09 Jul, 2026

Questions emerge on loan growth durability after lending strengthens again in Q2

By Harry Terris

Loan growth strengthened again in the second quarter, supporting expectations for net interest income even as tough competition likely weighed on loan spreads and funding needs put upward pressure on deposit prices, analysts said.

Some are asking how long the momentum can last.

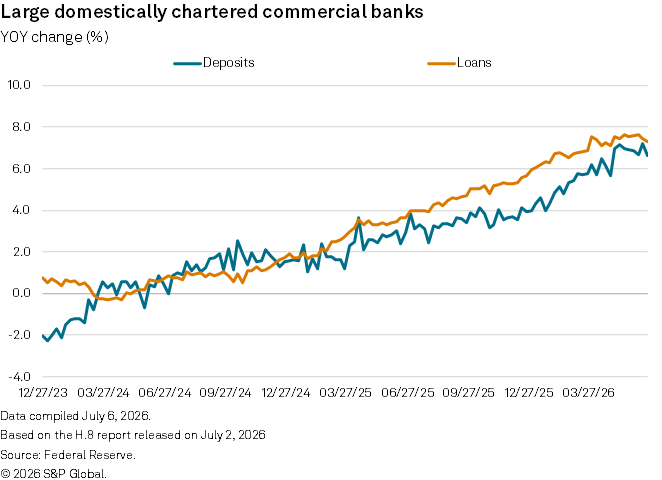

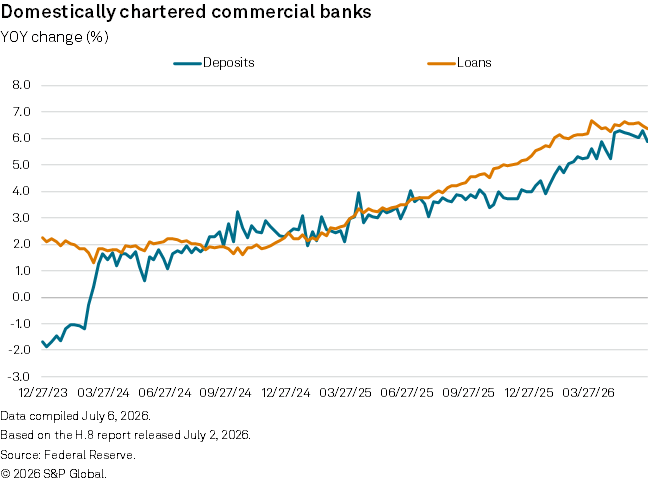

Year-over-year loan growth across domestically chartered banks ranged from 6.3% to 6.7% during the weeks ending in the second quarter through June 24, according to the most recent weekly data from the Federal Reserve. That is up from a range of 5.5% to 6.2% in the first quarter. Deposit growth accelerated to a range of 5.2% to 6.3%, from a range of 3.9% to 5.3%, while continuing to lag loan growth.

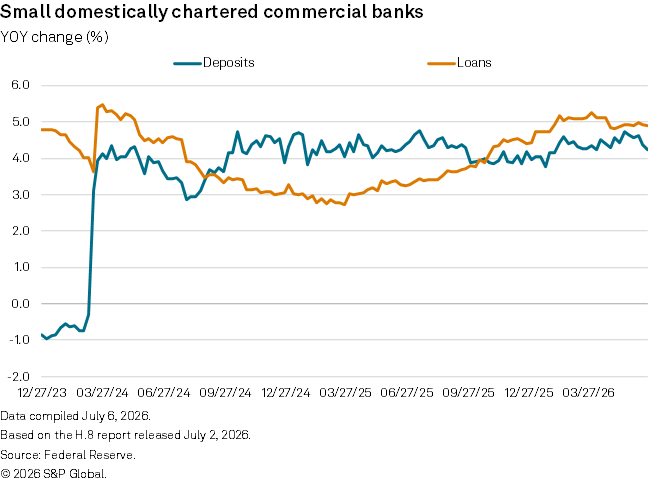

Large banks continued to lead the way. Loan growth at the 25 biggest banks by assets ranged from 7.1% to 7.7% in the second quarter, compared with 4.8% to 5.3% across the rest of the industry. Deposit growth at the large banks ranged from 5.7% to 7.2%, compared with 4.2% to 4.7% for the rest of the industry.

