10 Jul, 2026

Data center demand has investors reevaluating US electric utility stocks

By Allison Good

|

Utility stock prices have become more intertwined with data center power demand in recent years, prompting a valuation reassessment. |

AI data centers have upended the traditional investor view of electric utilities over the last two years, transforming a predictable industry that acted as a hedge against economic downturns into a growth sector with enormous upside, but also greater risk.

In doing so, the hierarchy of investor-owned power providers has shifted as vertically integrated utilities, independent power producers and wires-only utilities compete to serve the tech sector's surging demand for electricity.

Where operational performance, dividends and state regulatory environments once determined stock price premiums, investors now focus on whether utilities emphasize long-term spending and growth visibility over quarterly financial benchmarks and can lock down binding contracts with hyperscalers, industry analysts told Platts, part of S&P Global Energy.

Today, utility valuations reflect a hybrid approach: a blend of the certainty that comes with acting as a bond proxy and having a regulated monopoly, and increasing expectations for exponential profitability beyond 2030.

"You can't take a higher growth rate and think you have the same low-risk business, so you're going to have a little bit of defensiveness, a little bit of growth risk," CreditSights' Andrew DeVries said in an interview.

A new normal

The primary equity value distinction within the sector is between utilities with projected compound annual growth rates of 8% or greater and those with lower forecasts.

"Other factors may drive valuations, but [earnings per share compound annual growth rate (CAGR)] is now king," analysts at Mizuho wrote in a June 2 report. "The higher CAGR names are benefiting from emerging demand vectors that can compound beyond the current forecast window, while the lower CAGR names are largely executing against already well-defined plans."

But for utilities to retain their safe-haven status, investors still need proof that anticipated demand will materialize.

"If you're a bond proxy, you have to be able to underwrite that bond issuance, so utilities need to make sure they have firm offtake agreements," Evercore Managing Director Nick Amicucci said in an interview.

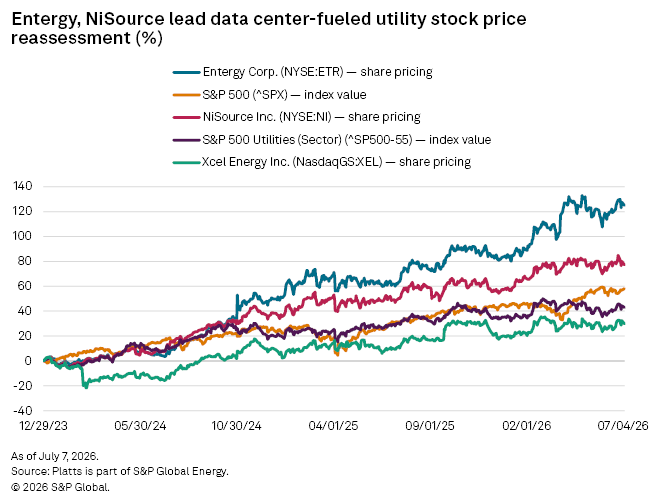

Entergy Corp., for example — which projects a 9% retail sales CAGR and a 16% industrial sales CAGR through 2030, and has the second-largest contracted data center pipeline across the sector, according to a June 1 Jefferies report — has seen its stock price surge nearly 150% since the beginning of 2024, substantially outpacing both the S&P 500 and the S&P 500 Utilities Index.

Analysts at Mizuho, Jefferies and CreditSights agreed that Entergy is one of the best-positioned to benefit from AI electricity demand.

They also named NiSource Inc., whose stock price has increased nearly 100% during the same period, as a top grower with significant data center commitments relative to the company's size.

Unlike Entergy, which is building additional generation in rate base to meet data center demand, NiSource's stock price also reflects an affordability premium, CreditSights' DeVries said.

NiSource will construct a new generation through NIPSCO Generation LLC, a ring-fenced affiliate of regulated utility Northern Indiana Public Service Co. LLC, designed to insulate residential ratepayers from higher bills and require hyperscaler customers to pay the costs.

DeVries anticipates that affordability will play a larger role in stock valuations.

"I think there will be a little bit of a shakeout in the group in maybe two, three or four years that focuses on who really protects the ratepayers," he said.

Compared to just a few years ago, investors are more focused on the regulatory "intricacies" within each state because "now you're talking about much larger magnitudes of deviation when it comes to upside as well as downside," Evercore's Amicucci said.

2nd wave of demand

Several of the utility companies guiding to relatively lower growth rates, including Consolidated Edison Inc., Dominion Energy Inc., Eversource Energy and Exelon Corp., were formerly vertically integrated, but shed their generation portfolios in the early 2020s to focus on transmission and distribution. Dominion has retained its generation assets, but sold off natural gas utilities.

"There was a lot of pressure to improve balance sheets at that time and bring cash flow in the door," Scotiabank Managing Director Andrew Weisel said in an interview.

Wires-only utilities are still positioned to potentially benefit from the second wave of data center demand.

"We're going to be talking about inference, reasoning and agentic data centers, where inevitably it's going to take the form of smaller installations, anywhere between 50 and 400 megawatts, and proximity and latency become a much bigger issue," Evercore's Amicucci said. "Some of those areas that couldn't accommodate these massive megacampuses become even more attractive."

AI inference is modular, geographically distributable and sensitive to latency, whereas AI training needs large, synchronized clusters of data centers.

Dominion's service territory in Northern Virginia, for example, is widely considered one of the most data center-dense markets in the world. But the region is constrained by transmission bottlenecks and has not seen the addition of large data centers under development that the South and Midwest are experiencing.

Once the company completes a slate of high-voltage transmission line projects, and as demand for faster AI response times increases, the data center build-out could shift back to that territory, Jefferies Managing Director Paul Zimbardo said in an interview.

Lingering skepticism

In the meantime, Jefferies has "seen a sharp uptick in investors looking for diversified companies whose growth rates are less inherently linked to data centers and AI."

Xcel Energy Inc., "in particular, offers top-tier growth with relatively limited data center reliance," the report continued.

"Old school" utility investors are generally more skeptical of the changes occurring in the industry, especially the increasing focus on generation, according to CreditSights' DeVries.

"If you go back 25 years, Enron was manipulating power prices and over a dozen utilities said, 'Hey, we're going to get into the unregulated power business,'" DeVries said. "That led to numerous bankruptcies, numerous companies handing the keys of power plants to creditors, and ... it was just an absolute disaster."

If "data center construction delays, adverse regulatory or legislative outcomes, supply chain constraints or broader macro headwinds cause companies ... to miss growth targets," the new "framework" for valuing stocks may no longer be applicable, Mizuho said in its report.

Most analysts never anticipated that regulated utilities would become the main beneficiaries of the AI boom. When Talen Energy Corp. sold a Pennsylvania campus to Amazon.com Inc. and agreed to provide it with power from the Susquehanna Nuclear plant in March 2024, they predicted that independent power producers would contract the lion's share of hyperscalers' electricity demand.

"It's really been the total opposite," Jefferies' Zimbardo said.

"The ability of the regulated utilities to be innovative and flexible was definitely a surprise," Zimbardo added. "It's been a big change internally and culturally for many companies."