Research — February 20, 2026

BD revenue to fall post spin-off as margins edge higher; Waters sales to jump

By Rahul Mamedala

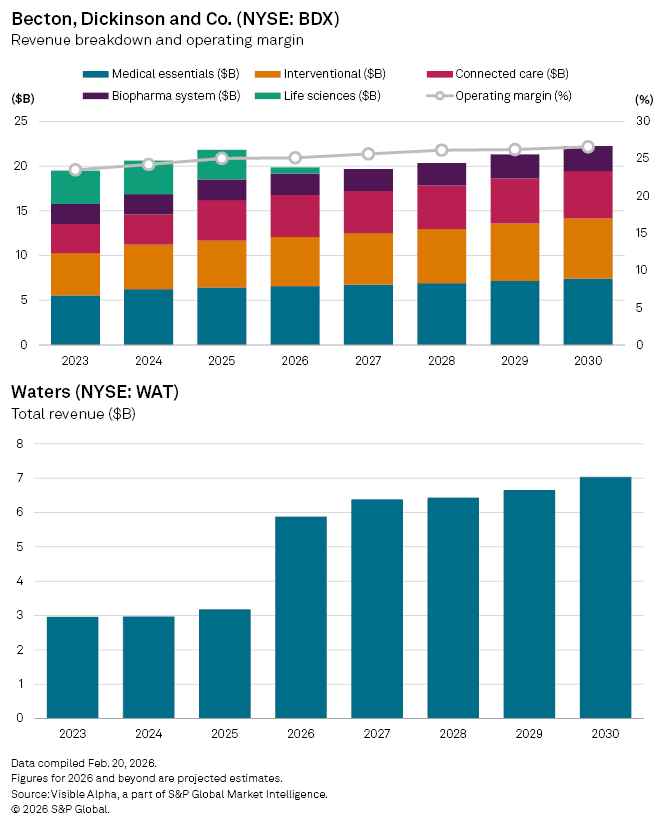

Medical device maker, Becton Dickinson (NYSE: BDX) has completed the spin-off of its Biosciences & Diagnostic Solutions unit (Life Sciences business) and merged the separated entity with Waters Corp. (NYSE: WAT).

In recent years, BD has divested three non-core businesses and executed more than 20 tuck-in acquisitions to sharpen its focus on higher-growth, higher-margin medical technology segments.

The Life Sciences division was a standout performer during the pandemic. In 2021, demand for COVID-19 diagnostic testing drove a sharp spike in sales, temporarily inflating the segment’s revenue base. As testing volumes normalized, those revenues unwound, creating tough year-on-year comparisons and a visible drag on reported growth in subsequent periods.

With the divesture now complete, analysts expect BD’s fiscal 2026 revenues to fall 12% year-on-year to $19.2 billion, largely reflecting the removal of the Life Sciences business from consolidated accounts rather than underlying weakness in its continuing operations.

Profitability, however, is forecast to edge higher. According to Visible Alpha consensus estimates, operating margins are projected to rise to 25.11% in 2026, from 25% last year, as the group becomes more concentrated in MedTech categories.

For Waters, the deal is transformative. The analytical instruments specialist reported revenue of $3.2 billion in 2025. Consensus forecasts point to an approximately 85% year-on-year jump to $5.9 billion in 2026, driven by the addition of BD’s Life Sciences assets. The combination materially expands Waters’ scale and broadens its footprint in diagnostics and life sciences tools, strengthening its position in laboratories and biopharma research settings.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Products & Offerings

Segment