East has hit the UK economy in March, stalling growth while driving inflation sharply higher.

Output growth across manufacturing and services has slowed to a crawl as companies blamed lost business directly on the events in the Middle East, whether through heightened risk aversion among customers, surging price pressures, higher interest rates, or via travel and supply chain disruptions.

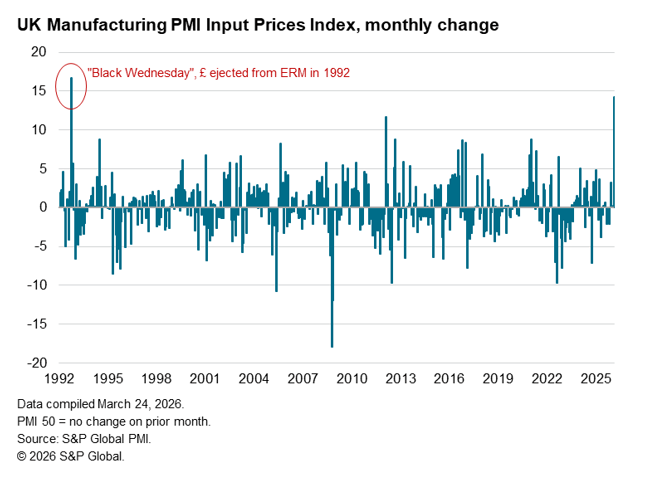

Inflationary pressures have surged higher on the back of rising energy prices and fractured supply chains. The acceleration in cost growth in the manufacturing sector was especially severe, being the sharpest since the depreciation of sterling following Black Wednesday in 1992.

The full impact on inflation and economic growth depends not just on the duration of the war but also the length of disruptions to energy markets and shipping, though March’s PMI numbers clearly underscore how downside growth risks and upside inflation risks have already materialised.

The Bank of England faces a challenging period where it will need to balance these growth and inflation risks when setting policy, seeking to dampen the potential for the inflation spike to become more engrained while ensuring a hawkish interest rate outlook does not exacerbate downturn risks.

Business growth hit by war outbreak

UK businesses reported a marked slowing of output growth in March as demand for goods and services fell for the first time since last November following the outbreak of war in the Middle East.

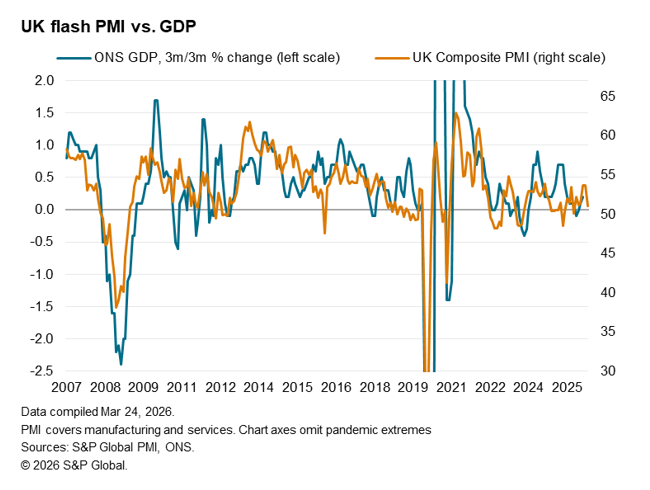

The PMI headline Composite PMI Output Index has slumped from 53.7 in February to a six-month low of 51.0 in March, according to the preliminary ‘flash’ reading. The latest reading is broadly consistent with GDP growth stalling in March, albeit with a modest 0.2% quarterly rise indicated for the first quarter as a whole.

