02 Jun, 2026

Smaller companies opting for reduced reporting more exposed to stock volatility

By Nick Lazzaro and Umer Khan

| US Securities and Exchange Commission Chair Paul Atkins speaks before ringing the bell at the Nasdaq stock exchange Dec. 2, 2025, in New York City. Under Atkins, the SEC has proposed policies, such as allowing companies the option to report earnings semiannually rather than quarterly, aimed at promoting IPO activity and increasing the number of public companies in the US. Source: Michael M. Santiago/Getty Images News via Getty Images. |

Smaller companies are more likely than larger companies to opt for less frequent mandatory financial filings if given the option, though reduced reporting may expose them to higher stock volatility.

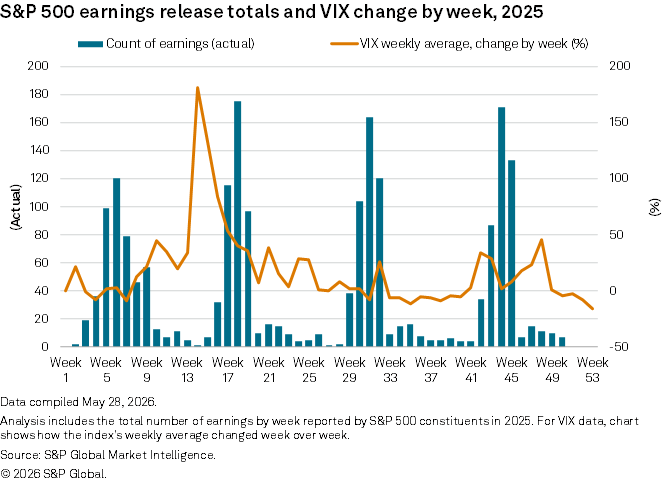

Stock market volatility as measured by the CBOE Volatility S&P 500 Index (VIX), also known as the market's "fear gauge," increased near earnings reporting cycles in the second half of 2025 while declining or remaining steady during quieter weeks of earnings releases, according to an analysis of S&P Global Market Intelligence data. The six-month period was bookended by periods of broader volatility marked by the announcement of US tariffs in the second quarter of 2025 and the onset of the Middle East war during the first quarter of 2026.

The SEC proposed a rule in May that, if passed, would allow public companies to report earnings twice a year instead of quarterly through Form 10-Q disclosures. The change could particularly benefit smaller companies and encourage more private companies to go public by alleviating compliance burdens, reducing costs and allowing management to focus on long-term goals. However, longer intervals between earnings reports could reduce transparency.

"Volatility could increase during earnings cycles as a result of bigger information shocks, with six months of developments being digested at once," Joseph Ferino, member of corporate transactions and financial services at Brach Eichler, told Market Intelligence. "This may matter to small- and mid-cap companies, as the market likely will still receive a large amount of information on large-cap companies."

Larger companies with established resources and more expansive analyst coverage are likely to maintain quarterly reporting cycles.

"I suspect many large-cap companies will keep quarterly reporting, at least initially, as well as companies in industries where investors demand frequent data such as banks, insurers, retailers and airlines," Ferino said. "Companies with sophisticated institutional investor bases may also keep quarterly reporting because their investors and the market may demand it."

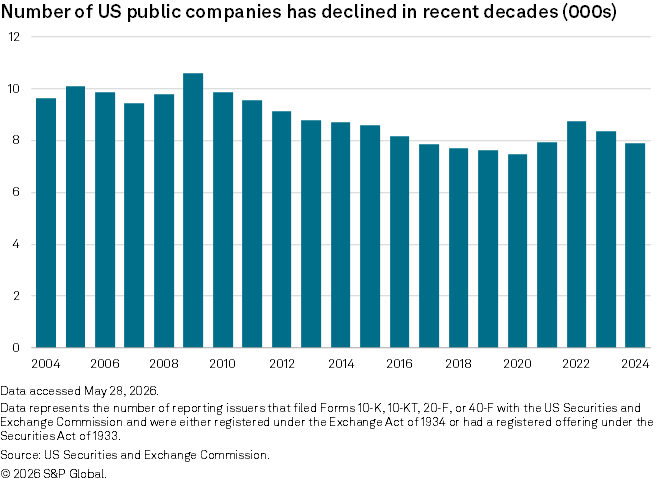

The proposal to allow less frequent financial reporting is part of the SEC's broader agenda under Chair Paul Atkins to promote IPO activity and increase the number of public companies in the US, a figure that has declined in recent decades.

Broad vs. single stock volatility

Broader equity market volatility could be tempered in the future if the SEC's proposed change shifts investment strategies, similar to markets in the EU and UK that already allow semiannual reporting.

"Historically, the UK and EU markets have been more long-term focused markets, and moving to a similar reporting cadence in the US is in part designed to promote a similar, long-term investing focus," Jen Moldaver, managing director at IQ-EQ, told Market Intelligence. "This shift might remove some of the short-term, event-driven volatility in US markets that results from sentiment-driven trading volume."

Still, during bouts of market uncertainty, individual stock price volatility will be more common for companies that choose to report semiannually, but prices will likely "move back to the correct market valuation through communications from investor relations or other signaling from the company and management," Moldaver said.

Multiple factors are likely to drive cross-sectional volatility among individual stocks.

"Cross-sectional volatility could increase as the range of forecasts of earnings growth, evolving company fundamentals, and positive and negative earnings surprises will likely rise in between semiannual reports," Steve Dean, chief investment officer for Compound Planning, told Market Intelligence.

Uneven information access

Analysts would need to rely more heavily on estimates or alternative data sources to fill information gaps for companies that report financial statements less frequently.

"Those with better access to either alternative sources of company data or closer connections to company management are likely to have better estimates in between reported results," Dean said. "Forecasting company results is hard enough without as frequent of a feedback loop on the accuracy of those forecasts."

Analysts may also have more difficulty relying on company comparisons to generate forecasts if industry peers are not reporting financial statements at the same frequency, Dean said.

While mid- and small-cap companies already receive less analyst coverage than their large-cap peers, choosing to report earnings less frequently may further reduce coverage of these companies.

"That may increase the already relatively higher possible misvaluations or inefficiencies for mid- and small- cap stocks, which could be an opportunity for active managers to capitalize on wider information gaps," Dean said.

Many smaller companies that opt for semiannual reporting may still be prompted by potential investors to provide additional disclosures and updated information between six-month earnings reports, according to Bruce Newsome, partner at Haynes Boone. This could impact companies such as those in need of additional early-stage funding.

"Those investors may very well want the company to consider putting out early information," Newsome said in an interview. "In that type of situation, companies would have to decide if the cost saving is worth it as compared to what investors are going to need if they're going to the market to raise capital on a more frequent basis than others."