Research — February 4, 2026

Gold miners to reap price windfall as bullion cools from record highs

By Sonam Sidana

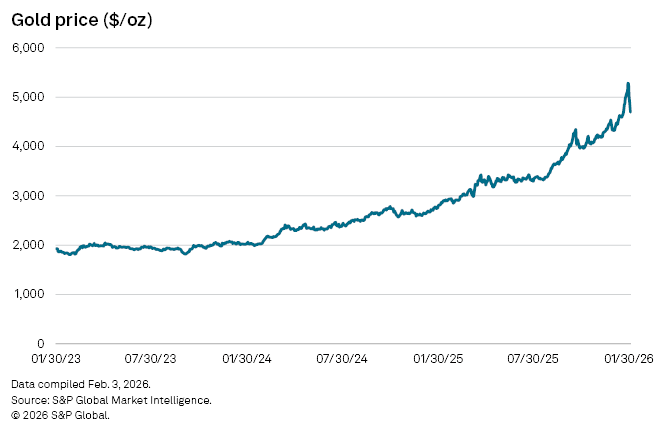

Gold and silver prices have retreated in recent sessions after a sharp reversal from a rally that carried prices of the precious metal to record highs. Last year, gold surged through successive thresholds, trading above $3,000 and then $4,000 an ounce, as investors sought protection from geopolitical risk, persistent inflation, and shifting expectations for interest rates. Prices notched fresh records again in January surpassing $5,000 an ounce as safe-haven demand intensified.

While prices have cooled off over the last few days, the pullback has done little to dent the broader picture. Prices still remain significantly elevated compared to those seen at the same point last year.

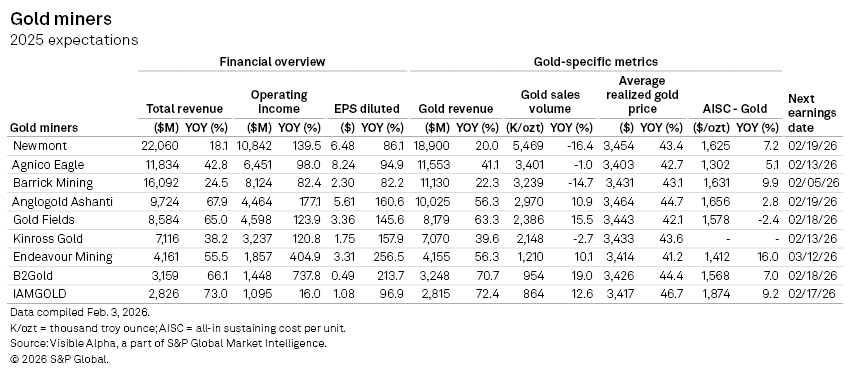

Among some of the largest gold producers tracked by Visible Alpha; Newmont (NYSE: NEM), Agnico Eagle Mines (TSE: AEM), Barrick Mining (TSE: ABX), AngloGold Ashanti (NYSE: AU), Gold Fields (JSE: GFI), Endeavour Mining (LSE: EDV), B2Gold (TSE: BTO), and Iamgold (TSE: IMG), shares have rallied strongly over the past 12 months, reflecting both the step-change in realized prices and expectations of fatter margins.

Consensus forecasts suggest the price strength is also expected to translate to strong earnings as the leading gold miners gear to report fourth-quarter fiscal 2025 results, starting with Barrick Mining on Thursday, February 5.

