09 Jul, 2026

Regulatory relief spurs de novo pickup, but hurdles remain

By Lauren Seay and Xylex Mangulabnan

Traditional community bank de novo activity is picking up amid federal and state efforts to simplify the startup process, but some hurdles still remain.

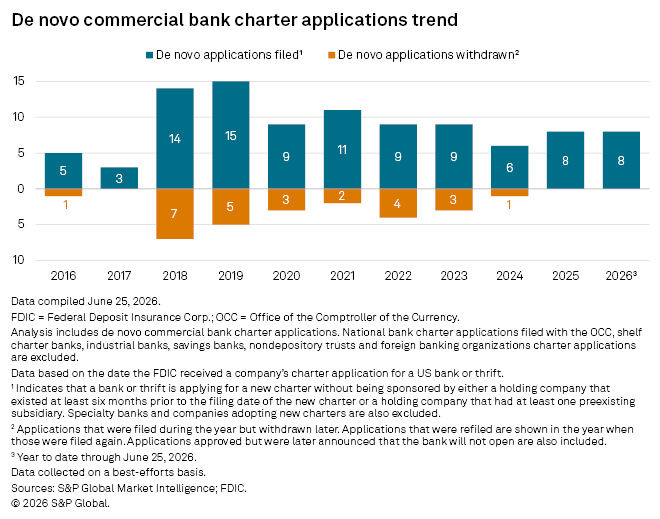

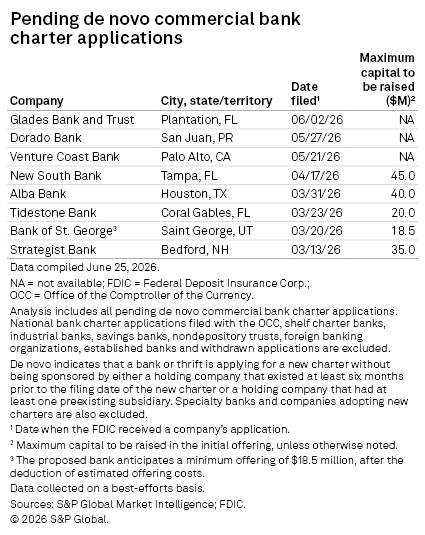

Along with national and trust bank charter applications, traditional community bank de novo applications are on the rise. Eight groups hoping to open a traditional community bank have filed for deposit insurance just halfway through 2026, putting the year on track to have the most applications

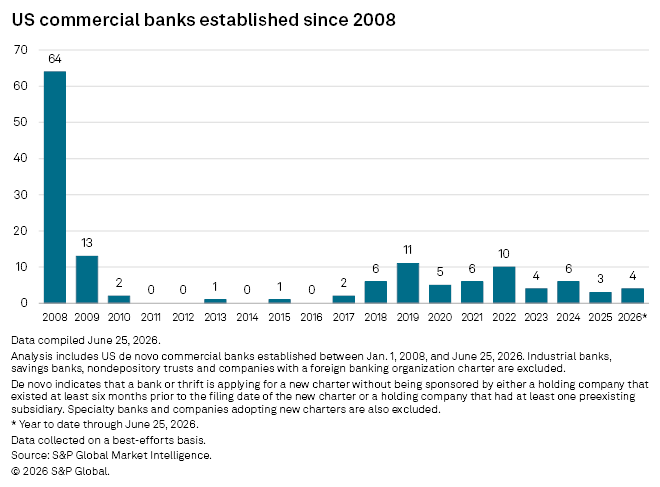

As application activity rises, community banks are also opening at a faster pace, with four established so far this year, already surpassing three openings in 2025.

With six approved de novo applications awaiting establishment, 2026 is rivaling 2019 and 2022 for the most community bank openings since 2009. The uptick comes as Federal Deposit Insurance Corp. Chairman Travis Hill has signaled an appetite to rebuild a de novo pipeline and encouraged the agency to be more flexible.

De novo relief efforts

High capital requirements are often cited among the biggest deterrents to starting a new bank. Prior to the financial crisis, new banks could be formed with as little as $10 million, but that minimum has doubled, with regulators typically requiring at least $20 million for most new banks, industry advisers said.