The Fed data "has remained upbeat, even accelerating in recent weeks," Piper Sandler analysts said in a June 29 note. "This growth should be sufficient to drive expansion in [net interest income (NII)], EPS, and overall capital levels."

Loan growth, supported by resilient commercial and industrial (C&I) demand, is "positioning banks to reiterate, and potentially bias toward the higher end of, full year guidance ranges," Jefferies analysts said in a June 24 note.

With industrywide loan growth running ahead of deposit growth, however, analysts underscored particularly intense deposit cost pressures at banks with high loan-to-deposit ratios and said the hot market is impacting loan yields as well. "We expect the lending market to remain highly competitive overall, particularly on pricing and structure for high-quality credits, which is likely to keep loan spreads compressed," the Jefferies analysts said.

Some analysts also emphasized that loan growth is vulnerable to a deterioration in economic and market conditions and called out signs of a slowdown late in the second quarter.

|

– Set email alerts for future Data Dispatch articles. – Download a template to generate a bank's regulatory profile. – Download a template to compare a bank's financials to industry aggregate totals. |

Loan growth, with caveats

C&I loans increased 2.4%, or $54.81 billion, from March 25 to June 24 across domestically chartered banks, and loans to nondepository financial institutions (NDFIs) increased 3.3%, or $46.76 billion, accounting for about 43% of the overall loan growth of $237.61 billion over the same period.

Commercial real estate loans were up 1.1%, or $32.80 billion. "We expect CRE payoffs and runoff to continue to weigh on overall loan growth, albeit at more moderate levels than in prior quarters," the Jefferies analysts said.

Approximations of sequential quarterly growth can be sensitive to cutoff dates used from the weekly data, which does not usually coincide with quarter-end dates.

From April 1 to June 24, total loan growth was substantially smaller at $158.44 billion. For the 25 biggest banks over the same period, C&I growth was 1.0%, or $15.40 billion, and NDFI loan growth was 0.8%, or $10.09 billion.

That represents "a sharp slowdown in period-end C&I plus NBFI loan growth," analysts at JPMorgan said in a July 6 note, and creates "some uncertainty about C&I loan growth outlook" for the third quarter. "This slowdown comes despite continued pressures at private credit funds from high redemption requests," they added.

However, the data supports strong sequential growth in average quarterly loans, the analysts said. They also projected median sequential ending-period loan growth of 1.4% in the second quarter across a group of 13 large-cap banks, compared with 1.6% in the first quarter.

"Investor focus appears to be shifting from current growth levels to the durability of existing loan pipelines should macroeconomic and geopolitical uncertainty persist," Raymond James analysts said in a July 1 note. However, recent conversations with banks and public commentary by executives "continue to point to healthy pipelines, solid demand trends, and broad reiteration of full-year outlooks."

Deposit pressures

Deposits, which are usually subject to big swings around tax season, increased 0.8%, or $136.99 billion, from March 25 to June 24 across domestically chartered banks. After seasonal adjustment, they increased 1.8%, or $308.02 billion.

Despite loan growth running ahead of deposit growth, aggregate loan-to-deposit ratios have been relatively stable. At the 25 biggest domestically chartered commercial banks, they ranged from 63.0% to 64.6% across the weeks ending in the second quarter, compared with 63.4% to 64.7% in the first quarter.

They were also stable across the rest of the industry, where they were also much higher overall. They ranged from 82.5% to 83.8% in the second quarter, compared with 82.6% to 83.4% in the second quarter.

With Treasury yields up across most maturities so far in 2026 and policymakers and futures markets anticipating a Fed hike this year, the "debate has shifted from peak funding pressure recovery to whether banks can protect NIMs," BofA Global Research analysts said in a June 25 note.

Bank commentary shows "a direct correlation between elevated loan/deposit ratios and intensified deposit competition," they added, saying that consensus forecasts expect a median sequential increase in interest-bearing deposit costs of 4 basis points across mid-cap banks in the second quarter, compared with a decline of 5 basis points the year prior.