20 May, 2026

Global bond selloff persists as inflation expectations rise, upending rate plans

By Brian Scheid

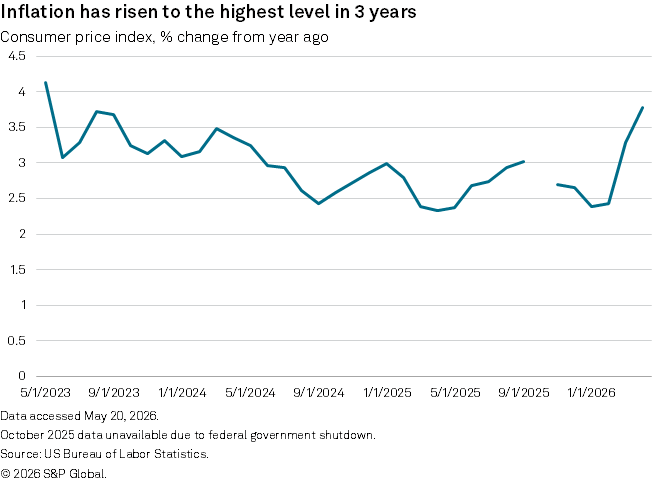

Rising inflation, expectations for persistently elevated interest rates, and the ongoing war in Iran have triggered a global bond sell-off with no clear signs of an end.

Government bond yields, which move opposite prices, have surged to their highest levels in decades in some cases as soaring energy prices have compelled central banks to shelve rate-cut plans and economies brace for slower growth and potential slumps in stocks and other financial markets.

"Investors are increasingly demanding higher yields to compensate for persistent inflation risk, expanding sovereign debt issuance, and uncertainty around central bank policy," said Jay Menozzi, chief investment officer and portfolio manager at Easterly Orange.

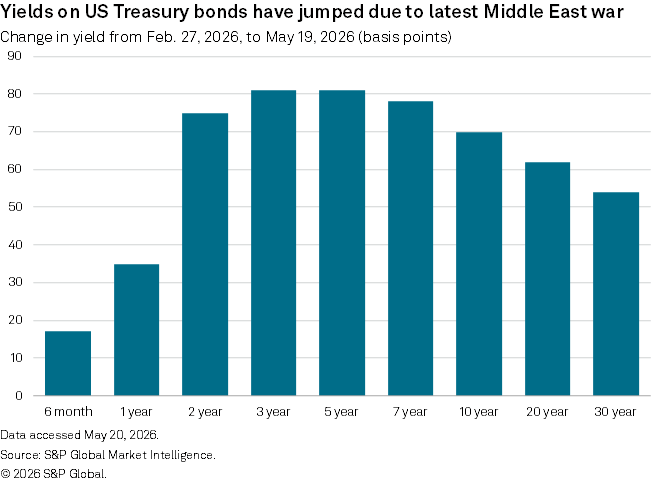

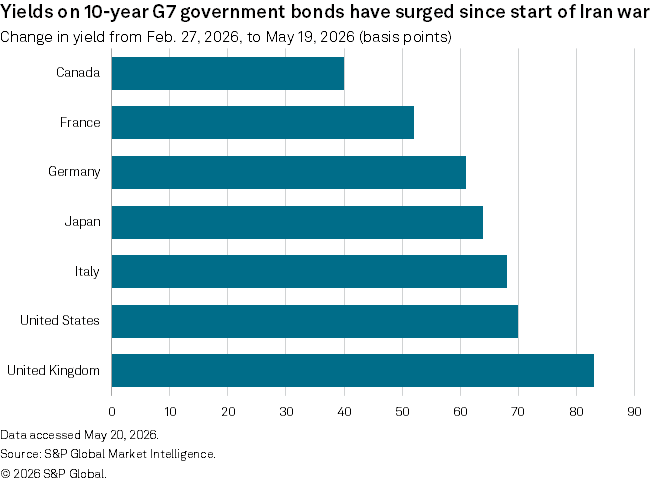

In the US, the benchmark 10-year Treasury yield has climbed 70 basis points since the start of the Iran war at the end of February. The 10-year yield is now trading at its highest point since January 2025 and will likely move higher as inflation expectations rise and the Fed keeps rates higher for far longer than most central bank watchers anticipated earlier this year.

