02 Jun, 2026

Blindsided lenders aim to reverse USDA program removal

The US Department of Agriculture's abrupt removal of lenders from a rural lending program has stunned those now appealing the decision.

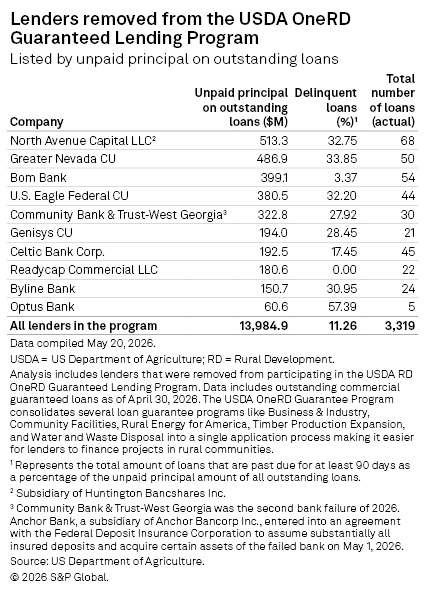

In what the agency itself called an unprecedented move, the USDA on May 12 issued a press release announcing the revocation of 10 institutions' program licenses and barring them from future participation in the Rural Development OneRD Guaranteed Lending program.

"This is an unprecedented action to revoke the privileges of the 10 lenders due to the significant findings of noncompliance with the regulatory requirements of the OneRD program," a USDA spokesperson said to S&P Global Market Intelligence. "We recognize that, given the unprecedented nature of these actions, some lenders may have been caught off guard. Under the leadership of the Trump Administration, high standards have been set for lenders participating in these taxpayer‑backed programs."

In February, the USDA temporarily paused the lenders' participation in the OneRD program, which provides commercial lenders with loan guarantees to make loans to businesses in rural areas, and asked for documentation to conduct an audit, according to the USDA spokesperson. The spokesperson said the USDA gave the lenders a 30-day notice that their licenses were being revoked, but several lenders said they felt blindsided by the decision.

|

The USDA requested an audit of four of its loans in March, then removed U.S. Eagle from the program in May. Though the credit union intentionally ceased participation in the program three years ago, it disagreed with the decision and submitted an appeal May 22. The USDA's removal of U.S. Eagle was "unreasonable," Moore said, as it was based on just the four audited loans.

"We were caught by surprise," Moore said. "Typically, when an entity like the USDA conducts a review of a program, it will come back with findings, opportunities for improvement, and provide us an opportunity to respond and discuss the issue. None of this happened with USDA."

Celtic Bank Corp. also felt the process lacked transparency.

"The USDA provided little transparency or communication during its recent review, despite full cooperation from Celtic. The USDA's criticisms and claims of noncompliance are inaccurate and unfounded. Celtic plans to appeal, and believes the USDA's actions will harm rural borrowers," a spokesperson for the bank said in a statement.

Several other lenders informed Market Intelligence of plans to work with the USDA to remediate or appeal, including Byline Bank, BOM Bank, Genisys CU and ReadyCap Commercial LLC.

Representatives from North Avenue Capital LLC and parent company Huntington Bancshares Inc., Greater Nevada CU, Community Bank & Trust - West Georgia, and Optus Bank did not respond to requests for comment.

BOM Bank is confident its lending status will be restored, President and CEO Ken Hale said.

"While we respect the Department's oversight role, we strongly disagree with the allegations cited in their press release," Genisys CU CEO Jackie Buchanan said in a statement. "This does not impact our lending going forward whatsoever, as USDA loans are less than 1% of our loan portfolio."

– Set email alerts for future Data Dispatch articles.

– Download a template to generate a bank's regulatory profile.

– Download a template to compare a bank's financials to industry aggregate totals.

Among the barred lenders, Byline was the largest bank at $9.9 billion in assets, and the only publicly traded bank among the revoked lenders. Analysts said its inclusion on the list was an unfortunate piece of media, but ultimately a non-event.

"I don't think it's material in the least," Piper Sandler analyst Nathan Race said in an interview. "Byline is generally a metropolitan-focused franchise in the city and Chicago suburbs, and there's generally, by the nature of the footprint itself, not a significant degree of USDA lending opportunities."

The USDA portfolio accounted for 0.6% of Chicago-based Byline's loan portfolio, according to an investor presentation.

Why these 10?