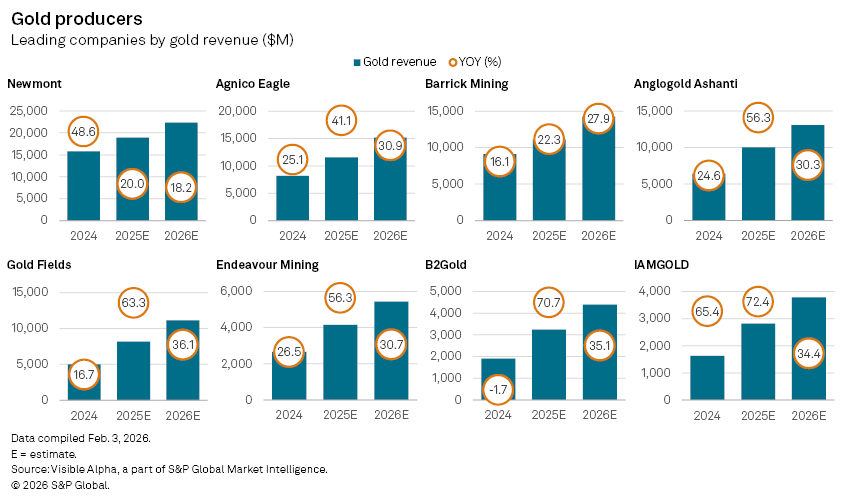

Newmont, the world’s largest gold producer by market capitalization, is expected to see gold revenues lift by 20% in 2025 to $18.9 billion, according to Visible Alpha consensus.

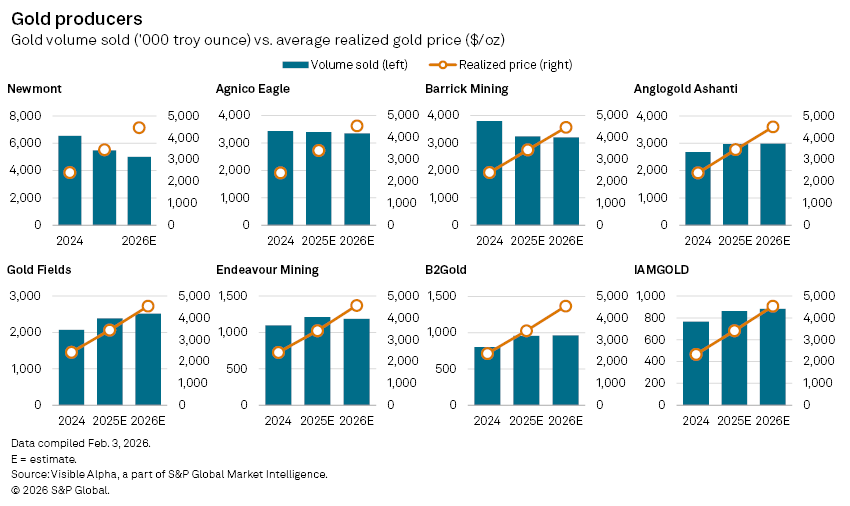

Gold accounts for about 86% of the group’s total revenue. The pace of growth is slower than the high double-digit expansion seen in 2024, a year that benefited from the integration of Newcrest Mining assets alongside rising prices. In 2025, topline growth is expected to be almost entirely price-driven, as gold sales volumes are forecast to fall 16% to about 5.5 million ounces following the completion of Newmont’s non-core asset divestment program.

A similar pattern is evident across peers. Agnico Eagle, which derives roughly 98% of its revenue from gold, is forecast to see gold revenue jump 41.1% to $11.6 billion in 2025, despite broadly flat sales volume. Barrick Mining, where gold contributes about 69% of revenue, is expected to post a 22.3% increase in gold revenues to $11.1 billion, even as volumes decline by an estimated 15% to 3.2 million ounces.

Smaller, more gold-pure producers show even sharper operating leverage to prices. B2Gold and IAMGOLD, which generate virtually all of their revenue from gold, are projected to record revenue increases of 70.7% and 72.4% respectively, taking annual gold revenues to about $3.2 billion and $2.8 billion in 2025.

Across the sector, analysts point to realized prices rather than output growth as the dominant driver of earnings in 2025. Forecast gold realized prices are sharply higher year-on-year, reflecting last year’s powerful rally, while sales volumes for the top three miners are flat or declining.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Theme

Products & Offerings

Segment