29 May, 2026

Inflation hits 3-year high as Fed officials no longer 'look through' Iran impact

By Brian Scheid

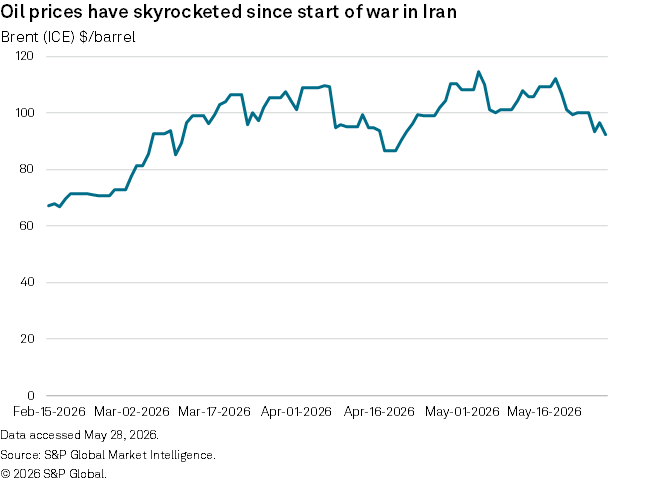

The war in Iran and the related surge in energy prices have pushed inflation to its highest levels in three years and triggered a shift at the Federal Reserve.

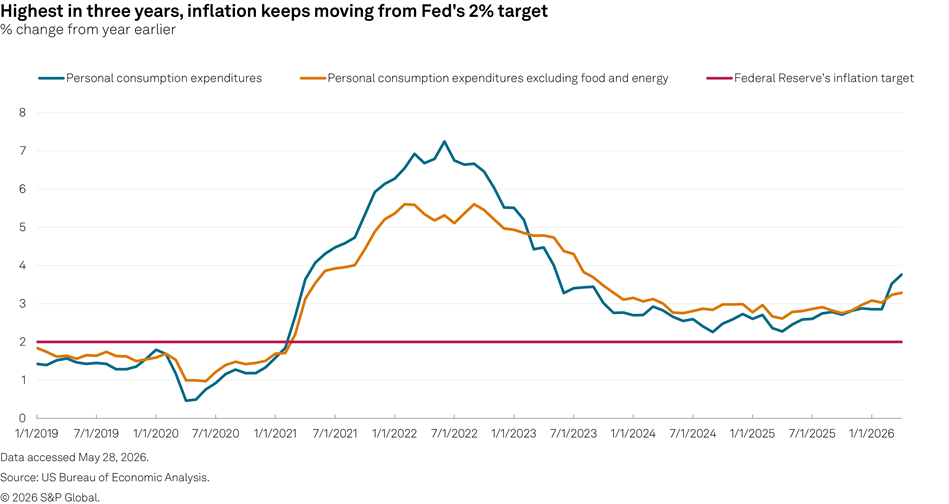

Personal consumption expenditures (PCE), the Fed's preferred inflation metric, jumped nearly 3.8% year over year in April, the highest annual increase since May 2023, and a roughly 150-basis-point increase from a year ago, the US Bureau of Economic Analysis reported May 28. So-called "core" PCE, which removes volatile energy and food prices, climbed by just under 3.3%.

Central bankers are now being forced to reassess their initial views that the Middle East war's impact on prices would be short-lived.

"It's becoming harder for policymakers to ignore inflation troubles that can't be easily explained by one-off supply shocks and have not just lingered but actually grown," said Kevin Burgett, a senior economist at Monetary Policy Analytics.

Long-run inflation expectations climbed to 3.9% in May, up from 3.5% in April, according to the University of Michigan's consumer survey released May 22. As the war in Iran drags on, keeping energy and other commodity prices elevated, those inflation outlooks could further worsen.

"If inflation expectations become de-anchored, we know from the 1970s that that's a really, really big problem," said Jill Cetina, associate director of the commercial banking program at Texas A&M University's Mays Business School. "We are really at risk, maybe we're already there, in terms of consumer inflation expectations being permanently changed."

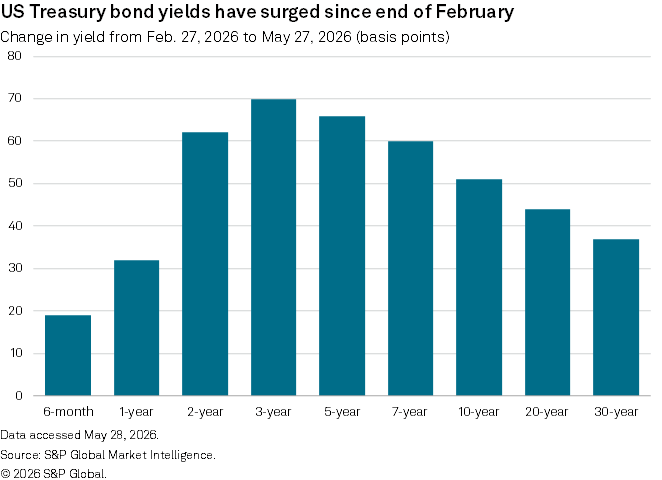

Lasting inflation impacts from the war have triggered a global leap in government bond yields, reversing expectations earlier this year of rate cuts. In the US, Federal Reserve officials no longer believe the central bank can "look through" the price effects of the war, as potentially the biggest energy supply shock in history has flipped rate-cut expectations to rate-hike probabilities.

"Inflation is not headed in the right direction," Fed Governor Christopher Waller said in a May 22 speech.

While Waller was initially hopeful that the Iran war would be "quickly resolved," uncertainty about the ultimate impacts of the ongoing energy shock compelled him to see a rate increase as likely as a cut as the Fed's next move.

"After four supply shocks in five years, the look-through framework is genuinely under strain," said Shawn Severson, CEO and head of market and thematic research at Water Tower Research.

Still, there is probably not enough of a case for hikes just yet, according to Severson. Core PCE would likely need to be above 3% for two or three consecutive months, price pressures would need to broaden from goods to services, and the labor market would need to be very firm, he said.

While the war has been a negative shock to the economy, some of the impact was blunted by fiscal stimulus, tax refunds and draws from oil and gas inventories, Cetina said. The partial offsets have lessened or entirely disappeared of late, increasing the likelihood of energy prices going parabolic.

"The potential recession risks that could come as a second phase I think are underappreciated and underpriced," said Cetina.

Waller was one of the first on the rate-setting Federal Open Market Committee to argue for rate cuts to counter downside risks to employment growth, so his conversion toward a more neutral stance suggests that the majority of Fed officials now see rising inflation as the prominent risk, according to Philip Marey, a senior US strategist at Rabobank.

"The FOMC's focus will likely be on the stability of longer-term inflation expectations," Marey said. "Once they become unanchored, we could see more persistent inflation with wages and prices reinforcing each other. This could trigger the committee to hike."

For now, the bias amongst the majority of Fed officials is neutral, said Burgett with Monetary Policy Analytics. If energy prices remain significantly elevated and inflation worsens, the Fed's bias could shift to a more restrictive one later this summer, potentially lining up a hike by September.

"I'd expect any such shift, if there is one at all, to be a little later than that, though," Burgett said.