03 Jun, 2026

SEC reforms aim to spur US IPO pipeline, expand capital-raising options

| The US Securities and Exchange Commission is considering a series of proposals to encourage more IPOs. Source: hapabapa/iStock Editorial via Getty Images. |

The US Securities and Exchange Commission is considering a series of proposals designed to entice more companies to go and stay public.

The SEC recently announced a trio of proposed reforms that aim to make IPOs more attractive by reducing compliance requirements for many companies. One proposal seeks to change the way public companies are categorized, and a second would make it easier for public companies to raise capital through shelf registrations. A third proposal would reduce the required frequency of earnings reports from quarterly to semiannually.

Legal experts and market observers agree that if enacted as written, the proposals would represent the most significant reform to securities regulation in over a decade. There is less agreement on whether the changes would accomplish SEC Chairman Paul Atkins' goal to increase IPOs, with experts noting that myriad factors influence business leaders' decision-making on when and if to take a company public.

"It's the commission's view that the existing disclosure requirements are too burdensome, and they believe that it will be less costly for companies to be public if we substantially scale back the required disclosures," said Jill Fisch, the Saul A. Fox Distinguished Professor of Business Law at the University of Pennsylvania Law School. "Whether or to what extent that works remains to be seen."

Extending the on-ramp

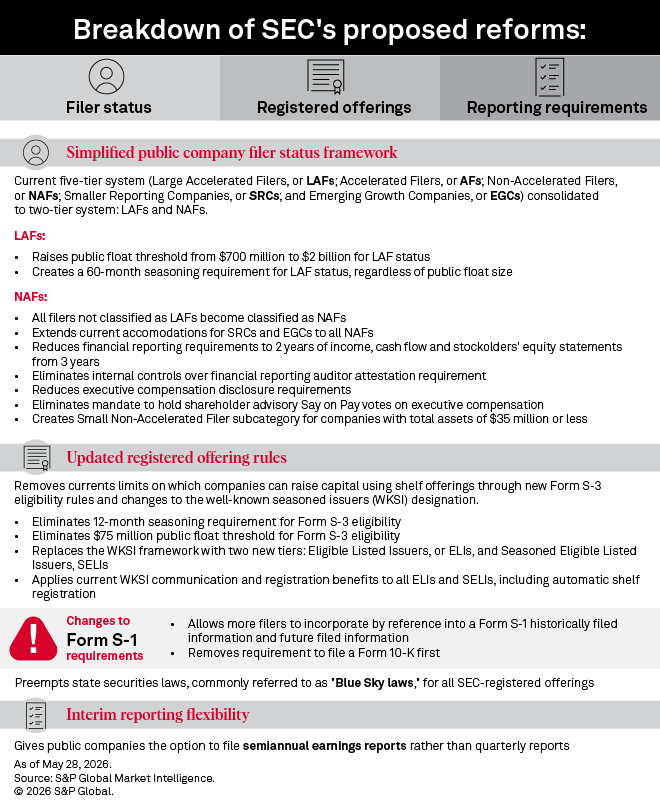

Of the three SEC proposals under consideration, the one that would collapse the five-tier filer status framework into two tiers stands to have the most impact on companies considering whether to go public, said Mike Bellin, IPO services leader at PwC US.

The current five tiers range from large accelerated filers (LAFs) at the top to emerging growth companies (EGCs) at the bottom. LAFs, with a public float threshold of $700 million, have greater reporting requirements, based on the assumption that larger companies can afford the additional costs.

The SEC's proposal would raise the public float threshold for LAF status to $2 billion, which the SEC estimates represents 20% of registrants. The proposal would also collapse the four smaller tiers into a single non-accelerated filer (NAF) category, comprising the remaining 80% of registrants. Notably, all NAFs would be subject to a number of exemptions and accommodations reserved for the smallest companies, and all newly public companies, regardless of float size, would receive NAF status for a period of five years.

With the extended accommodations, NAFs would only need to provide two years of audited income and cash flow statements, rather than the three years currently required for most registrants. NAFs would also not be required to obtain an independent auditor's attestation of management's assessment of the effectiveness of the company's internal controls over financial reporting.

"If those are adopted, it's going to reduce the cost and time of IPO preparation, and [the] cost to be a public company," Bellin said. "It doesn't mean internal controls is going away ... It just means the auditor attestation of it, which can be a heavy lift for many companies, is deferred for five years as a newly public company."

