01 Jun, 2026

Insurers prepared to weather 'below-average' Atlantic hurricane season

By Tom Jacobs and KRIS ELAINE FIGURACION

|

Homes in Homestead, Florida, that Hurricane Andrew leveled August 24, 1992. The Category 5 storm, the only hurricane to strike the US mainland that year, inflicted between $37 billion and $40 billion (2025 dollars) in insured losses and caused 65 deaths. |

Insurers are set up to handle any fallout from the looming hurricane season as local and state officials warn against complacency despite forecasts calling for a decreased amount of activity.

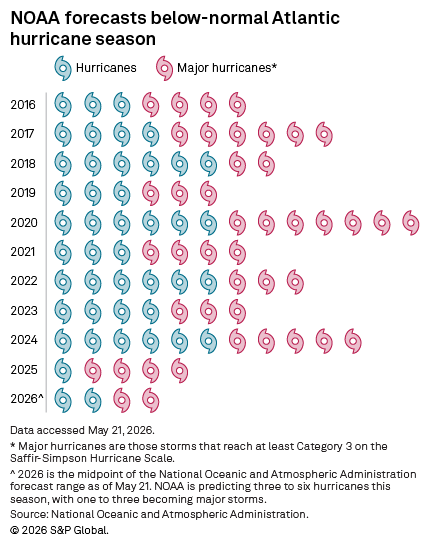

The National Oceanic and Atmospheric Administration (NOAA) said in a news release that there is a 55% chance of a "below-normal" number of named storms for the 2026 Atlantic hurricane season, which runs from June 1 through Nov. 30, and a 35% chance of a "near-normal" amount of activity.

NOAA is forecasting eight to 14 total named storms for the season, with three to six expected to become hurricanes, defined by winds of 74 mph or higher. As many as three are expected to develop into major hurricanes, Category 3, 4 or 5, with winds of 111 mph or higher.

AccuWeather is predicting a similar level of activity, anticipating that between three to five named storms will impact the US, while Colorado State University is forecasting 13 named storms and six hurricanes, two of which it expects to intensify into major hurricanes.

The prospect of another mild hurricane season on the heels of the quietest season in a decade, combined with P&C homeowners insurers reporting record-low combined ratios, bodes well for insurers like those in Florida's resurgent market, said CFRA Research analyst Cathy Seifert.

"Most insurers are entering hurricane season in pretty decent shape," Seifert said in an interview, adding that "Florida really has done a good job of implementing building code changes and really tightening up things so that their structures withstand these pressures much better."

Insurers in the Sunshine State are also reaping the benefits of legislative reforms that have led to a stabilized market and attracted 20 new insurers since the reforms were enacted in 2023.

Progress in the Pelican State

Louisiana has also made strides in its mitigation and resiliency efforts through the Louisiana Fortify Homes Program (LFHP), which is patterned after a program Alabama started in 2011.

Louisiana Insurance Commissioner Tim Temple said that since 2023, when the program was initiated, 4,395 state homeowners have had their roofs fortified using LFHP grants and more than 9,000 homeowners have voluntarily had their roofs fortified.

"Our fortified roof program is a phenomenal success," Temple said in an interview. "We are the fastest-growing state in the country for fortified roofs, and we're going to continue to push and promote that."

The program will also benefit from a bill signed May 27 by Gov. Jeff Landry. The bill, HB 1187, will allow Louisiana Citizens Property Insurance Corp., the state's insurer of last resort, to transfer $50 million from bond assessment funds related to Hurricane Katrina and Hurricane Rita to the LFHP.

That funding is in addition to the $30 million the LFHP will receive through taxes and fees on insurance entities.

El Niño in command

The reason for the below-average hurricane season prediction is the behavior of El Niño, an atmospheric condition that influences cyclonic activity.

El Niño is characterized by the warming of ocean surface temperatures in the central and eastern tropical Pacific Ocean and the weakening or reversal of the east-to-west trade winds that blow along the equator. The presence of an El Niño knocks down the high winds in the upper atmosphere that are essential to the formation of a tropical cyclone.

As an El Niño increases in strength, it increases forecasters' confidence in the number of storms for the season, said Alex DaSilva, lead hurricane expert for AccuWeather. For the storms that do form, DaSilva said that El Niños usually push them away from the Western Gulf of Mexico, which lowers Texas's risk of significant impacts.

"The steering flow usually pushes stuff to the north and east," DaSilva said in an interview. "So areas such as the northeastern Gulf Coast and ... the Carolina coast line are the areas that could be impacted this year."

It only takes one

While El Niño tends to decrease the number of storms, it does not decrease the chances of a major hurricane making a destructive landfall. Dan Ward, senior director for model development for risk modeler Karen Clark & Co., said it is not unusual to have an active Atlantic hurricane season with below-average loss or an inactive season with one hurricane landfall that leads to an above-average loss.

"The 1992 hurricane season was far below average in terms of hurricane activity but was a massive year for losses because of Hurricane Andrew," Ward said in an email to S&P Global Market Intelligence. "On the other hand, the 2020 hurricane season had six hurricane landfalls, tying the record, but these landfalls were not in highly populated areas, and losses for the year were average."

Andrew, which devastated South Florida and caused insured losses of between $37 billion and $40 billion (2025 dollars), was the lone 1992 hurricane to make landfall in the US. Temple stressed to Louisiana residents preparing for the season that when it comes to a costly season, "It only takes one."

"[Below-average forecasts] ... create an opportunity to let their guard down and perhaps not prepare as they might otherwise," Temple said. "The cliche is 'plan for the worst, and hope for the best,' and that's part of the message, that we've got to go out there and just remind people, 'Don't let your guard down.'"