16 Jun, 2026

Europe's top banks signal pullback in lending to sectors vulnerable to oil shock

By Bea Laforga

European banks are taking measures to address the impact of an energy shock on their loan books, with some already scaling back lending.

Standard Chartered PLC, Barclays PLC and Banco Bilbao Vizcaya Argentaria SA are among the large European banks that are closely monitoring sectors sensitive to elevated energy costs, weaker demand and higher interest rates in the wake of the Middle East war.

It comes after the European Central Bank on June 11 raised interest rates, citing the longer-than-expected "major energy shock" that has started to spill over into the broader economy. European banks have already set aside more than €1.5 billion to cover potential losses related to the war and geopolitical risk, an analysis by S&P Global Market Intelligence showed.

"We don't see anything that's flashing red, but there's plenty that's amber that we're watching," StanChart Group CEO William Thomas Winters said during the bank's first-quarter earnings call on May 19.

Barclays remains "vigilant" about the inflationary impact of the energy shock and is reducing its exposure to "more highly leveraged non-investment-grade corporates," it expects to be "vulnerable to a weakening economy," Group CEO C.S. Venkatakrishnan told analysts at its April 28 earnings call.

Meanwhile, BBVA has put at least 12 subsectors on a watchlist — including transportation, electric power supply, steel and cement — developed an enhanced monitoring of vulnerable clients and is conducting stress testing to detect potential second-round effects of the conflict, according to CFO Luisa Gómez Bravo.

The bank is being cautious and disciplined with risk, but had not seen any sign of distress or pressure by the time of its April 30 earnings call, Gómez Bravo said.

Second-round effects

The European Central Bank (ECB), in its May 27 Financial Stability Review, warned of the potential credit risks related to vulnerable sectors, noting that potential second-round effects could be "material" and affect banks' exposures.

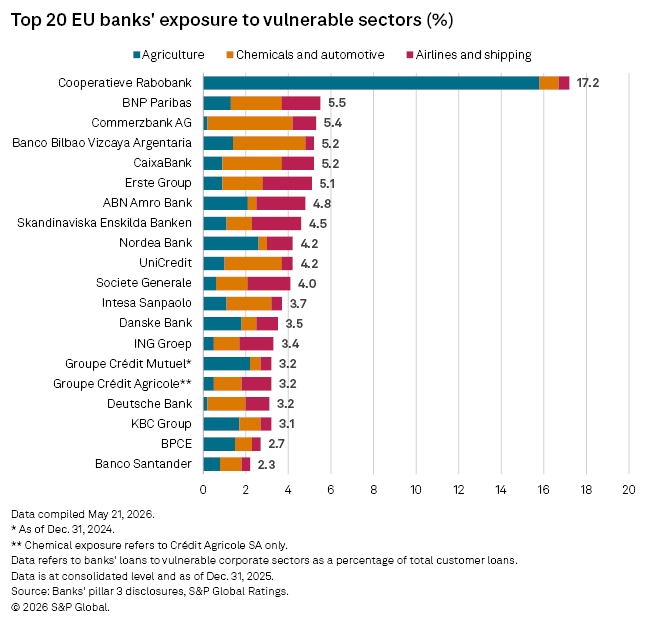

Europe's 20 biggest banks rated by S&P Global Ratings have a combined exposure of €400 billion to sectors vulnerable to an energy shock, representing about 10% of their total corporate loans and 5% of total customer loans. Ratings said these sectors — agriculture, automotives, chemicals and transportation — would face greater challenges in a downside scenario where disruption to energy and shipping flows through the Strait of Hormuz is extended and credit stress widens.

The agriculture sector, already reeling from structural challenges and higher tariffs, will be affected by elevated energy costs and supply chain disruptions, while spikes in fuel prices will mean significant cost pressure for European airlines and container shipping firms, Ratings said in a May 7 note.

High oil prices will threaten the region's commodity chemicals industry, which heavily relies on imported hydrocarbons and petrochemical feedstocks, while weaker business and consumer confidence may result in another year of low sales volume for specialty chemical companies. For automotives already weighed down by slow growth, trade tariffs and intense global competition, a prolonged shock would hamper recovery prospects, it noted.

"This stress would be driven less by the initial shock and more by duration, shortages of critical goods, second-round inflation effects and tighter financing conditions," it noted.