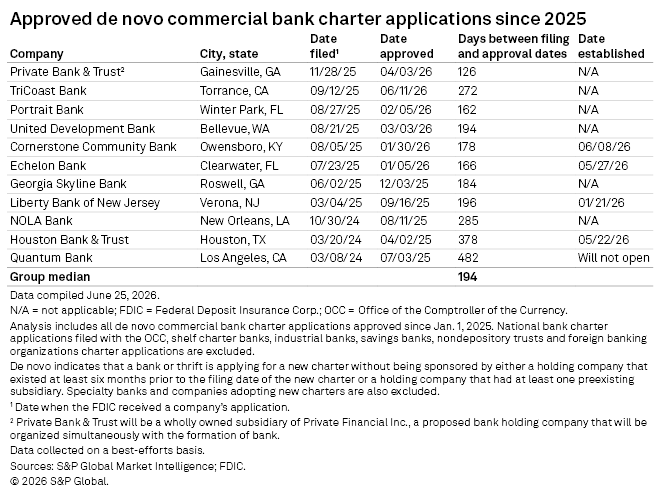

Since Trump-appointed regulators took their place at the start of 2025, two banks have secured FDIC deposit insurance approval with capital below $20 million: Washington-based United Development Bank at $15 million and Georgia-based Private Bank & Trust at $19 million.

Prior to that, only one bank was approved with required capital below $20 million in all of 2023 and 2024.

The highest community bank capital requirement the FDIC has handed out since 2025 was $40 million for Liberty Bank of New Jersey, compared to a high of $50 million in 2024 for New York-based Greater Gotham Bank and $96 million for Puerto Rico-based Nave Bank in 2023.

"For a long, long time, $20 million was about as low as they would go. ... There's been a little bit of a psychological shift where $20 million is not the bar," Paul Davis, Bank Slate founder and lead consultant, said in an interview. "The regulators seem to be approving more with reasonable capital thresholds."

Further capital relief could come from the final housing bill currently waiting to be signed by the president. The bill allows federal regulators to adopt a two-year phase-in program for de novos to gradually comply with federal capital requirements. It also allows new banks to request a deviation from their initial approved business plan during that two-year period.

The bill also aims to address the complex application process by instructing the regulatory agencies to streamline the de novo application procedure and improve communication with applicants by designating caseworkers who meet with organizers to give a tutorial of the application process and serve as a primary point of contact.

The bill also directs regulators to set up a de novo mentor program in which recently approved de novo organizers volunteer to mentor de novo hopefuls.

|

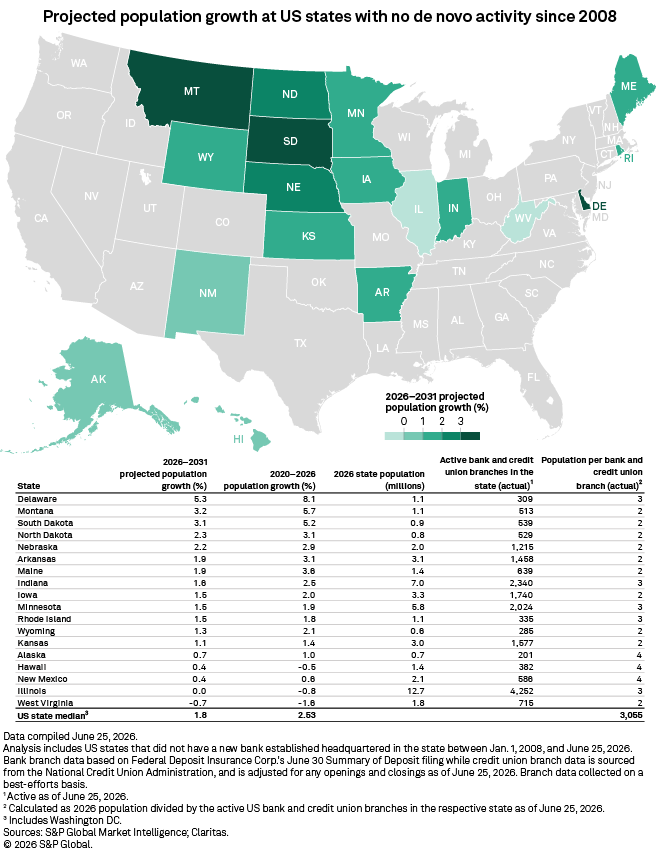

States step in

Florida has dominated de novo activity with 22 established, conditionally approved or pending applications since 2016. In the past year, five Florida-based community bank hopefuls have applied for deposit insurance. Among those, two have received approval and three are pending.

Other states have seen little to no activity since 2008, including 18 with none. Some states are taking things into their own hands to spur de novos.