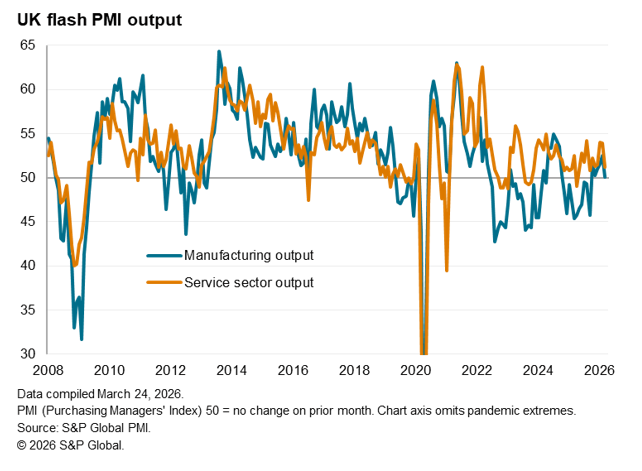

Manufacturing output grew only marginally, posting its worst performance since production growth resumed five months ago, while service sector business activity rose at the slowest rate since last September.

War impact

The March flash PMI data, collected between 12-20 March, represent the first snapshot of business conditions after the outbreak of war in the Middle East on 28 February. Approximately one-third of all companies reporting a reduction in orders attributed the decline directly to the events in the Middle East, albeit often through varying channels.

In the service sector, reduced travel and tourism bookings were reported due to war-related travel concerns, while increased prices, higher interest rates and risk aversion were also cited as dampening demand, especially in financial services.

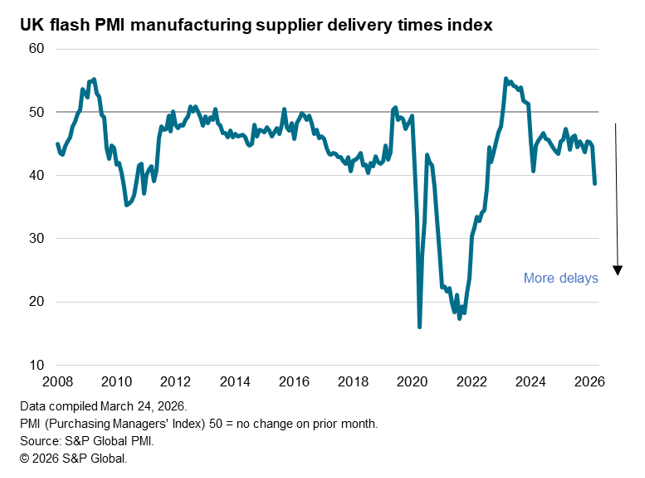

Manufacturers likewise reported a broad-based demand hit from the war, with customers often postponing or cancelling orders, though factories also cited the war’s disruption to supply chains. Supplier delivery times lengthened in March to the greatest extent since July 2022, when supply chains were affected by the pandemic. Half of all companies reporting longer lead times attributed the deterioration to the events in the Middle East to some extent, often citing the need to divert shipping due to the conflict. March’s supply delays are by no means as severe as seen during the height of the COVID-19 disruptions, though are more pronounced than seen during the escalation of Houthi Red Sea attacks in 2024.

