Research — March 18, 2026

Higher gold prices are boosting revenue expectations but squeezing margins

By Karan Sadh

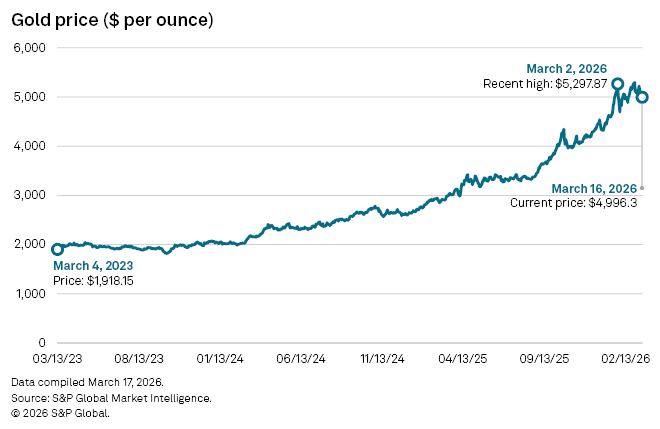

Gold producers are enjoying a favorable pricing backdrop, with bullion remaining elevated after surging on geopolitical risk and haven demand. That windfall is lifting topline figures sharply across the sector, yet the same high price environment is increasingly a source of margin pressure as cost inputs, royalties and taxes ratchet up.

Gold prices pushed past January highs in early March as tensions surrounding the Iran conflict unsettled markets, reinforcing bullion’s status as a haven asset. Although prices have since eased, they remain still historically high.

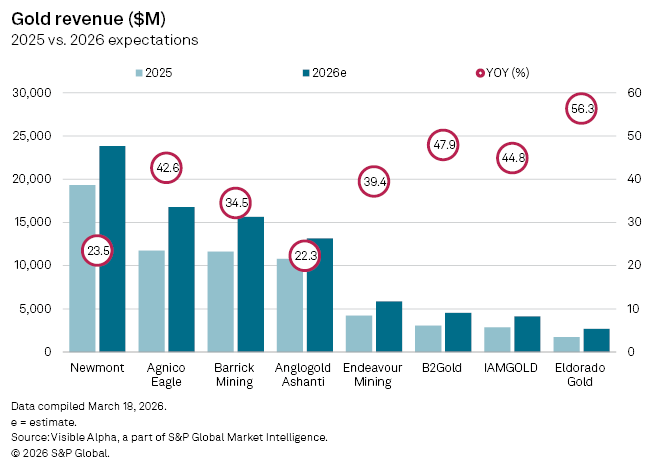

This has translated into significant revenue growth expectations for producers, Visible Alpha consensus show.

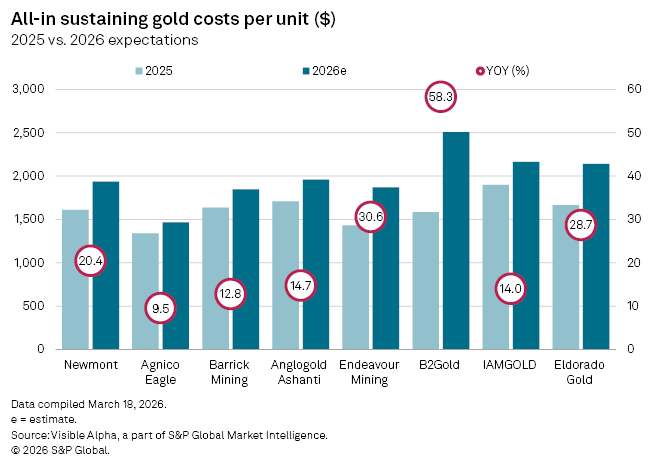

At the same time, producers are contending with rising all-in sustaining costs (AISC), a comprehensive industry measure of cash costs inclusive of sustaining capital, royalties and other site costs. Inflationary pressures across labor, energy, and materials combined with royalty regimes that scale with the gold price are expected to push AISC materially higher for many miners.

Visible Alpha consensus forecasts point to pronounced cost escalation in 2026. Estimates suggest B2Gold’s (TSE: BTO) AISC could climb about 58% year-on-year to roughly $2,507 per ounce, driven by production transitions, deferred stripping, and an expanded royalty bill.

Endeavour Mining (TSE: EDV) and Eldorado Gold (TSE: ELD) are also expected to see AISC rise about 31% and 29%, respectively, with Newmont (NYSE: NEM) facing a projected 20% increase.

Other large producers such as Agnico Eagle Mines (TSE: AEM), Barrick Mining (TSE: ABX) and AngloGold Ashanti (NYSE: AU) are anticipated to report more moderate 10–15% increases.

Royalty burdens are an increasingly salient factor for cost inflation. Ghana, Africa’s largest gold exporter, has cancelled long-term mining deals and raised royalty rates to align with elevated gold prices, effective March 2026. In Turkey, legal changes effective from July last year widened sliding‑scale royalty price bands, forcing miners to pay higher state levies at current bullion prices and materially lifting unit costs.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Products & Offerings

Segment