"The basic market assumption is that the Strait of Hormuz will remain stuck … and while it's stuck, inflation expectations continue to ratchet higher," said Padhraic Garvey, head of global rates and debt strategy at ING. "If that's true, it's tough to imagine any other route for Treasury yields apart from up, at least in the coming few weeks."

The 10-year US Treasury yield settled at 4.67% on May 19 and could "snap higher in yield at any point" if investors see inflation rising even more and begin to aggressively sell bonds, Garvey said.

Since the start of the Iran war, flow data shows that selling in the US bond market has been largely offset by buying as inflation expectations have slowly risen, Garvey said. While those expectations could moderate or even lessen in the near term, depending on the path of the war, yields will likely test higher, Garvey said.

"Whatever happens, we are being left with an echo of higher inflation," Garvey said. "So, even if we were to see an earlier-than-expected end to this conflict, yields won't lurch lower dramatically."

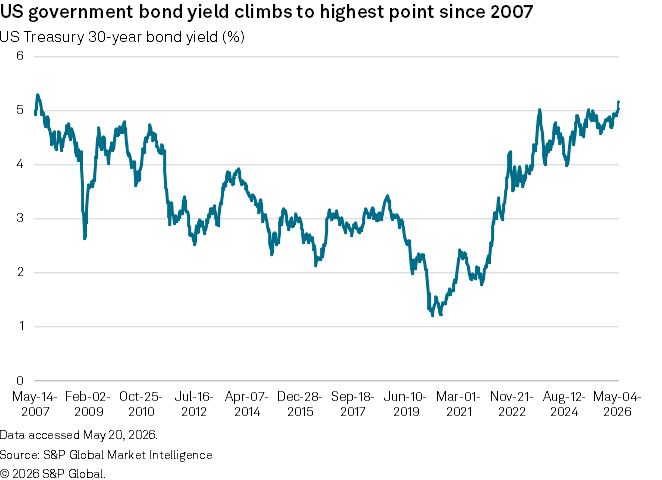

The 30-year Treasury yield this week climbed to 5.18%, a 54-basis-point rise from the end of February and the highest yield for this long-dated government bond since 2007.

"Long-end Treasury yields have been rising, driven mainly by risk of higher and stickier inflation, while growth and labor markets are healthy," said Guneet Dhingra, head of US rates strategy at BNP Paribas. "While fiscal risks are also increasing, they are yet to fully impact long-term yields and remain a source of significant upside risk to 30-year yields."

With inflation risk likely remaining relatively high and fiscal risks potentially increasing, the 5% yield on the 30-year US bond that was broken through in early May could soon be seen as the market's floor, rather than its ceiling, Dhingra said.

"We do not believe yields have peaked," Dhingra said.

Central bank pressure

Bond yields could rise further as investors see inflation as more persistent and more susceptible to second- and third-round effects, pushing businesses to pass on higher costs to consumers, putting more pressure on inflation expectations and wage growth, said Michael Hewson from MCH Market Insights.

All this could pressure central banks to keep rates on hold for far longer than forecast, but also boost the likelihood of modest rate hikes before the end of this year.

"Pressure is already starting to build," Hewson said. "The prospect of higher yields could well have a negative effect on the prospects for global growth, as well as potentially capping any further upside potential for stock markets."

As higher inflation drives up bond yield, consumers' capacity to spend is seeing reductions, Garvey with ING said. Higher prices will likely need to be offset by higher labor costs, giving the Fed a strong case for rate hikes, which will elevate the costs of car loans, mortgages and other leveraged purchases.

"The higher bond yields go, the bigger are these material pulls on the economy," Garvey said.

Ultimately, the impact of high bond yields on the broader economy will depend on whether rates rise in an orderly fashion or spike suddenly to levels that materially tighten financial conditions, Menozzi with Easterly Orange said.

"If bond yields remain elevated but do not move sharply higher, particularly if the 10-year Treasury remains below the 5% threshold, the impact on broader risk assets may remain manageable, especially given the current administration's preference for stable financial conditions and resilient equity markets," Menozzi said. "That said, higher-for-longer rates will gradually create economic headwinds."