Research — March 24, 2026

Geopolitical volatility driving rapid shifts in 2026 oil & gas forecasts

By Karan Sadh and Shalabh Gupta

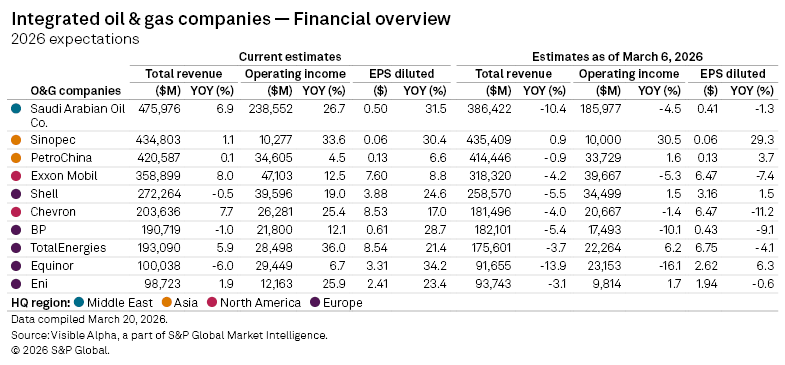

Analysts have lifted 2026 expectations for the world’s largest integrated oil and gas companies in recent weeks, as geopolitical tensions in the Middle East inject fresh volatility into energy markets and reshape near-term earnings prospects.

Crude prices have rallied sharply amid escalating tensions involving the Middle East, with markets pricing in a rising risk of supply disruption from a region that underpins a significant share of global oil flows. The prospect of interruptions to key transit routes, particularly the Strait of Hormuz, has pushed a geopolitical risk premium back into prices, reversing some of the weakness seen earlier this year.

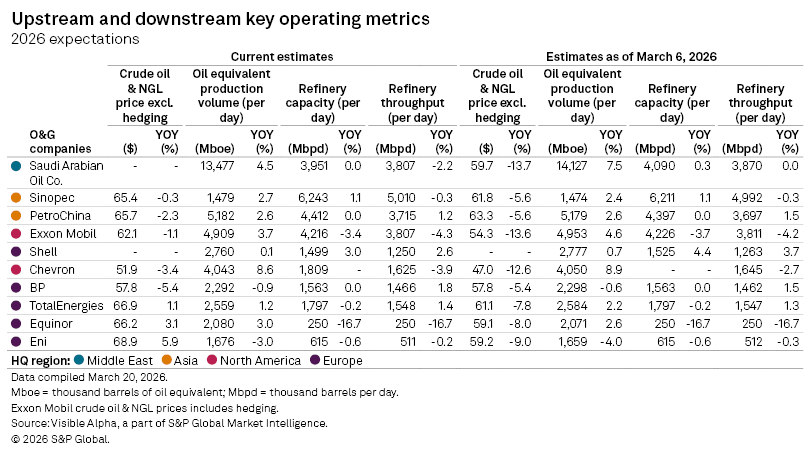

This shift is clearly reflected in analyst forecasts. Consensus assumptions for 2026 crude oil and natural gas liquids prices have been revised higher compared with early March estimates, as stronger near-term price realizations feed into outlooks. However, the more notable change has been in profitability, where upgrades have been more pronounced.

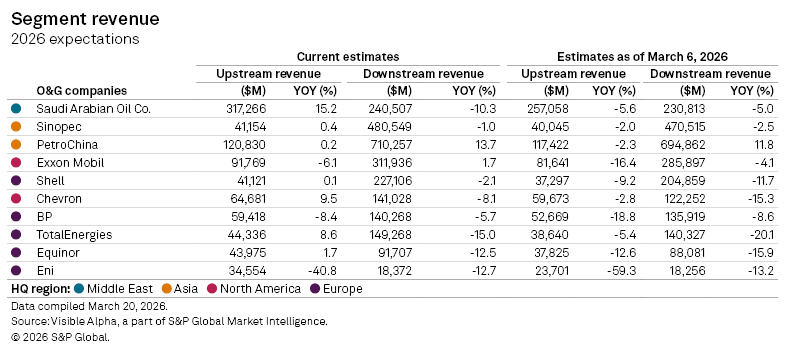

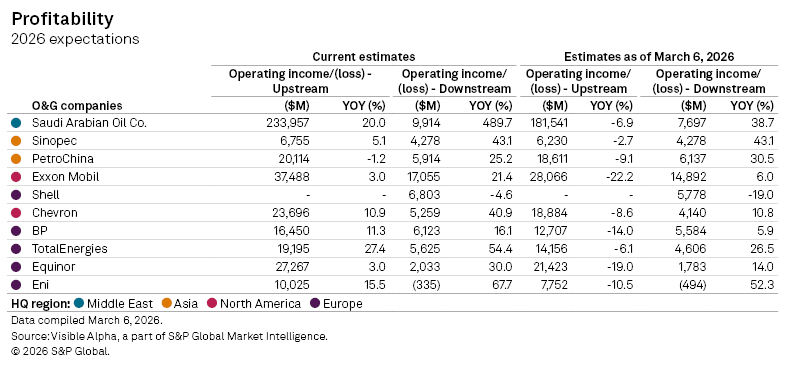

Across the sector, analysts have raised forecasts for operating income, supported by stronger downstream performance and improved margin expectations. Refining and marketing businesses are expected to benefit from higher product prices and widening crack spreads, as refined fuel markets tighten more quickly than crude supply.

Upstream earnings expectations have also moved higher, reflecting improved near-term realizations and firmer pricing assumptions. The combination of stronger upstream pricing and resilient downstream margins is driving a broad-based uplift in profitability forecasts across the majors.

Notably, these upgrades are not being driven by volume growth. Production and refining capacity assumptions have remained broadly stable, and in some cases edged lower, indicating that the improved outlook is largely margin-driven rather than a function of higher output.

Looking ahead, the market will continue to be shaped by both geopolitical developments and underlying supply-demand dynamics. As seen in the recent analyst revisions, it is worth noting that consensus expectations are changing rapidly in response to evolving price signals and regional risks.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Products & Offerings

Segment