Research — February 17, 2026

Mattel craters, while Hasbro's digital gaming division delivers

By Cristalina Pinto

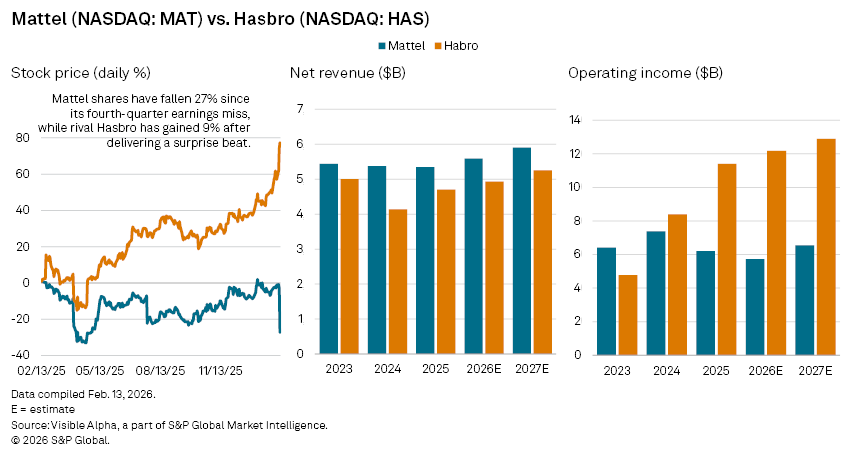

Mattel Inc. (NASDAQ: MAT) reported fourth-quarter 2025 results on Tuesday, February 10, that fell short of Visible Alpha consensus expectations. Q4 net revenue of $1.77 billion, was 4.1% below preQ expectations, while operating profit of $160 million came in 33.7% below estimates. Shares have since slid nearly 27%.

Hasbro Inc. (NASDAQ: HAS), reporting the same day, delivered the opposite surprise. Revenue of $1.44 billion beat Visible Alpha preQ forecasts by 14.4%, and operating profit of $314 million topped expectations by 44%. Its stock has risen by about 9% since the results. Mattel remains larger by sales, although profitability tells a different story.

Both companies faced a challenging seasonal backdrop, with tariff-related cost pressures and intense promotional activity. Hasbro, however, found a key growth engine in its Wizards & Digital Gaming division, home to Magic: The Gathering and digital/mobile game Monopoly Go, where revenue surged 86% year-on-year, helping offset weakness in traditional toy categories.

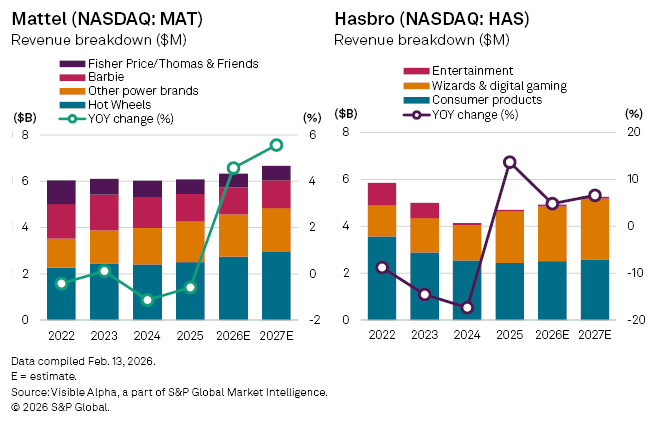

Visible Alpha consensus forecasts point to a revenue rebound for Mattel in 2026, with sales expected to rise 4.6% to $5.6 billion. Management is betting on a shift beyond toys, moving deeper into entertainment and mobile gaming through the planned full acquisition of Mattel163, a developer of digital game titles based on the group’s flagship brands. The company’s Power Brands segment benefiting from these investments is expected to see 2026 revenue climb 10% to $2.7 billion.

Still, heavier spending on digital games, technology, and marketing is expected to weigh on margins, with operating profit expected to fall 8% in 2026 to $573 million.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Theme

Products & Offerings

Segment