19 Jun, 2026

Rate hikes to have mixed impact on EU banks' net interest income

Interest rate hikes would have an uneven effect on net interest income across EU banks, the European Banking Authority (EBA) said.

Resurging inflation amid heightened geopolitical uncertainty in the first half of 2026 has driven a shift in central bank policy and brought interest rate risk back into focus as a supervisory concern, the EBA said in its latest risk assessment report released on June 18.

While current data suggests the overall impact of a policy tightening should be an overall positive for banks' net interest income (NII), the average result "conceals an important heterogeneity," the EBA said.

A rate increase of 200 basis points would mainly benefit institutions with "predominantly floating-rate asset books and sticky deposit bases, as asset yields reprice faster than funding costs in such cases," the EBA said.

However, for banks with largely fixed-rate loan portfolios, there would be limited benefit or even a negative impact on NII over the short term given that "higher funding costs might materialize before fixed-rate books reprice."

Current interest rate risk in the banking book (IRRBB) data suggests a bigger benefit for banks in predominantly variable-rate mortgage markets such as Spain, Portugal and Finland, the EBA said. The impact could be more adverse for savings and cooperative banks in countries such as Germany, Austria and France, which have higher fixed-rate asset concentrations and slower repricing deposit bases, it noted.

IRRBB scenarios may not capture all risks that may emerge under more complex moves of the interest rate curve, so authorities across the EU member states should do further analysis on how those changes would affect banks, the EBA said. Banks' interest rate positioning and management, the way they hedge for interest rate risk, and the structural features of the market they operate in should all be considered, it added.

"Banks and supervisors should also remain attentive to the risk that hedging structures conceived under one rate scenario may perform poorly under a different shock configuration," the EBA said.

The latest economic data suggests that interest rates are expected to stay higher for longer across major jurisdictions, including the EU, the UK and the US, due to inflationary pressures fueled by the Middle East war. The ECB raised its key deposit rate to 2.25% from 2% on June 11 and is expected to raise rates twice more by year-end, according to economists at ABN Amro.

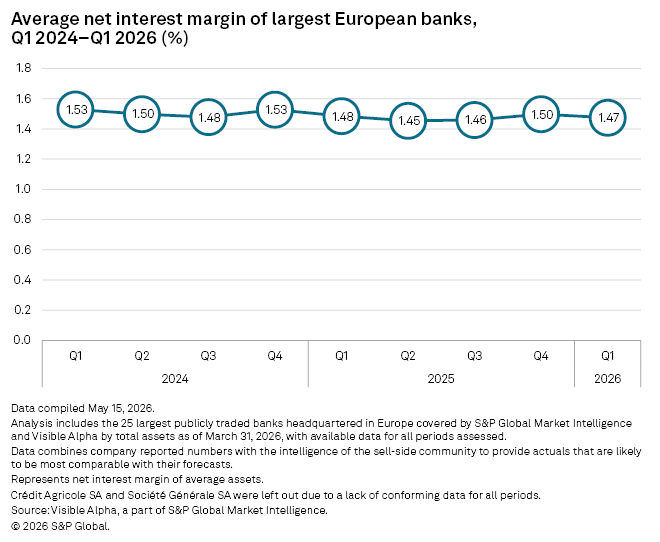

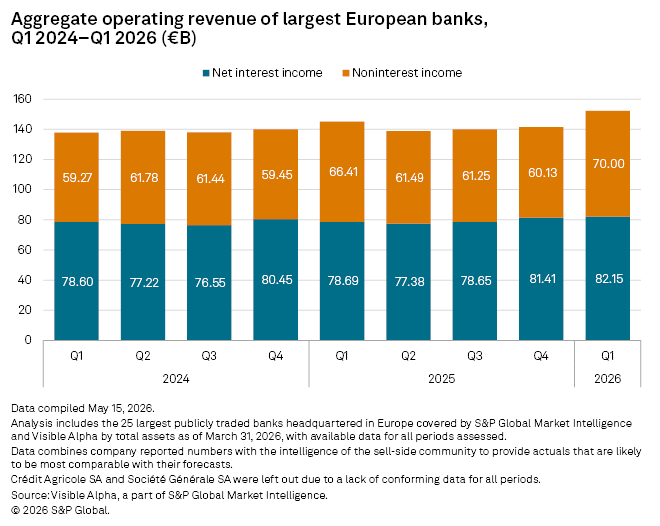

Aggregate NII at the 25 largest European banks has increased in each of the last three quarters, S&P Global Market Intelligence data shows.

Net interest margins (NIMs), which measure NII as a share of banks' average interest-earning assets, dipped in the first quarter of 2026, the data shows.