Staying true to one's shelf

For newly public or smaller publicly traded companies, the SEC's proposal to expand eligibility to raise capital through the short-form registration process on Form S-3 is likely to be more significant than the filing tier changes, according to Frank Zarb, a partner in Proskauer Rose LLP's corporate department.

Form S-3 allows eligible publicly traded companies to quickly offer and sell securities to the public without filing the more detailed Form S-1. Form S-3 is commonly used for shelf registrations, in which companies register securities to be sold at some point in the future. Under current Form S-3 eligibility requirements, companies must have been public for 12 months and have a public float of at least $75 million. The SEC proposes to eliminate both of those eligibility requirements.

The changes would benefit newly public companies, which currently have to wait 12 months after their IPO before using the short-form registration, Zarb noted.

"A lot of what the SEC has been doing under the current administration has been making it more attractive to be a public company and to raise money in the public markets rather than the private markets," Zarb said.

Additionally, the SEC proposes to eliminate its well-known seasoned issuers (WKSIs) category, which confers certain reporting and communications benefits to the largest companies. Instead, it would create two new categories, eligible listed issuers and seasoned eligible listed issuers — both of which would have access to many of the benefits reserved for WKSIs, such as pay-as-you-go filing fees and the ability to make prefiling offers.

"The way that the current rules are constructed, all the benefits are for the largest companies that have been reporting the longest," Zarb said. While there are exemptions for the smallest companies, "there's a big gap in the middle class of public companies," Zarb added.

The SEC estimates that only 34% of reporting issuers qualify as WKSIs. Under the new SEC proposal, 74% would qualify as SELIs.

"To give the behemoth public companies these advantages just because they're the largest isn't going to move the needle in terms of economic growth," Zarb said. "What you really need to do is provide more flexibility to the smaller and medium-sized growing companies that are creating jobs."

Semiannual vs. quarterly

A third SEC proposal announced in early May would enable companies to elect semiannual reporting, reducing the frequency requirement from quarterly.

Most market observers see this proposal as having a smaller impact on whether companies go public than the other proposals.

"A public company balancing its books and reporting those numbers every 90 days to its owners is hardly onerous," said Brenon Daly, an analyst with 451 Research from S&P Global Energy Horizons. "Millions of households manage to do a similar thing every single month."

Bellin, though, said with reduced reporting requirements, some smaller companies might issue quarterly financial information in a press release as opposed to a formal Form 10-Q.

Overall, savings for newly public companies could be significant if the SEC's proposals are adopted as written, said Davina Kaile, corporate and securities partner and global leader of Pillsbury Winthrop Shaw Pittman's capital markets and public companies practice.

"I think it could be meaningful in the six-figure savings for a small reporting company if they only had to do biannual and scaled disclosure," Kaile told Market Intelligence.

For larger companies, though, Kaile said other factors — including how much information buy-side investors demand, required reporting under existing debt covenants and the reporting frequency of industry peers — will determine how many adopt semiannual reporting if the proposal is implemented.

IPO impact

It remains under debate as to whether adopting the SEC's proposals would prompt more companies to go and stay public.

"The companies that are sitting on the sidelines today ... are not necessarily waiting for these reforms," Bellin said. "They're waiting for volatility to settle. They're waiting for the macro environment to be right for them. They're making sure they're ready to be a public company and their metrics are working out."

He said that a trio of highly anticipated IPOs this year — those for Space Exploration Technologies Corp., OpenAI LLC and Anthropic PBC — could "capture the attention of the marketplace" and add momentum to the market, regardless of how soon the SEC moves on reforms.

Even with the proposed changes, the ease and speed of raising capital in the private markets will still trump public capital raising.

"The real reason we see more long-term private companies is deregulation of private capital raising. And if you don't have to go public, you don't," said UPenn's Fisch.

Zarb agreed that when it comes to the IPO market, much remains outside the SEC's control. He pointed to the war in Iran, oil prices, inflation, interest rates and whether ships can get through the Straight of Hormuz.

Nevertheless, Zarb said the SEC's goal seems to be to make the IPO pipeline bigger by removing as much friction as possible.

"I think the SEC is going to move quickly to adopt these proposals because it wants the framework to be ready if economic conditions support a larger volume of IPOs," Zarb said.