22 Jun, 2026

Intesa Sanpaolo looks for new growth driver with €31B Monte dei Paschi deal

By Cathal McElroy and Uneeb Asim

Intesa Sanpaolo SpA €31 billion move for Banca Monte dei Paschi di Siena SpA would extend its strong run of fee growth in recent years and decrease its reliance on net interest income (NII) as interest rates fall, S&P Global Market Intelligence data shows.

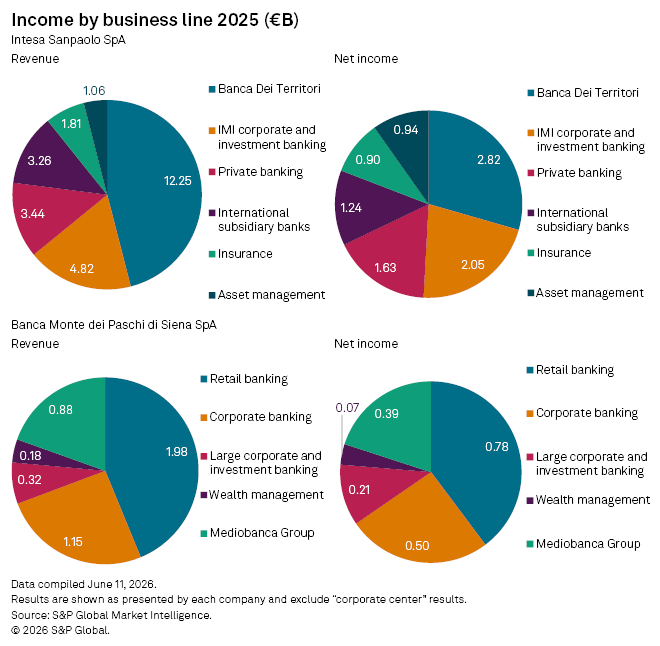

The deal would shift Intesa's revenue profile further away from retail banking and net interest income — the difference between what banks earn from interest on lending and pay for funding — and toward fee-generating businesses such as wealth management and corporate and investment banking. Pressure from falling interest rates has weighed on the bank's NII, its largest source of revenue, which fell by 1.6% to €17 billion in 2025, the data shows.

Robust fee growth in the last two years has helped offset Intesa's lower NII. Net fee and commission income increased more than 11% to €11.28 billion in 2025, after a 9.5% rise in 2024.

Intesa CEO Carlo Messina has said the bank aims to become the Italian version of Swiss wealth management giant UBS through the deal.

"If successful, Intesa's proposed deal would in our view consolidate its leading franchise and competitive edge in Italy," S&P Ratings said in a June 9 report on the deal. "It would also strengthen Intesa's corporate and investment banking proposition through Mediobanca Banca di Credito Finanziario SpA's expertise."

Intesa's domestic and international retail banking networks generated only 45% of its net income from 60% of revenue in 2025.

Monte dei Paschi's (BMPS) non-retail banking operations produced just over half of its 2025 net income from 45% of revenue. Intesa's plan to offload almost half of BMPS's retail network to BPER Banca SpA for antitrust purposes via an agreement with insurer Unipol Assicurazioni SpA also serves to reduce its retail exposure while adding about €1 billion in revenue and €380 million to its annual accounts.

Intesa operates almost 2,500 branches across Italy, the data shows. The bank plans to retain 625 BMPS branches, while BPER would take the other 635 should it agree to the deal with Unipol, its largest shareholder. BMPS has a much stronger presence in its local market of Tuscany compared to Intesa and BPER, which would provide an attractive opportunity for both to grow in that market.

All three banks have a strong presence in Italy's north, the country's economic powerhouse. The overlap among the banks in the region suggests Intesa and BPER should have significant opportunities for cost synergies as they integrate BMPS's branches into their branch network and optimize their footprint. The deal is expected to generate €1.5 billion in cost synergies pretax per year for Intesa.

"Recent domestic transactions demonstrate that cost synergies are significant and execution risk has been relatively modest, especially since most entities now have a strong track record of integrating newly acquired banks in a relatively short period of time and without meaningful disruptions," S&P Ratings said.

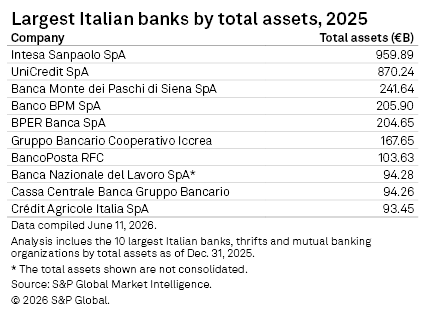

The deal will promote Intesa to the league of Europe's banking giants with total assets of more than €1 trillion, the data shows. Intesa is already Italy's largest bank with almost €960 billion of total assets as of the end of 2025, around €90 billion more than second-placed UniCredit SpA. Intesa will absorb the majority of the almost €242 billion in total assets BMPS held at the end of last year.

