03 Jun, 2026

US solar panel imports fall to lowest level in nearly 7 years in Q1

By Kirsten Errick and Umer Khan

US solar panel imports slid to their lowest quarterly level in nearly seven years in the first three months of 2026 as federal incentives and trade policies continued to reshape the photovoltaic supply chain.

The US imported 4.5 gigawatts of solar modules in the first quarter, down almost 50% from the prior quarter and down 32.3% from the first quarter of 2025, according to the S&P Global Market Intelligence Global Trade Analytics Suite.

That marked the lowest quarterly module shipment volume since the second quarter of 2019, the data showed, and came as the July 2025 budget bill's foreign entity of concern (FEOC) restrictions took effect.

"FEOC compliance didn't take effect until the start of 2026, so there was a natural rush to ship modules and cells before that deadline," S&P Global Energy Horizons principal market analyst Alex Kaplan said in a May 26 email.

Kaplan added that it is unclear "how much imports will recover," but there will likely "be a recovery after a quarter or two, and this was a natural lull after a policy-driven spike."

The falling US solar panel imports mirrored declining imports of lithium-ion batteries, which are also subject to the FEOC restrictions.

To meet ongoing strong demand in the US, solar project developers amassed stockpiles of safe-harbored and non-FEOC panels from abroad in 2025. Moreover, domestic module production capacity has grown to roughly the size of the US solar market — fueled by the Biden-era tax incentives to which Republicans and President Donald Trump added the FEOC rules.

The US Treasury Department and the IRS issued interim FEOC guidance in February, though several stakeholders have called for more clarity and the industry is awaiting additional guidance.

In the meantime, new and pending trade cases continue to target foreign shipments, largely from suppliers linked to China.

Several US solar manufacturers filed an anticircumvention case in May that claimed China is evading restrictions by routing components through Ethiopia. There is also a pending antidumping and countervailing duty (AD/CVD) case on solar imports from India, Indonesia and Laos, sometimes referred to as Solar 4 because it is the industry's fourth AD/CVD case. Commerce set duties in mid-2025 in the third AD/CVD investigation on imports from Cambodia, Malaysia, Thailand and Vietnam.

The solar industry is also awaiting the decision on a national security investigation into foreign polysilicon.

Indonesia was the largest source of US solar module imports in the first quarter at 40.6%, down from 64.5% in the prior quarter. The other markets in the top five were the Philippines (24.8%), Ethiopia (9.2%), and Laos and Vietnam (both at 4.6%). Imports from Vietnam and the Philippines increased from the previous quarter.

The remaining countries in the top 10 for the first quarter were Nigeria, Malaysia, Singapore, South Korea and Kenya.

"We are seeing the impact of the Solar 4 investigation," Rob Gardner, vice president of congressional and regulatory affairs at the Solar Energy Manufacturers for America Coalition, told Platts, part of S&P Global Energy. "Imports are down this quarter, but we are seeing another supply chain shift, similar to what we saw about 10 months into the Solar 3 investigation. Module imports were down 90% in Solar 4 countries Indonesia and Laos, while the Philippines, Turkey and Ethiopia and now Nigeria and Kenya have become major exporters. This follows a dramatic increase in exports of cells from China to these countries."

The US imported 3.7 GW of cells in the first quarter, down 20.9% from the prior quarter and down 16.5% from the first quarter of 2025.

South Korea was the largest source of solar cells with 31.9% market share, up from 22.2% in the prior quarter. It was followed by Thailand (22.2%), Indonesia (12.4%), Ethiopia (9.1%) and Malaysia (9%). These top five markets of origin accounted for 85% of solar cell imports.

The remaining countries in the top 10 for the first quarter were the Philippines, Turkey, Taiwan, Laos and Tanzania.

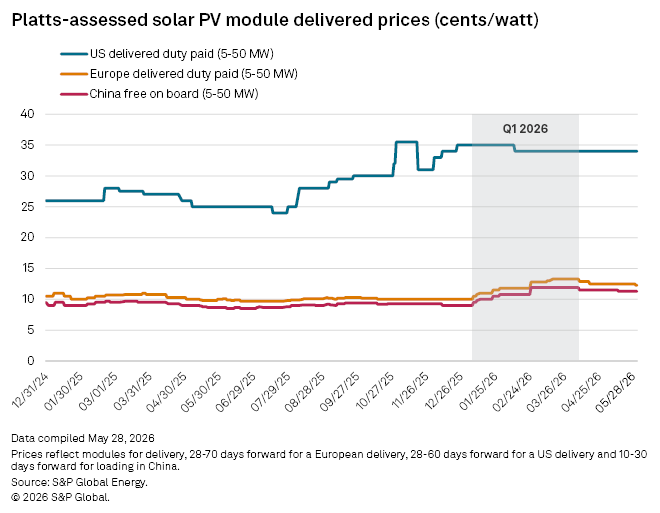

Average monthly prices for Platts-assessed delivered-duty-paid US solar Topcon modules for 5-50 MW volumes averaged 34.4 cents per watt over the first quarter, up 28.8% from the first quarter of 2025.

The price has remained at 34 cents per watt so far in the second quarter of 2026. That is approximately three times higher than prices for the Europe delivered-duty-paid 5-50 MW and the China free-on-board 5-50 MW, as assessed by Platts.