Oregon, which has not had a new bank since 2008 and has only 12 banks headquartered in the state, recently passed a law that will exempt state-chartered de novos from up to $1 million in taxes for the first three years of operations.

The law was inspired by a similar law in Ohio that went into effect in 2021, Oregon Bankers Association President and CEO Scott Bruun said in an interview with S&P Global Market Intelligence. Since then, six new banks have opened in Ohio, including two national banks chartered with the Office of the Comptroller of the Currency.

However, the tax law's practical use has been limited.

Fortuna Bank, which opened in 2024, has yet to take advantage of the tax relief as it works toward profitability, founder, President and CEO Ilaria Rawlins told Market Intelligence. Fortuna Bank has posted net losses in the past six quarters since it opened. Typically, de novos take several years to post a profit.

The tax relief was also not a major factor in organizers' decision to form Fortuna Bank, Rawlins said.

Bruun is hopeful Oregon's unique tax structure and high number of credit unions will make the law more enticing. Oregon is one of five states without a sales tax, meaning it relies more on income and business taxes than other states. That dynamic widens the competitive gap between banks and credit unions, which are tax-exempt, in the state, Bruun said. There are 47 credit unions headquartered in Oregon, according to Market Intelligence data.

"If you're an investor or a banker that's finding investors that has a notion to start a de novo bank, you're not worried about competing against Wells Fargo & Co. or JPMorgan Chase & Co.," Bruun said. "But you can't go anywhere in Oregon without there being four, five or six credit unions all around you, and that's who you're coming out of the ground competing with. You just can't do it. And so that's how we ultimately got to 'We got to do some sort of tax credit, tax incentive to get people going here.'"

Still, Bruun acknowledged that there are still many hurdles to de novo formation, such as high capital requirements and Oregon's lack of growth compared to other states, he said. Oregon's population is expected to remain steady between 2026 and 2031, but its median household income is projected to grow 12.8% during that period, according to Claritas Pop-Facts data.

"A tax credit is no magic bullet. It's no panacea," he said. "I don't guarantee that we're going to have six new banks in the next six years [like Ohio]. ... But I do guarantee that conversations are going to happen in Oregon that weren't happening prior."

Bruun said he has since heard from other state banking association leaders hoping to implement a similar law, including Oregon's neighbor, Washington.

Remaining hurdles

Despite the relief efforts going on at both the federal and state levels, hurdles remain. Capital requirements are still a headwind, but the industry is hopeful that the recent approvals showing flexibility will stick.

"Capital requirements have to be on a case-by-case basis," Bruun said. "The up front capital to start a bank in Portland should be different than the up front capital to start a bank in some rural part of the state."

Ohio-based Fortuna was approved to open once it raised $20 million in capital.

"While capital requirements are a significant barrier to entry, I believe strong capitalization is critical for a de novo bank's success," Rawlins said. "At Fortuna, we addressed the challenge by lowering the minimum investment amount, which enabled us to attract a broader base of shareholders who are invested in both the bank's mission and its long-term success." Fortuna is a women-owned bank focused on serving women-owned and -managed businesses.

The FDIC's management expectations are also a hurdle, advisers said. While it can be easier to find a CEO to lead the bank, particularly as a recent wave of M&A frees up some executives, Davis said, putting together a multi-person board that meets regulatory requirements can be a challenge. The FDIC wants board members with prior banking experience that can guide the management team, said both Davis and Victoria Reider, partner at Dilworth Paxson and former head of the Pennsylvania Department of Banking.

"Board experience is a big, big thing. Regulators want an experienced board from the beginning," Davis said. "They want people on those boards who can actually provide counsel to the management team from day one."

The FDIC particularly pays close attention to which board members will serve on the audit committee, according to Reider.

"Do they have the expertise to really look into what the bank is doing?" she said. "If you don't have a real qualified CPA that's actually auditing the bank, that isn't sufficient."

The overall application process also remains complex, with little insight into what regulators are looking for, both Davis and Reider said.

"There could be better outreach by the agencies themselves too, to maybe spell out 'Here are some common shortcomings that we see in applications. Here are things that are going to get an application sent back to the chef,'" Davis said. "If the name of the game is to juice up applications, you certainly could be a little more transparent about what things are tripping up applications."

A de novo's business plan is particularly "scrutinized closely," Reider said.

Business plans "need to be fleshed out. You need to understand the community footprint that you're operating in. You need to understand the type of lending activity that you're interested in doing. I mean, if you want deposit insurance, you need to convince the FDIC that you know what you're doing, that you've really thought it through, that there is a need," she said.