Cost pressures highest for over three years

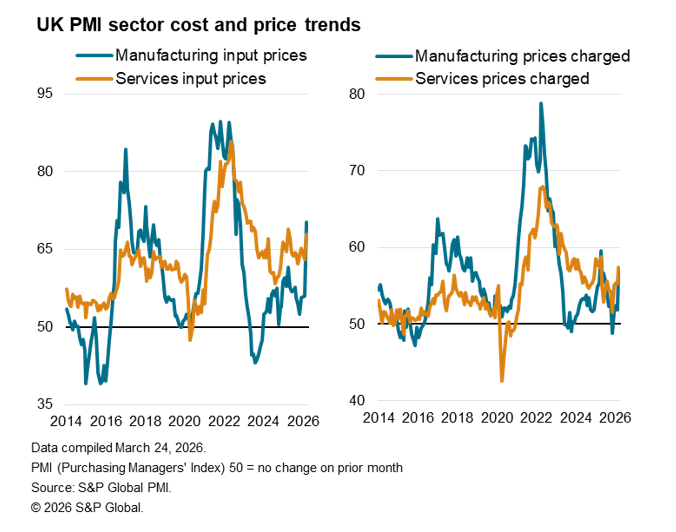

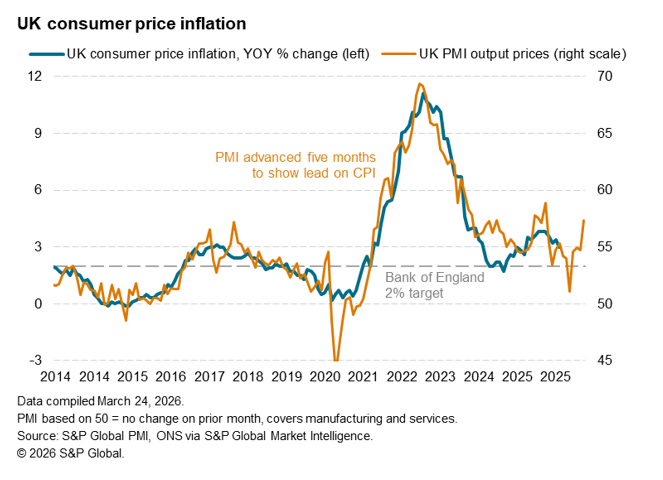

The biggest impact of the war, however, was on prices. Higher energy and fuel prices, the latter driving up freight and shipping costs, exacerbated existing upward price pressures – notably from rising wage costs – to push input cost inflation up to its highest since February 2023.

Manufacturers reported an especially steep jump in costs, the rate of increase hitting the steepest since October 2022. The acceleration in manufacturing input cost inflation during the month was the greatest recorded since sterling was ejected from the European Exchange Rate Mechanism in 1992. Service sector input cost inflation also accelerated, hitting an 11-month high, led by a surge in cost inflation among travel and transport companies.

Higher costs fed through to increased selling prices, with the rate of inflation across goods and services climbing to the highest since April of last year. At its March level, the PMI’s Output Prices Index is indicative of consumer price inflation accelerating to around 4.5%.

Confidence slips amid war worries

A further toll on the economy from the war appeared via a sharp deterioration in business optimism. Companies’ expectations about the outlook for the year ahead sank to the lowest since last June, when confidence had been hit by US tariff worries, dropping well below the survey’s long-run average. The deterioration marks a sharp reversal of the recovery of confidence seen at the start of the year, when business expectations had revived to a 16-month high.

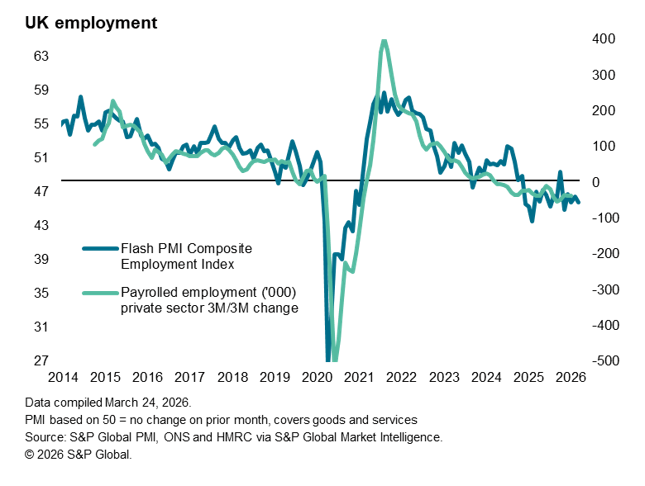

Job losses accelerate

The loss of confidence led to further job losses in March, with employment dropping across manufacturing and services at a slightly increased rate. Jobs have been cut continually since October 2024, according to the PMI survey panel, focused primarily on the need to offset higher staffing costs introduced in the past two autumn Budgets.

Read the press release here.

© 2026, S&P Global. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

Read our latest PMI commentary here.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Theme

Location

Products & Offerings