06 May, 2026

Exit outlook dims for private equity's long-held software investments

Recent advances in AI are complicating the exit outlook for private equity firms with long-held portfolio companies that operate in the software industry.

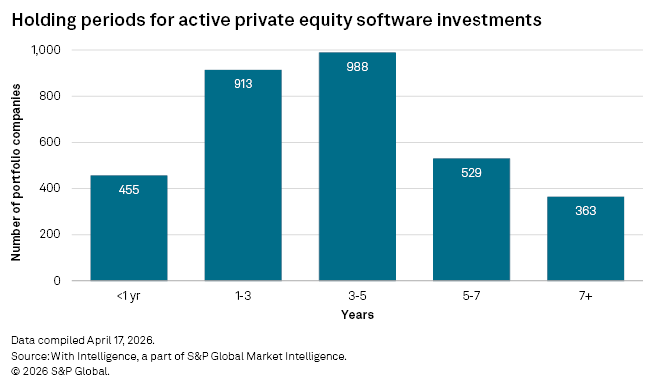

More than 27% of active private equity portfolio companies in North America's software industry as of April were businesses acquired at least five years earlier, according to the "Private Equity Harvest Report 2026" from SPS by With Intelligence. About 11% were acquired seven or more years ago, well beyond the point when a private equity fund manager typically seeks to exit a portfolio company investment through a sale or IPO and return profits to the fund's limited partners.

The median hold time for North America-based private equity portfolio companies at exit was 5.4 years as of the fourth quarter of 2025 and just five years in the technology sector, which includes the software industry, according to With Intelligence data.

Owners of software portfolio companies preparing for exit in 2026 must contend with diminished tech-sector deal activity and unanswered questions around AI's potential to undermine software company business models and valuations, said Scott Denne, a senior financial research analyst at 451 Research from S&P Global Energy Horizons.

"The holding periods are longer and they're going to get longer because there effectively isn't an exit market for these companies," Denne said.

Public market signals

Concerns about AI's impact on the software sector escalated earlier in 2026 in a rout of software stocks, with the S&P North American Technology Software Index shedding 27.73% of its value between Jan. 1 and April 10 before partially recovering. As of May 4, the index was down 14.03% for the year, a period when the S&P 500 gained 4.99%.

The declines reflect uncertainty about how AI might disrupt software revenue streams, including seat-based licensing models that charge per user. Now that some of those human users may be replaced by AI agents, software-as-a-service companies are being forced to consider switching to consumption- or usage-based pricing models, said Scott Twibell, co-head of the global technology group at investment bank Lincoln International LLC.

"Software business models are changing. You have this pressure on the seat-based license concept that's been around a long time," Twibell said.

In addition, revenue growth across public sector software companies has fallen to about 15% since peaking close to 30% in the second quarter of 2021, during the COVID-19 pandemic.

"Private companies are going to have a similar dynamic, where growth is worse," Denne said.

Degraded valuations

Against that backdrop, the valuation multiples paid by software company acquirers are declining.

Since 2015, software company acquirers have paid a median multiple of 4.1x trailing-12-month revenue, according to 451 Research M&A KnowledgeBase data. That median multiple peaked to 6.4x in 2021 and remained at 5.8x in 2022, but acquirers paid a median multiple of just 3.2x in 2026 as of April 20.

That period of peak valuations coincided with a private equity buying spree, when fund managers loaded up on software businesses, noted Adam Reilly, a national managing partner at accounting firm Deloitte LLP.

Reilly said AI will not have a uniform impact across the software sector, and the advances in AI technology are likely to boost some businesses even as they undermine others. But for private equity managers aiming to exit software companies in the near term, widespread valuation declines are "a pretty big sticking point," Reilly said.

The high prices paid at entry, combined with the less certain growth outlook for software, are eroding the returns that private equity firms earn on investments in the tech sector, according to a report issued in April by consultant Bain & Co. Buyouts completed between 2020 and 2022 generated a median return of 2.1x at exit, below the 2.9x return for tech buyouts completed in the 2010–19 period, according to Bain.

Slow software M&A

A sharp decline in software deals is another factor in the dimming exit outlook.

Software M&A totaled $310 billion in 2025, including deals both with and without private equity involvement, but activity was well off that pace in 2026, with just $25 billion of software deals recorded this year through April 20, according to 451 Research M&A KnowledgeBase data. Most of the year-to-date deal value — $18 billion, or 72% of the total — was linked to deals announced in January.

Potential strategic acquirers for application software businesses are, in many cases, listed software businesses that have recently seen their stock prices drop. Strategic investors typically structure M&A deals with a mix of cash and stock, but with their stocks trading lower, they are "much less able and less interested in paying up" for acquisitions, Denne said.

Private equity firms may be struggling with a similar lack of M&A firepower. Buyouts rely on substantial debt, but pressure on private credit funds — under scrutiny from investors concerned about the software loans in their portfolios — may mean debt is harder to come by, and elevated interest rates make loans more expensive, Denne said.

Private equity firms are also getting choosier. About 64% of private equity firms surveyed by EY for its first-quarter "Private Equity Pulse" report said AI disruption risk made them "more selective" in allocating capital to software.

Outlook

Twibell said the tech deals that close in May and June — deals that were being structured as headlines warned of a "Saaspocalypse" — will give a good indication of the path of software M&A in 2026. Large deals, in particular, would give private equity sponsors more confidence in lining up software portfolio companies for IPOs, Twibell said.

The reception of expected mega-IPOs this year by OpenAI LLC, Anthropic PBC and Space Exploration Technologies Corp., or SpaceX, will gauge investor appetite.

If software companies remain stuck in private equity portfolios, it will only add to the pressure fund managers are under to monetize investments and return capital to investors.

"It certainly weighs on that fundraising cycle," Denne said.

With Intelligence is a part of S&P Global Market Intelligence.

451 Research is a technology research group within S&P Global Energy Horizons.