Research — February 4, 2026

Copper rally to squeeze margins for India’s Crompton Greaves in 2026

By Yash Gupta

Copper, a critical raw material for the consumer durables industry has seen prices rally over the last year, barring the recent pullback. With global copper prices on a high, appliance makers are finding it harder to protect margins without risking demand.

Indian household appliance maker, Crompton Greaves Consumer Electricals Ltd. (NSE: CROMPTON), flagged this pressure in its recent second-quarter earnings, pointing to commodity inflation and the risk that higher input costs could translate into elevated inventory levels as companies stock up ahead of further price increases.

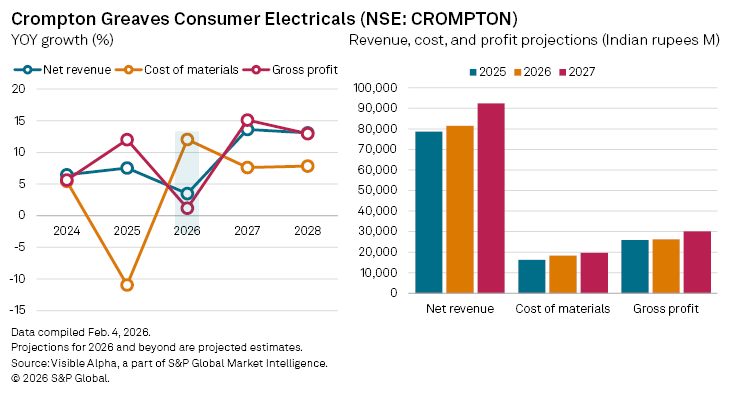

According to Visible Alpha consensus, these pressures are expected to weigh on the company’s topline in 2026. Crompton’s cost of materials consumed is forecast to rise 12% year-on-year in 2026 to INR18.2 billion, reflecting higher commodity prices and limited near-term relief on inputs. At the same time, revenue momentum is expected to soften. Net revenue growth is projected to slow to 3.5% in 2026, down from 7.5% last year, as price hikes become harder to pass through in a competitive consumer market.

The squeeze is most visible at the gross profit line. Analysts expect gross profit growth to decelerate sharply to 1.2% in 2026, from 12% in 2025, impacted by rising copper and other commodity costs. EBIT margins in Crompton’s consumer electricals segment are forecast to ease to 12.76%, from 13.92% last year.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Products & Offerings