The country's largest lender had appeared an unlikely participant in the ongoing consolidation of Italy's banking sector due to its scale and the potential antitrust issues it would face with further domestic acquisitions.

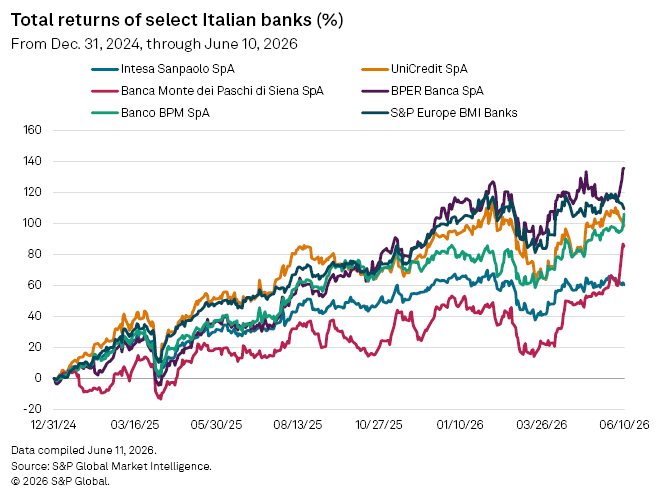

The limits on Intesa's ability to grow in its home market have contributed to less enthusiasm for the bank's stock among investors relative to its domestic peers. It has recorded the weakest total returns among Italy's largest banks since the sector's M&A rush commenced in early 2025, partly due to the surge in BMPS's share price since Intesa's deal was announced.

Intesa's total returns rose about 60% from the beginning of 2025 to June 11, according to the data. Three of Italy's largest lenders — BPER Banca, UniCredit and Banco BPM SpA — enjoyed total returns growth of more than 100% during that time, while Banca Monte dei Paschi rose by almost 80%.

Investor support for BMPS surpassed that for Intesa despite the Siena-based lender suffering repeated negative headlines during the period, including the launch of an investigation in November by Italian authorities into CEO Luigi Lovaglio and the bank's two largest shareholders and a failed attempt in March by its board to oust the CEO.

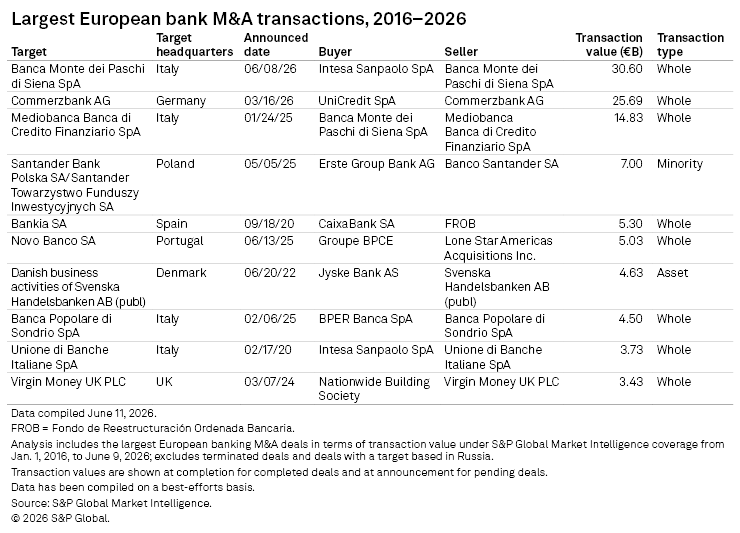

If successful, Intesa's €31 billion deal for BMPS will become the largest European banking M&A deal in the last decade, almost double the size of BMPS's €17 billion takeover of Mediobanca last year.

Italian banks dominate the ranking of Europe's largest executed and proposed bank M&A deals in the last 10 years. UniCredit's ongoing €25.7 billion move for German lender Commerzbank AG would rank as the second-biggest during the period. BPER Banca's €5.42 billion acquisition of Banca Popolare di Sondrio S.p.A last year and Intesa's €4.22 billion deal for Unione di Banche Italiane SpA also make the list.

Intesa is offering 16 newly issued ordinary shares for every 10 MPS shares tendered, along with €1 cash for every MPS share tendered. The offer represents a 12.5% premium to MPS's June 5 closing price.