Long term impact

The Middle East war and closure of the Strait of Hormuz, where more than 25% of global seaborne oil trade passes through, have prompted wild swings in energy prices. Brent crude reached as high as $126 a barrel on April 30, compared to the $69 per barrel average in 2025.

The US and Iran, on June 14, were widely reported to have agreed on a deal to extend the ceasefire by 60 days and open the Strait. Still, the more than 100 days of war are likely to have a longer-term disruption to the energy supply.

Even if the Strait reopened in the third quarter, oil shipment traffic is only likely to return to pre-war levels by early 2027, according to the US Energy Information Agency's June 9 short-term outlook.

'Manageable drag'

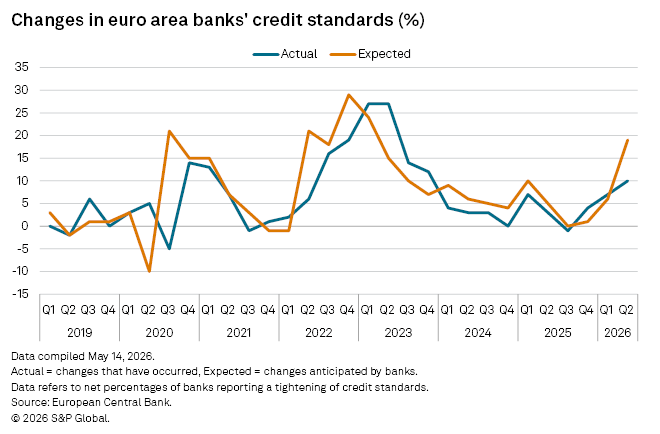

Euro area banks began tightening credit standards during the first quarter, reaching a level not seen since 2023, according to the ECB's latest euro area lending survey.

Banks cited higher perceived risks and lower risk tolerance, with some reporting additional tightening to energy-intensive firms and to the Middle East. Banks anticipate further marked tightening in the second quarter.

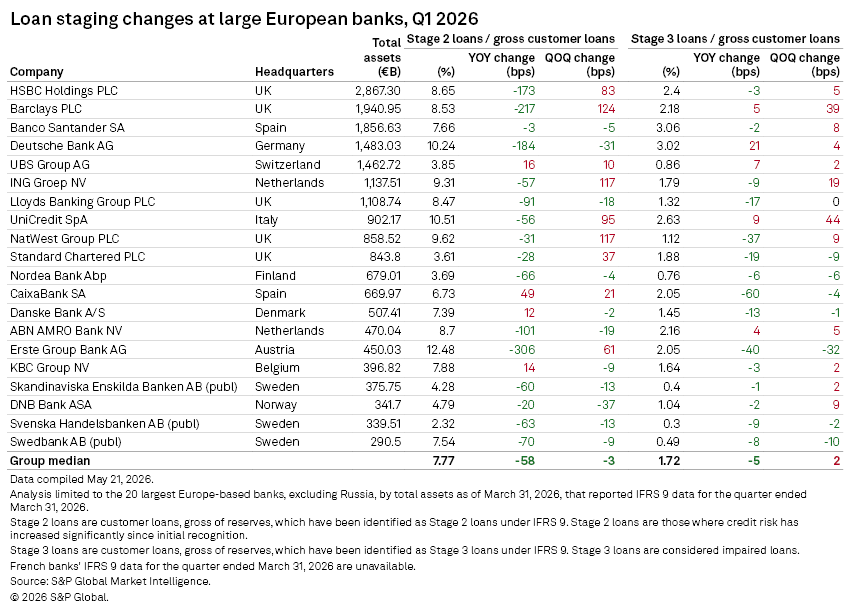

Asset quality, meanwhile, has stayed resilient. First-quarter Stage 3 loan ratios, which represent the share of bad loans to total customer loan book, of most large European banks improved versus a year earlier, according to S&P Global Market Intelligence data.

Stage 2 loan ratios, where the credit risk of loans has increased since origination, have improved for the majority of the lenders on both a quarterly and a yearly basis.

Still, Ratings sees Stage 2 ratios of large EU banks increasing by between 5% and 30% in 2026 as a result of the energy shock, though it does not expect a material change in Stage 3 ratios.

Higher credit costs and a potential deterioration in asset quality will be a "manageable drag" on profitability as banks have built strong capital buffers over the past years, and higher lending margins and efficiency gains provide an earnings boost, the agency noted.