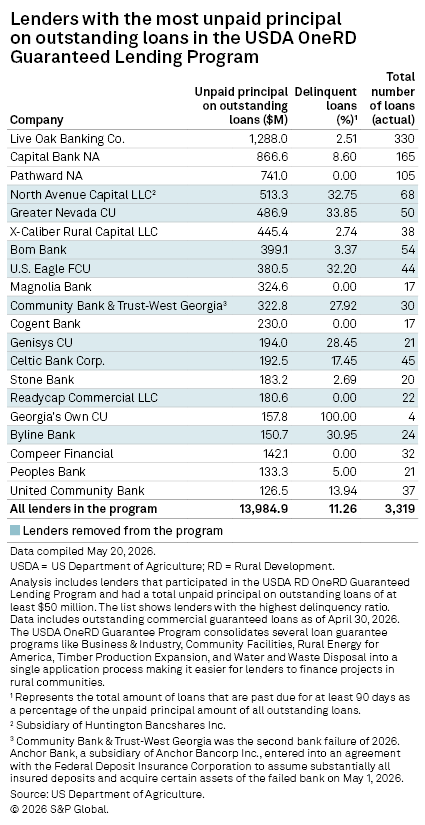

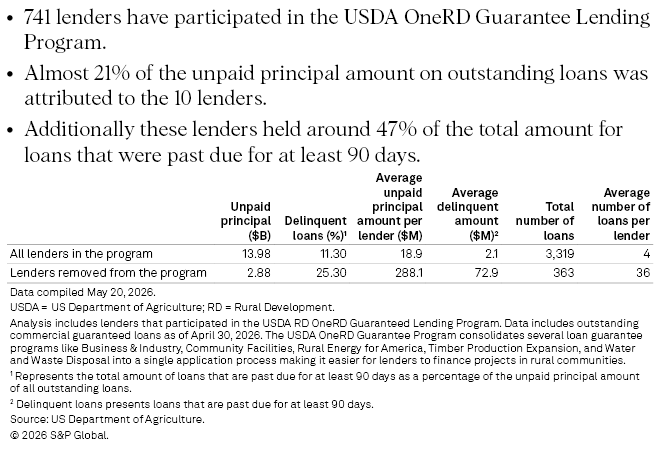

The USDA's press release cited the lenders' combined $620 million in delinquent loans that accounted for roughly 47% of Rural Development's delinquencies.

Out of 741 participating lenders, the removed institutions held 20.6% of all OneRD's unpaid principal and 10.9% of total loans, according to a Market Intelligence analysis. Delinquent loans accounted for 25.3% of the collective group's loan portfolio.

"The results of audits of these 10 lenders showed significant findings of noncompliance with the regulatory requirements of the OneRD program," the USDA spokesperson said.

The institutions removed from the program had an average unpaid principal of $288.1 million compared to $18.9 million for all lenders, and an average delinquent amount of $72.9 million compared to the program's overall average of $2.1 million.

|

One of the removed lenders, Readycap Commercial, had a 0% delinquency ratio. The entity said its license expired in January and was not renewed, and then it was barred from the program in May. ReadyCap commercial head of small business lending Gary Taylor said the USDA's characterization of the company was wrong, and it was not given an opportunity to address issues raised before its license expired and was not renewed.

"The USDA press release cites high delinquencies and losses as the basis for its enforcement action," he said in a statement. "Our USDA portfolio has no defaults or delinquencies and has not caused any loss to the agency, as reflected in USDA portfolio data."

Market Intelligence asked the USDA what criteria was used in deciding which lenders to cut and how they met that criteria. The USDA's official statement said that the agency's audit evaluated the lenders, their portfolios' health and potential noncompliance with regulatory requirements, evaluating the audit's results to make its decision.

When asked by Market Intelligence how often lenders are reviewed and why the action was announced now, a USDA spokesperson said, "Lenders are reviewed periodically for compliance with the regulations. Since taking office, President Trump has cited eliminating waste, fraud and abuse from government as a key priority. This and other actions being taken by the federal government underscore this commitment."

Among the list of removed lenders was Community Bank & Trust - West Georgia, which failed May 1 and had substantially all its insured deposits and certain assets assumed by Anchor Bank. The bank had entered a consent order in January with the FDIC over alleged unsafe or unsound banking practices and/or violations of the law. Later, its parent company, Community Bankshares Inc., was issued a cease and desist order from the Federal Reserve Board and the Georgia Department of Banking and Finance.

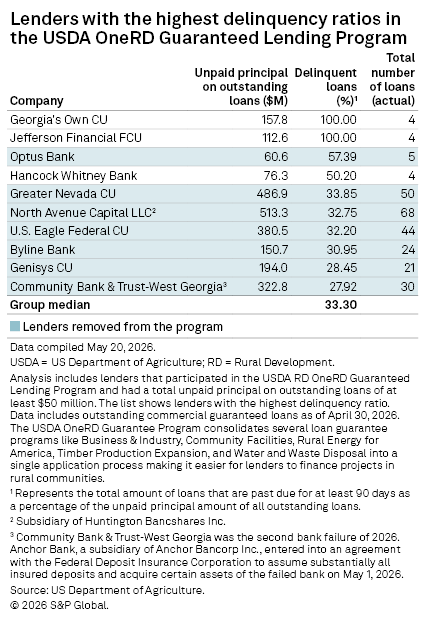

Other institutions had higher delinquency ratios than the removed lenders, including Georgia's Own CU and Jefferson Financial FCU, whose four loans apiece were 100% delinquent. Jefferson Financial was acquired by Keesler FCU in 2025. In a response to a request for comment, Keesler FCU said it does not participate in the OneRD program.

Hancock Whitney Bank, a subsidiary of Hancock Whitney Corp., was also among the top lenders by delinquencies on the program, with $76.3 million in unpaid principal on outstanding loans and a 50.20% delinquency ratio on its four loans.

Georgia's Own, Jefferson Financial and Hancock Whitney were not among the institutions listed as having their licenses revoked in the May 12 USDA release. Hancock Whitney declined to comment. Georgia's Own did not respond to requests for comment.

U.S. Eagle said it acknowledges that its 32.20% delinquency ratio for its USDA portfolio is elevated, but "it is an industrywide issue and not just a U.S. Eagle problem," the credit union's CEO said in his statement.

The move to remove the 10 lenders from the program comes as the agriculture sector has been under stress for the past year following tariff announcements in 2025, and more recently, surging fuel and fertilizer costs due to the war with Iran.

"Stressed conditions bring out government agencies and make them more aware," MacDonald Partners LLP Managing Partner Chip MacDonald said in an interview.