24 Jun, 2026

Capital deterioration projected in stress test falls to lowest level in 7 years

By Harry Terris and Ayesha Shahbaz

Projected losses dropped for the second year in a row in this year's Federal Reserve stress test compared to the year prior, to the lowest level in at least seven years.

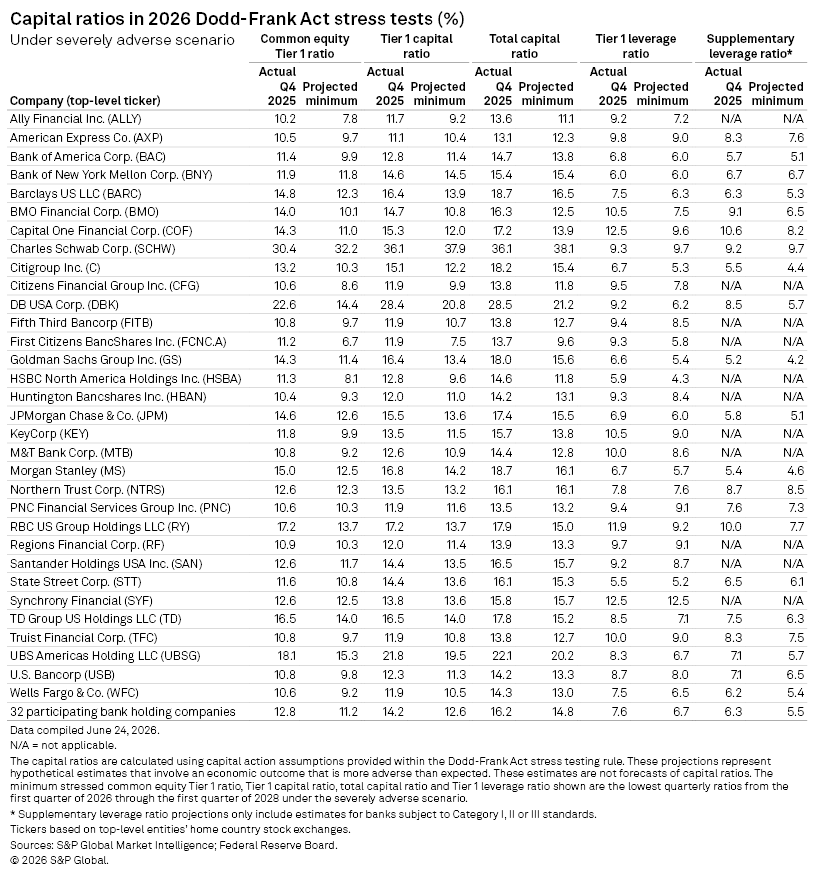

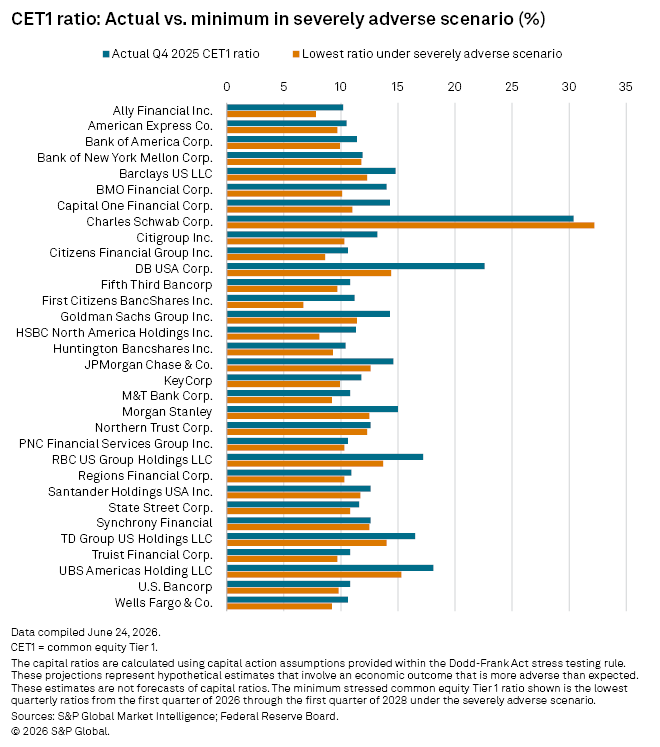

Across the 32 banks in the stress test, the aggregate common equity Tier 1 (CET1) ratio fell by a maximum of 1.6 percentage points, compared with 1.8 percentage points last year. The Fed said that larger projected loan losses due to loan growth in 2025 and factors, including harsher assumptions for corporate bond spreads and commercial real estate prices, pushed up losses overall. Moving in the other direction, recent loan growth lifted net interest income (NII) and produced higher projections for NII. A higher trough for interest rates used in the scenario also helped protect projected NII, and resulted in lower unrealized bond gains.

In a news release, the Fed said the hypothetical recession scenario used this year "was similar in severity to the prior test." Over the last seven years, the largest decline in aggregate CET1 was 2.8 percentage points in 2024.

Analysts and investors watch for changes in hypothetical losses from stress test to stress test since they inform capital requirements and offer a perspective on how banks would manage under different market and economic scenarios and other assumptions.

|

In this year's test, analysts expected better results for Category IV banks, which generally include banks with $100 billion to $250 billion in assets, that did not participate in the 2025 test, since the scenarios and assumptions used in the 2026 test appeared easier than those in 2024.

Citizens Financial Group Inc. and KeyCorp were among the banks in that size category that, in fact, showed better results in 2026 than in 2024. Both are subject to stress capital buffers (SCBs) above the minimum of 2.5%. At Citizens Financial, the maximum CET1 deterioration fell to 2.0 percentage points from 4.0 percentage points in 2024.

Overall, maximum CET1 deterioration declined at more than two-thirds of the participating banks compared with their most recent previous stress test.

Projected CET1 deterioration at Citigroup Inc. also continued to improve, declining to 2.9 percentage points from 3.2 percentage points in 2025.

The results this year are a signpost for how banks will fare as regulators pursue sweeping changes to the exercise. Hypothetical losses estimated bank by bank under the stress test determine individual SCBs, a component of the banks' overall capital requirements.

The Fed decided to keep banks' existing SCBs in place until 2027 as it seeks to implement a process for incorporating public feedback on the models it uses under a proposal from 2025. The Fed has also proposed other important changes to the stress test, including using results averaged over two years for SCBs.

|

Projected CET1 deterioration increased at JPMorgan Chase & Co., Wells Fargo & Co. and Goldman Sachs Group Inc., with the biggest increase at JPMorgan Chase to 2.0 percentage points from 1.5 percentage points in 2025.

In the 2025 test, the Fed called out trading positions at some banks in late 2024, reflecting "atypical client behavior" as an important factor helping the overall results.

That was not a factor this year, according to Federal Reserve officials, though trading losses were helped by a change in assumptions about how long banks would have to exit positions under stress.

In the aggregate, trading and counterparty losses fell to $37.1 billion in this year's test from $42.4 billion in 2025.